Why Tech Giants Rush to Invest in “NeoClouds”

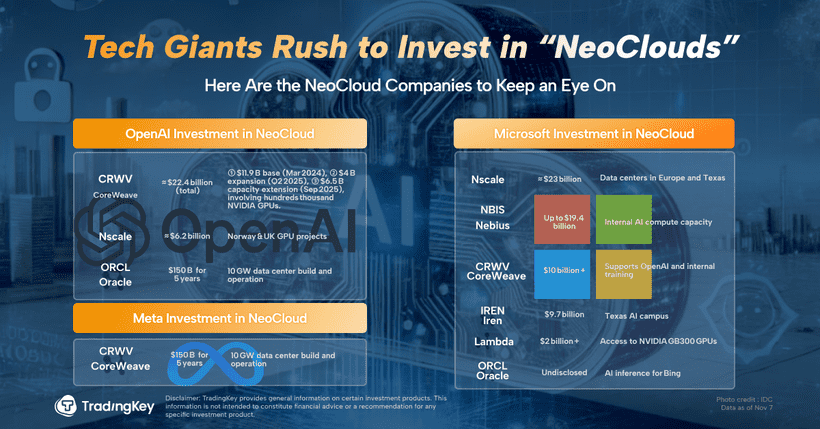

TradingKey - On Wednesday, reports confirmed what many had been watching unfold slowly but steadily: Microsoft is ramping up its investment in next-generation AI infrastructure—what some are calling the “new cloud,” or NeoCloud. Total capital now committed by Microsoft to data center partnerships tied to this strategy exceeds $60 billion.

One of its biggest moves? A $23 billion deal with Nscale, a UK-based startup working on AI-native compute infrastructure. In exchange, Microsoft will gain access to roughly 200,000 units of NVIDIA’s next-generation GB300 GPUs across locations including the UK, Norway, Portugal, and Texas. Since Bloomberg first published a running total of Microsoft’s NeoCloud-related spend in October, the number has nearly doubled.

Just two days earlier—on Monday—Microsoft had announced two more sizeable NeoCloud partnerships, totaling over $10 billion. The partners: Lambda Labs, a U.S.-based GPU cloud provider, and Australian miner-turned-datacenter operator Iren.

Across the broader NeoCloud space, names like Nebius and CoreWeave have also emerged as competitive players—moving fast and raising capital on the back of announced hyperscale deals.

In early September, Microsoft signed a $19.4 billion compute capacity agreement with Nebius. Just weeks later, CoreWeave disclosed a separate order from NVIDIA worth at least $6.3 billion. Under that agreement, NVIDIA commits to purchasing unused GPU inventory from CoreWeave through April 2032.

And in late September, CoreWeave made headlines again—this time with Meta. Their new supply contract: up to $14.2 billion in GPU-backed compute capacity. Each of these announcements has helped push CoreWeave—and the broader NeoCloud thesis—further into mainstream capital markets.

If there’s been a surprise in this trend, it’s what’s not happening: enterprise spending shows no signs of slowing. Despite record capex figures, hyperscalers continue to deepen their AI infrastructure pipelines—suggesting the cycle is not yet topping out.

NeoClouds Rise on Soaring AI Computing Demand

It’s a fair question. Microsoft already operates one of the world’s most mature and globally scaled public cloud infrastructures. So why the need to co-invest with third-party data center specialists?

The answer comes down to one thing: AI workloads, and the compute gap they have exposed.

Unlike traditional cloud service providers (think AWS, Google Cloud, Azure), NeoCloud players offer access to bare-metal GPU compute—meaning users get physical control over the hardware without the additional abstraction layers of traditional cloud environments. These setups allow elite AI builders to maximize utilization, customize software environments, and execute model-scale training workflows with minimal OS overhead.

In other words, this category isn’t just about servers. It’s about optimization at the rack-to-algorithm level.

NeoCloud providers focus exclusively on delivering the most scarce and most powerful GPU resources—with no intermediary services between the hardware and end-user environment. That means no bundled APIs, minimal platform lock-in, and far greater performance per dollar in high-compute scenarios.

For leading AI labs and frontier model teams, the value proposition is clear: hundreds of thousands of GPUs, vertically integrated, and tuned for peak efficiency during parallel training runs. Traditional clouds, by contrast, are optimized for flexibility, not intensity.

But Beneath the Boom—Some Cracks Are Forming

If 2023 was the year of NeoCloud’s rise, 2024 may be the year of financial scrutiny. CoreWeave, arguably the category leader, offers a compelling example of both scale and fragility.

Following Microsoft’s order, CoreWeave secured billions in financing from Blackstone and other lenders—deploying the capital to expand its GPU fleet and lock in more NVIDIA capacity. But this debt-driven growth model is starting to raise flags.

While top-line growth has remained eye-catching—driven by expanding client orders—profitability remains structurally elusive. CoreWeave’s latest financials show accelerating revenue, but nearly zero profits. At the same time, long-term debt has reportedly surpassed $17 billion, with interest costs beginning to weigh.

The Microsoft-core NeoCloud playbook is starting to become recognizable: co-develop data centers, lease or acquire GPUs from NVIDIA, scale GPU clusters to hyperscaler-grade demand. But behind the infrastructure execution sits a heavy dependence on credit—and on the assumption of persistently rising AI demand.

If demand softens, or GPU monetization lags, financing risk may no longer be downstream—it may move upstream in the chain.

So far, AWS, Google Cloud, and Azure have not launched open counter-strategies. But they may not stay silent for long.

As NeoCloud players begin aggregating high-value AI training workloads—club deals, lab contracts, large-model leases—it’s possible the dominant public clouds reassert themselves, either by acquiring bare-metal operators or standing up internal equivalents. Already, some cloud providers have begun tweaking pricing and provisioning for GPU-heavy users.

The challenge is not technical. It’s strategic: whether to accommodate runaway compute intensity within existing cloud environments—or to treat AI-native infrastructure as a distinct modality entirely.

Recommended Articles