Broadcom's Valuation Gets Fresh Fuel from Blowout Earnings Guidance

TradingKey - Broadcom crushed earnings expectations, reigniting interest in its AI-driven growth potential.

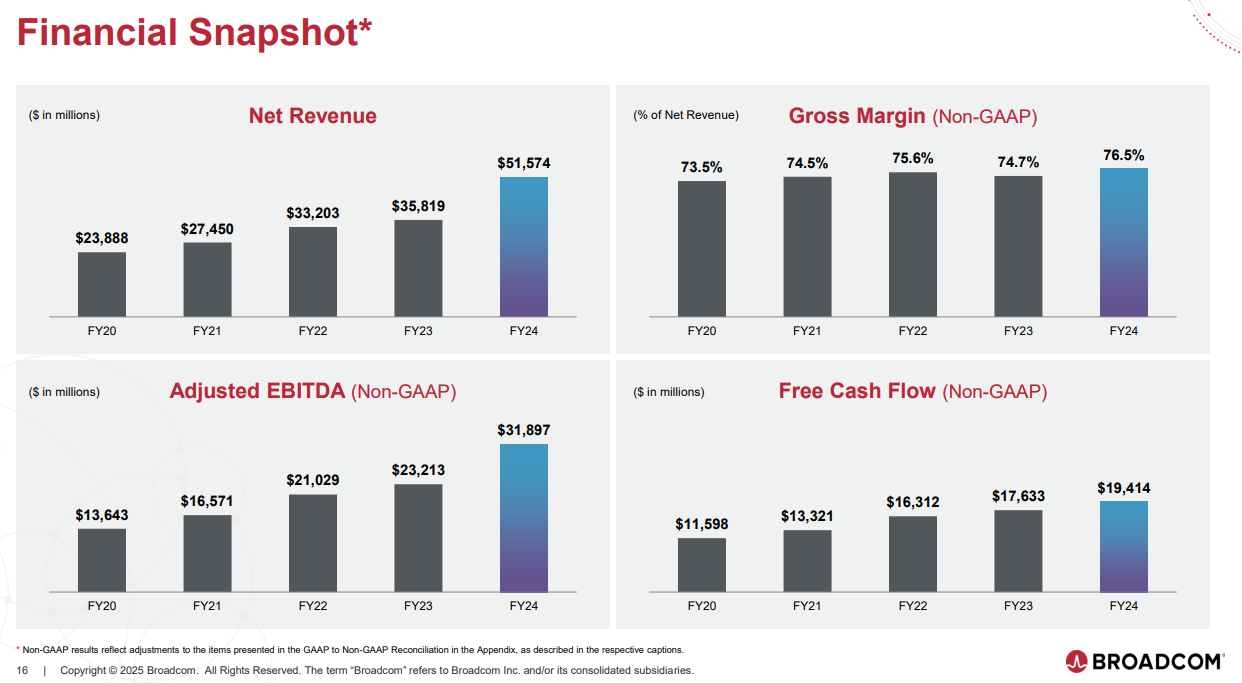

For the fiscal second quarter, Broadcom reported $5.2 billion in AI-related revenue, exceeding Wall Street estimates. More importantly, management raised its long-term guidance, pointing to a strong ramp-up in shipments in FY2026 — and forecasting that next year’s growth could outpace 2025.

That optimism didn’t go unnoticed: shares jumped 1.23% after hours and nearly 11% pre-market. Since April, the stock has doubled, making it the third-best performer in the Nasdaq-100 over that time period.

So the big question is: can AVGO go even higher from here?

The Real Growth Engine: Custom AI Chips

This quarter’s spotlight is firmly on Broadcom’s AI acceleration business. On the earnings call, CEO Hock Tan revealed that in addition to the three large cloud customers they've already secured, Broadcom has landed a massive $10 billion order from a fourth unnamed client for custom AI silicon.

While Tan didn’t say who the customer is, industry chatter points toward OpenAI. With GPT-5 in the pipeline, OpenAI CEO Sam Altman has said the company plans to double its compute capacity in the next five months. Meanwhile, multiple reports suggest OpenAI is trying to reduce its dependence on Nvidia — using AMD chips via Microsoft Azure and exploring custom chips tailored to its model workloads.

