This AI Stock Has Soared 475%, But Here's 1 Reason It Still Isn't a Bubble

Key Points

Analysts don't expect Nebius to deliver big gains in the coming year, and that's no surprise after looking at its expensive price-to-sales ratio.

However, Nebius is expected to deliver phenomenal growth in the coming years.

The company has already landed a significant contract, and the booming demand for AI computing capacity points toward years of terrific growth.

- 10 stocks we like better than Nebius Group ›

Neocloud provider Nebius Group (NASDAQ: NBIS) delivered sizzling returns on the market in the past year, rising 475% as of this writing. This stunning surge in the stock is backed by the outstanding growth in the company's revenue in recent quarters, a result of the remarkable demand for its artificial intelligence (AI) data centers.

This phenomenal rally may lead investors to think that Nebius stock is in a bubble. A closer look at the company's valuation would also suggest the same. But is it really in a bubble? Let's find out.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images

It may seem that Nebius stock has gotten way ahead of itself...

Nebius currently has a price-to-sales ratio (P/S) of 114. That's extremely expensive when we consider that the U.S. technology sector index has an average sales multiple of 9.5. Meanwhile, Nebius peer CoreWeave (NASDAQ: CRWV) is trading at 19 times sales, and it has been growing at an incredible pace as well.

CoreWeave reported a tripling of year-over-year revenue in the second quarter to $1.21 billion. Nebius' revenue, meanwhile, came in at $105 million, but it jumped much faster at 645% compared to the year-ago period. Nebius bulls may argue that the company's significantly faster growth than CoreWeave justifies its expensive valuation. Even then, its P/S seems like too much of a stretch.

The sky-high valuation explains why Nebius' 12-month median price target points toward a jump of just 25% from current levels. That's why anyone who's looking to buy this AI infrastructure stock may not be inclined to do so in light of its prohibitively expensive valuation and limited upside potential in the coming year.

That's because any signs of a slowdown in the company's growth could send the stock into a downward spiral considering its valuation, which suggests that it is in bubble territory right now. However, there's a simple reason this cloud infrastructure company isn't in a bubble.

...but its tremendous backlog suggests otherwise

Nebius is in the business of building dedicated AI data centers powered by the latest chips from the likes of Nvidia, Advanced Micro Devices, and Intel. It also provides a software stack that includes managed services and tools to train or fine-tune models, run AI inference applications, and develop custom AI applications, among other things.

Nebius gives its customers the flexibility to rent its infrastructure on an hourly basis or purchase tokens for running AI inference applications. This business model is in great demand. There is a shortage of AI computing infrastructure in the cloud, which is why companies are buying whatever capacity they can lay their hands on.

Microsoft, for instance, said in its latest earnings conference call that the demand for its Azure AI cloud services "again exceeded supply across workloads even as we brought more capacity online." The tech giant has been taking steps to get its hands on more AI capacity, and that was precisely why it offered Nebius a huge contract a couple of months ago.

Nebius will provide Microsoft with dedicated GPU infrastructure capacity over a five-year period in a contract valued at $19.4 billion.

The contract runs through 2031, and Nebius says that it will begin deploying infrastructure for Microsoft from 2025. This is a big deal for a company that was expecting to hit an annualized run-rate revenue (ARR) of $1 billion by the end of 2025 before this contract was announced.

The Microsoft contract alone has the potential to substantially boost Nebius' growth over the next five years, and analysts are expecting its top-line growth to simply take off.

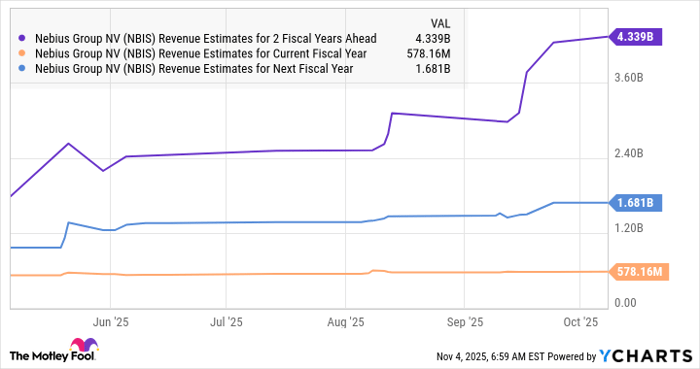

NBIS Revenue Estimates for 2 Fiscal Years Ahead; data by YCharts.

Nebius was growing at an incredible pace even before it landed the Microsoft deal, so the demand for its computing infrastructure was already strong. The company has been aggressively looking to bring more data center capacity online. It had 220 megawatts (MW) of connected capacity by the end of the second quarter. The company plans to increase its contracted data center capacity to more than 1 gigawatt (GW) by the end of 2026.

The added capacity brought online should sell out quickly thanks to the shortage of computing capacity. That should allow the company to achieve the remarkable revenue growth that analysts are anticipating. Assuming Nebius hits $4.4 billion in revenue in 2027 (as seen in the previous chart) and trades at a significantly discounted 19 times sales at that time (in line with industry peer CoreWeave's sales multiple), its market cap could jump to almost $84 billion.

That would mean a potential jump of 180% from current levels. So, investors looking to buy a fast-growing AI stock can still consider Nebius because the huge Microsoft contract and the hunger for AI computing infrastructure can ensure years of strong growth for the company.

Should you invest $1,000 in Nebius Group right now?

Before you buy stock in Nebius Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nebius Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $592,390!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,196,494!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 193% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of November 3, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Intel, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short November 2025 $21 puts on Intel. The Motley Fool has a disclosure policy.

Recommended Articles