BloFin Research Analysis: Market Outlook 2026 Across Crypto Majors, Perp DEXs, and Forecasting Markets

This 2026 outlook examines how evolving market structure is reshaping crypto’s core narratives, from Bitcoin’s changing cycle dynamics to the competitive realities of Layer 1s, perpetual DEXs, and prediction markets.

Bitcoin: Broke the Pattern, Not the Cycle

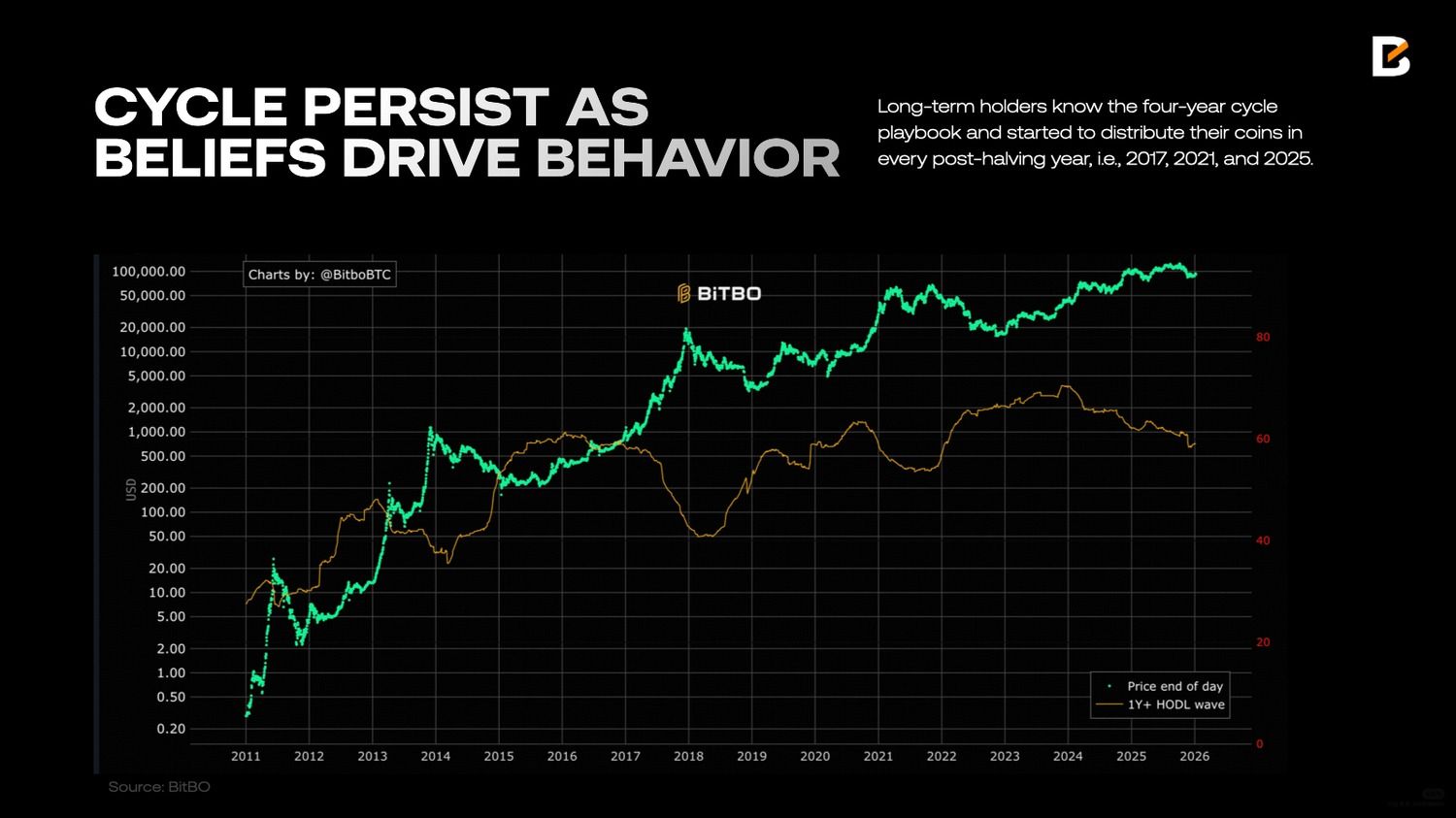

In 2025, Bitcoin presents an apparent contradiction that has reignited debate around the validity of the 4-year cycle theory. Historically, the post-halving year has always seen strong positive returns. In 2025, however, Bitcoin delivered a first-ever negative annual return in a post-halving year, breaking this long-standing belief. Yet, paradoxically, 2025 also saw Bitcoin reach a new all-time high, with the price peak occurring in Q4. This is precisely in line with the prior cycle. In that sense, Bitcoin still followed the cycle, even though the path looked different from the past.