That’s where Broadcom comes in, offering custom-built XPU chips and high-speed networking products specifically for AI training and inference tasks.

Why Custom Silicon Is Getting Hot

Nvidia may dominate the AI GPU market, but custom silicon is increasingly being adopted by Big Tech players — and for good reasons.

ASICs (application-specific integrated circuits) offer several key advantages: they deliver hardware that's tailor-made for a specific workload, meaning faster performance and greater power efficiency. And when deployed at scale, custom chips cost significantly less per unit of compute and energy compared to GPUs.

In short — companies like OpenAI, Microsoft, Google, and Amazon are all exploring (or actively using) their own chips because it helps reduce bottlenecks, manage costs, and improve overall system output. Broadcom is well-positioned to meet this demand.

Expectations Are High — But So Is the Potential

The latest earnings results clearly show Broadcom is gaining traction in the custom AI chip space. Investors are now speculating: could more hyperscalers follow in OpenAI’s footsteps and turn into major Broadcom customers?

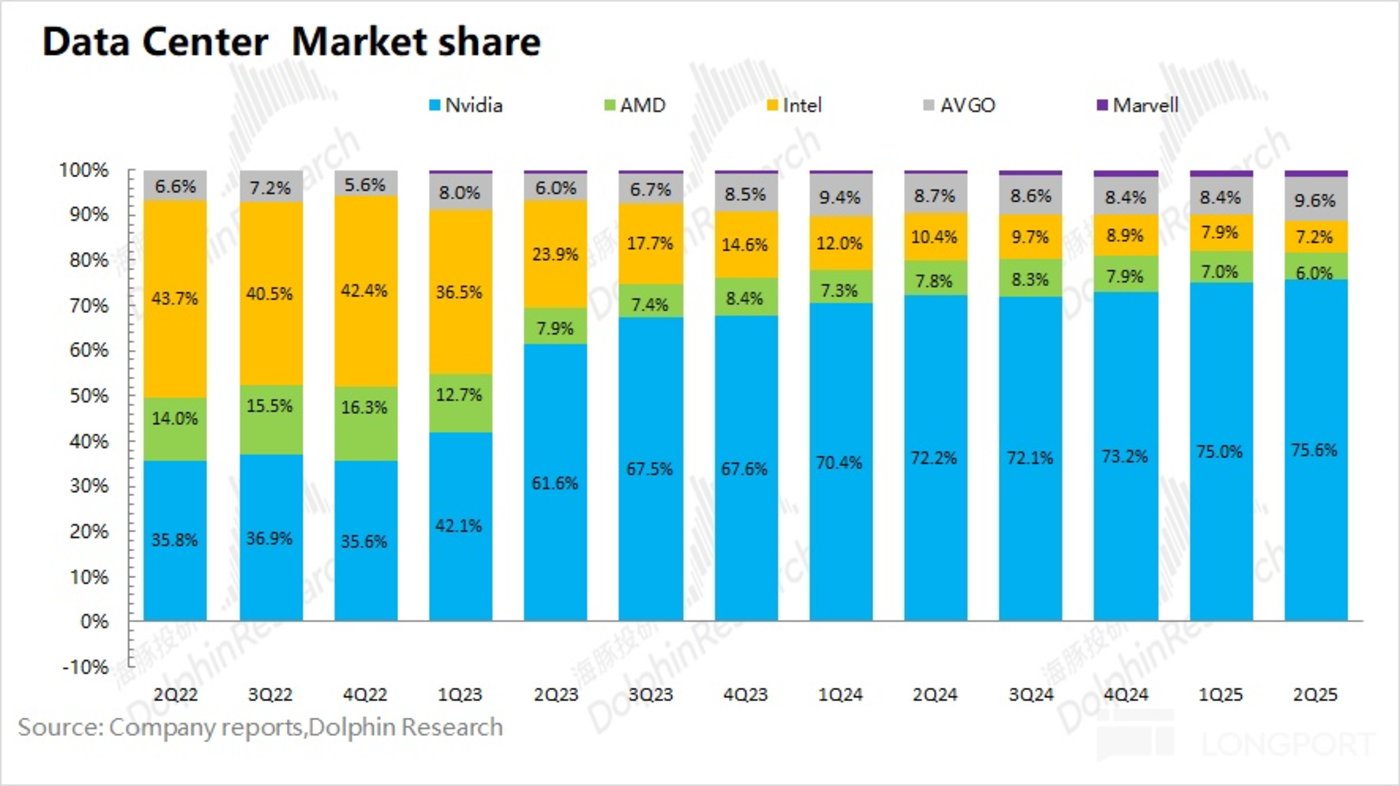

As it stands, Broadcom has already moved past AMD in AI data center networking and custom chips and has emerged as a serious alternative to Nvidia in certain segments. If adoption keeps accelerating, its long-term AI revenue — currently priced in at around $60–90 billion — could grow even higher.

That said, the bull case is also looking increasingly “priced-in.” Broadcom is already guiding for 60%+ AI revenue growth next year, so there's limited room for positive surprises above that. Investors may start to wonder if the bar is getting too high.

As Joseph Shaposhnik, PM of the Rainwater Equity ETF (which holds AVGO as its 3rd largest position), put it:

