Q2 Earnings Show AMD’s Strength Beyond the Blemishes — Sales to China Could Be a Game-Changer

TradingKey - AMD (Advanced Micro Devices), the world’s second-largest AI chipmaker after NVIDIA, delivered a record-breaking second-quarter performance on August 5, with revenue and guidance exceeding expectations. However, investors reacted negatively to uncertainty around the resumption of chip exports to China, sending AMD’s stock down more than 5% in after-hours trading.

Solid Quarter Amid Policy Headwinds

AMD reported:

- Q2 revenue: $7.685 billion, up 32% YoY, above the $7.43 billion consensus

- EPS: $0.48, down 30% YoY, slightly below the expected $0.49

The earnings decline was largely due to a non-cash inventory charge of $800 million related to U.S. export restrictions on its Instinct MI308 AI accelerator — a one-time impact from the Trump administration’s April 2025 decision to restrict exports of advanced chips to China.

Despite the drag, AMD issued strong forward guidance:

- Q3 revenue outlook: $8.4–9.0 billion, above the $8.37 billion consensus

- Gross margin expected to rebound to 54%, up from 43% in Q2

If not for the export-related charge, Q2 gross margin would have been 54% — consistent with the previous two quarters.

China Export Uncertainty Weighs on Sentiment

The key variable shaping AMD’s outlook is U.S. policy on semiconductor exports to China.

While Washington has reportedly begun re-easing restrictions as part of ongoing U.S.-China trade talks, AMD has not yet received final approval to resume MI308 shipments.

CEO Lisa Su said during the earnings call that the licenses are still under review. They are not including any MI308 revenue in our Q3 outlook. The timing of revenue contribution depends on when licenses are granted — but overall, the situation is better than it was 90 days ago.

She expressed optimism about the broader AI market, stating that she sees a clear path for their AI business to reach multi-billion-dollar annual revenue.

AI Demand Broadens Beyond GPUs

Su highlighted growing demand for AMD’s Epyc CPUs in AI infrastructure, driven by the rise of agentic AI — AI systems that perform multi-step tasks autonomously.

She added that every token generated by a GPU triggers multiple CPU-intensive processes — from retrieval to reasoning. This is creating strong demand for general-purpose compute.

While MI308 remains in limbo, AMD’s next-generation chips are gaining momentum:

- MI355 began production in June and is now shipping, with strong initial customer demand

- The upcoming MI400 series accelerators have received positive feedback in early engagements

Mixed Market Reaction

Despite the strong results and optimistic outlook, AMD shares fell ~5% after hours, reflecting investor caution over:

- Lack of clarity on China export timelines

- Valuation concerns after a 77% rally in the past three months

Year-to-date, AMD is up over 44%, outperforming the broader market.

Analysts Remain Constructive

- Mizuho’s Jordan Klein said it’s unclear what level of guidance would satisfy investors, but noted that early demand for MI355 and data center growth are positive signs

- Jefferies had warned that any conservative commentary on China sales could trigger a pullback

- Mizuho expects any sell-off to be moderate and short-lived, creating a buying opportunity

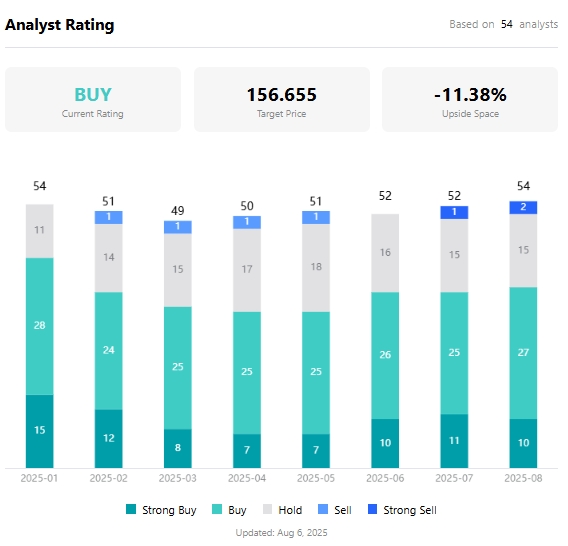

According to TradingKey, the average analyst price target for AMD is $156.66, implying a potential 11% downside from current levels — reflecting lingering caution despite strong fundamentals.

Recommended Articles