This leads to the second question: if the cycle theory implies that 2026 should be a bear market year, does this framework still hold under today’s market condition, where the demand structure is fundamentally different from the prior cycles? The introduction of spot Bitcoin ETFs and the growing number of institutional investors have entered the market as a consistent bidding power. Unlike retail-driven flows, which tend to be sentiment driven, institutional capital brings the Bitcoin market a more persistent and structured bid, they either view Bitcoin as a long-term hedge to money debasement or allocate a small percentage of portfolio (like 4%) for diversification purposes. Both investment objectives focus more on long-term rather than short-term price fluctuation.

This change has led many to argue that the four-year cycle is dead. However, we believe that declaring the death of the four-year cycle is premature.

Bitcoin’s value is driven largely by investor expectations (since it has no earnings or cash flows), making its price highly reflexive. The four-year cycle pattern played out reliably in all previous times, and Bitcoin peaked again in Q4 2025. Investors, especially those who have remained in the market across multiple cycles, have come to expect this rhythm. That very expectation can, in turn, influence investor behavior and reinforce the cycle itself.

Cycles persist not merely because investors believe that “history repeats,” but because those beliefs drive positioning, creating a self-fulfilling prophecy.

Bitcoin 1-year+ holding wave reflects this dynamic. This metric refers to the proportion of Bitcoin supply that has not moved for at least one year. A declining 1-year+ holding wave suggests long-term holders are distributing coins. These long-term holders know the four-year cycle playbook and started to distribute their coins in every post-halving year, i.e., 2017, 2021, and 2025.

Therefore, while 2026 may not resemble a textbook bear market, the broader framework still offers explanatory power. The cycle is likely to soften and we may not see large drawdowns as severe as in previous cycles due to the structural support provided by institutional capital, but four-year cycle expectation continues to shape timing and sentiment. Against the backdrop of still-tight macro liquidity conditions, 2026 is more likely to be characterized by heightened volatility and range-bound rather than a deep downturn.

For a deeper analysis of Bitcoin in 2026, read here: Whale’s Digital Asset View: Bitcoin’s Cycle Position in 2026

Ethereum: A Stronger Platform, a Weaker Asset Narrative

Back when Ethereum completed the Merge upgrade in 2022 and introduced the fee-burning mechanism via EIP-1559, it had an important monetary narrative as “Ultra-Sound Money”. The thesis was straightforward: as network usage increased, more ETH would be burned, the circulating supply would fall, and ETH as an asset could become structurally deflationary. In that case, ETH was not only the fuel of the Ethereum network, but also a scarce asset capable of functioning as a store of value like Bitcoin.

Fast forward to today, Ethereum’s evolution has unfolded on a very different path. As a decentralized platform, Ethereum has arguably never been stronger. It has cemented itself as the dominant settlement layer for stablecoins, decentralized finance, and tokenization of real-world assets. Hundreds of billions of dollars in stablecoins already circulate on Ethereum and potentially trillions of dollars in tokenized financial assets is not a far-fetched expectation.

Ethereum has also successfully executed its Layer 2 scaling roadmap, dramatically reducing transaction costs and improving user experience. With rollups now handling the bulk of transactional activity, Ethereum’s development focus has shifted back to Layer 1 scalability.