“The business is performing really well, but the stock has already gone up a lot. At this level, anything can happen.”

Valuation is telling a similar story. According to Seeking Alpha, Broadcom’s forward P/E for FY2025 was revised from 44 to 45 post-earnings — suggesting that the stock's recent gains outpace its earnings revisions.

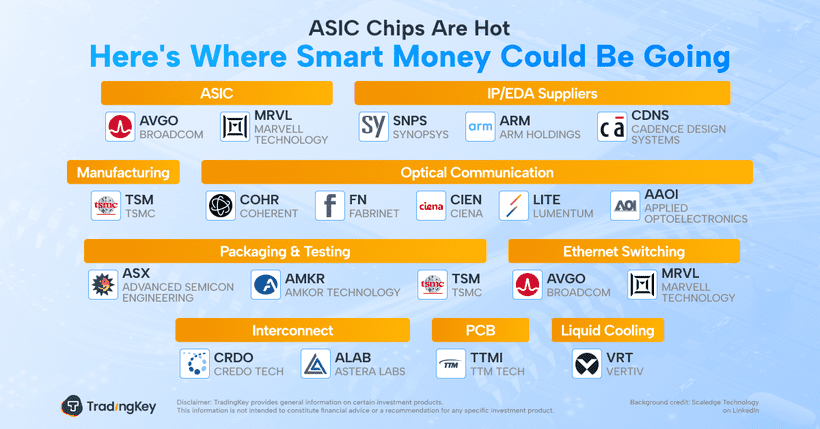

Broadcom Isn’t the Only Player in the ASIC Game

With custom silicon becoming the next frontier for AI infrastructure, the entire ASIC supply chain is gaining attention. And several other players — many trading at more reasonable valuations — are worth a closer look.

Upstream: These companies lay the groundwork for chip design and manufacturing — providing IP, design tools, wafers, and equipment. Names to watch include:

- Arm Holdings (ARM) – IP design and licensing

- Synopsys (SNPS), Cadence Design Systems (CDNS) – EDA software

- Taiwan Semiconductor (TSMC), ASE Technology (ASX), Amkor (AMKR) – foundry and packaging services

Midstream: This is where full ASIC design and production happens — from logical design through to tape-out, fabrication and packaging. Key players include:

- Broadcom (AVGO), Marvell (MRVL) – full-stack ASIC players

- Packaging: TSMC, ASE, Amkor

Downstream: This segment includes companies integrating ASICs into data centers, advanced networking, and high-performance systems:

- Broadcom (AVGO), Marvell (MRVL) – AI accelerators and Ethernet chips

- Coherent (COHR), Lumentum (LITE), Fabrinet (FN), AAOI – optical interconnects

- Credo Technology (CRDO), Aster Labs (ALAB) – high-speed networking

- TTM Technologies (TTMI) – circuit board solutions

- Vertiv (VRT) – liquid cooling and data center infrastructure

Recommended Articles