ASML Q3 Preview: Outlook Under Pressure — Order Execution and New Guidance in Focus

TradingKey - ASML is set to release its third-quarter financial results on October 15 at 7:00 a.m. Central European Time. Over the past month, ASML’s shares have surged 45%, making it Europe’s most valuable company by market capitalization in September — its best-performing month in two decades.

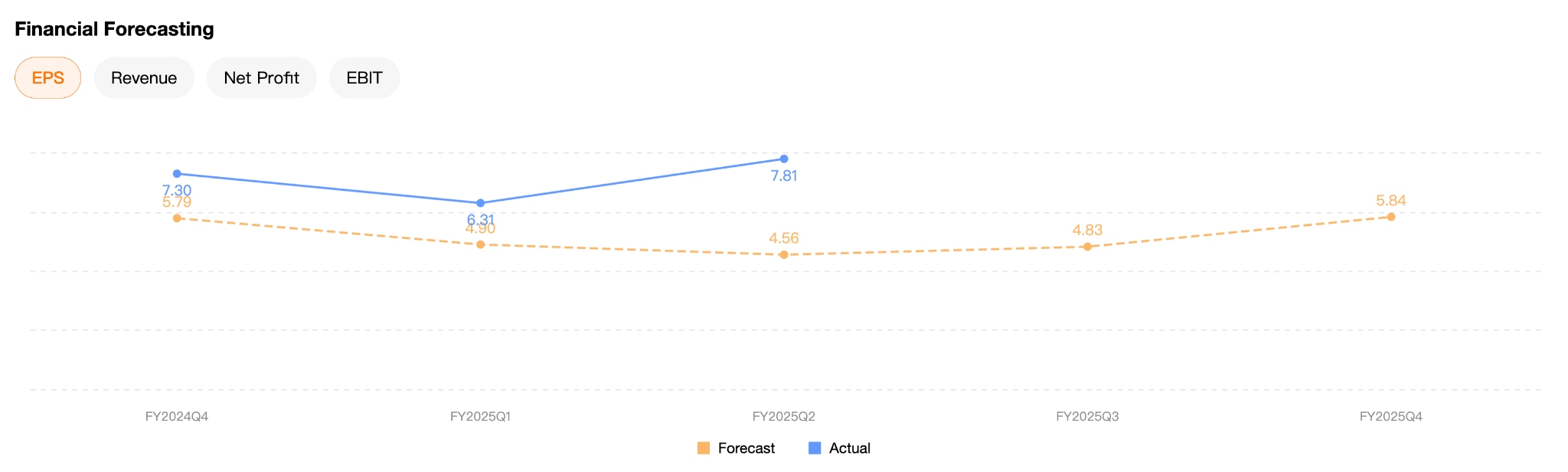

According to LSEG data, analysts expect ASML’s Q3 revenue to rise 3.51% year-over-year to €7.729 billion, with earnings per share (EPS) up 2.67% to €5.421.

[ASML EPS Forecast, Source: TradingKey, LSEG]

Short-Term Margin Pressure Amid Structural StrengthASML’s profitability in Q3 may experience temporary weakness, primarily due to rising costs associated with revenue recognition from its High Numerical Aperture (High NA) EUV systems. While this technology currently weighs on overall gross margins, it represents the future of semiconductor process advancement and holds strategic importance for long-term competitiveness.

Additionally, macroeconomic uncertainty and shifts in customer purchasing patterns could further pressure quarterly profits. However, steady growth in equipment maintenance and service revenue will provide some support to overall performance.

High NA Rollout: A Key Market FocusThis quarter marks a critical phase for the commercial rollout of High NA EUV systems. The pace of volume production and customer feedback — particularly from Intel and TSMC — will be closely watched and could significantly influence investor confidence.

Despite near-term margin headwinds, demand for EUV remains strong. Investment cycles in AI-driven logic chips and advanced node expansions continue, indicating that the underlying growth trajectory of EUV remains resilient.

With high expectations ahead of Wednesday’s report, investors are looking for ASML to deliver an upgraded outlook for next year — stronger than the guidance provided in July. Amid ongoing trade tensions, markets are also seeking evidence that chip equipment makers like ASML are beginning to monetize the current AI boom.

“Investors now want to see whether increased AI-related capex from chipmakers is starting to show up in ASML’s order book,” said Reinder Wietsma, Portfolio Manager at Centive Global.

JPMorgan analysts noted that ASML’s recent rally has been largely driven by hedge fund buying, while long-term institutional investors remain cautious or on the sidelines. While a more optimistic view on 2026 would be welcomed, concerns remain that “management may still lack sufficient clarity” to fully reassure the market.

Recommended Articles