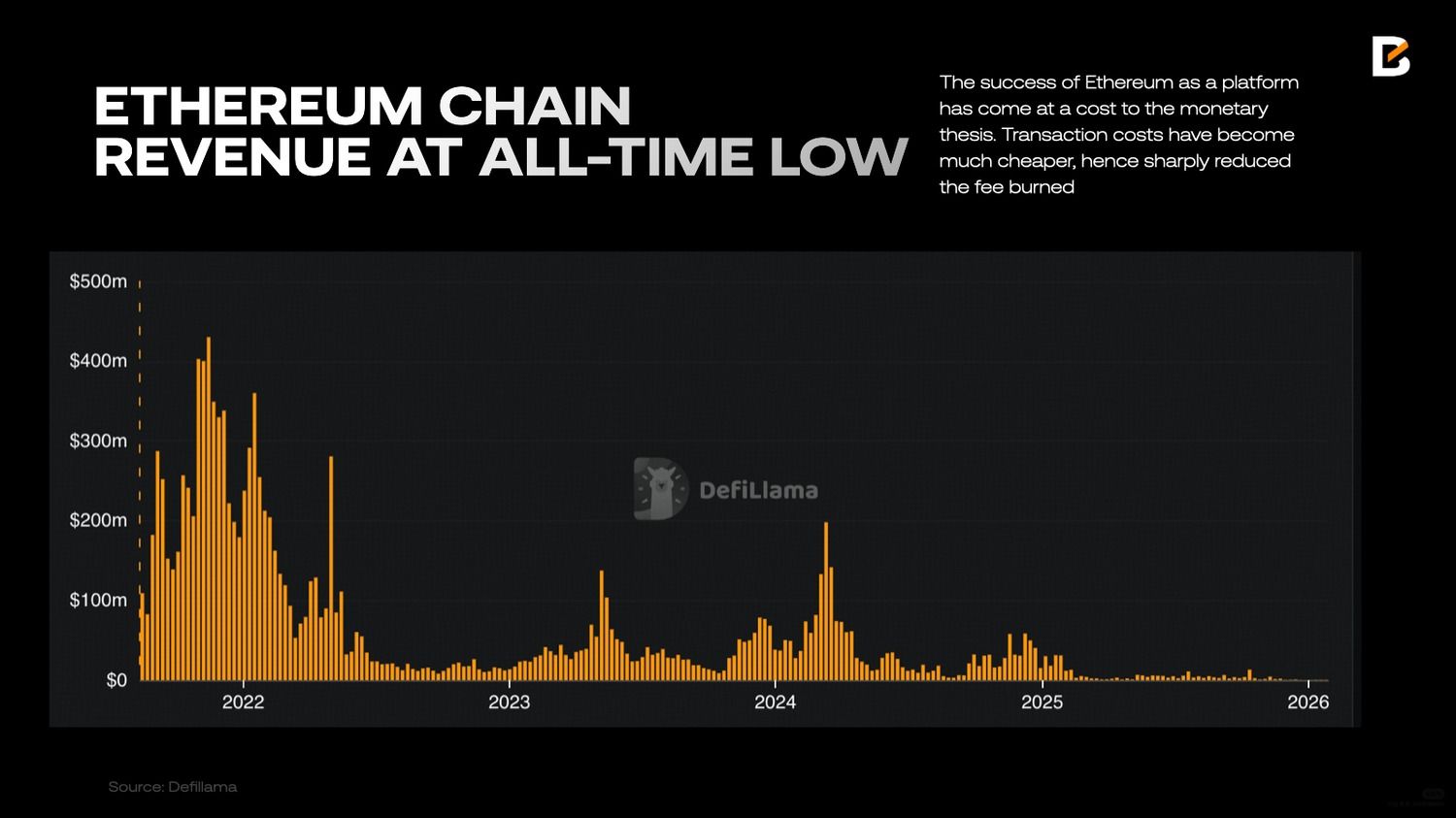

However, the success of Ethereum as a platform has come at a cost to the monetary thesis. Ethereum transaction costs have become much cheaper and more scalable. This has sharply reduced the fee burned. Adding to this is that most activity migrating to Layer 2s, ETH burn has fallen to the lowest level since the burning feature was introduced. As a result, the ETH supply has shifted back into inflation.

The divergence between Ethereum’s strength as a network and ETH’s performance as an asset has never been so large. One has to ask the important question: what is the current narrative for ETH as an asset?

We think there are two main narratives: 1) The “Digital Oil”; and 2) a “Yield-bearing productive asset” or “Institutional Treasury Staple”. Let’s evaluate both.

1) ETH remains best understood as digital oil, as the asset used to pay for computation on the network. However, commodity-like assets do not necessarily trend upward in price over the long run. Oil, despite being critical to the global economy, has largely traded in wide cyclical ranges. Its price is driven by demand cycle rather than scarcity.

2) In 2025, with the rising of companies treating ETH as a corporate treasury asset, a new narrative emerged, putting ETH as a yield-bearing productive asset, particularly attractive to institutional investors. Through staking, ETH generates native yield while offering exposure to the growth of an on-chain economy at the same time.

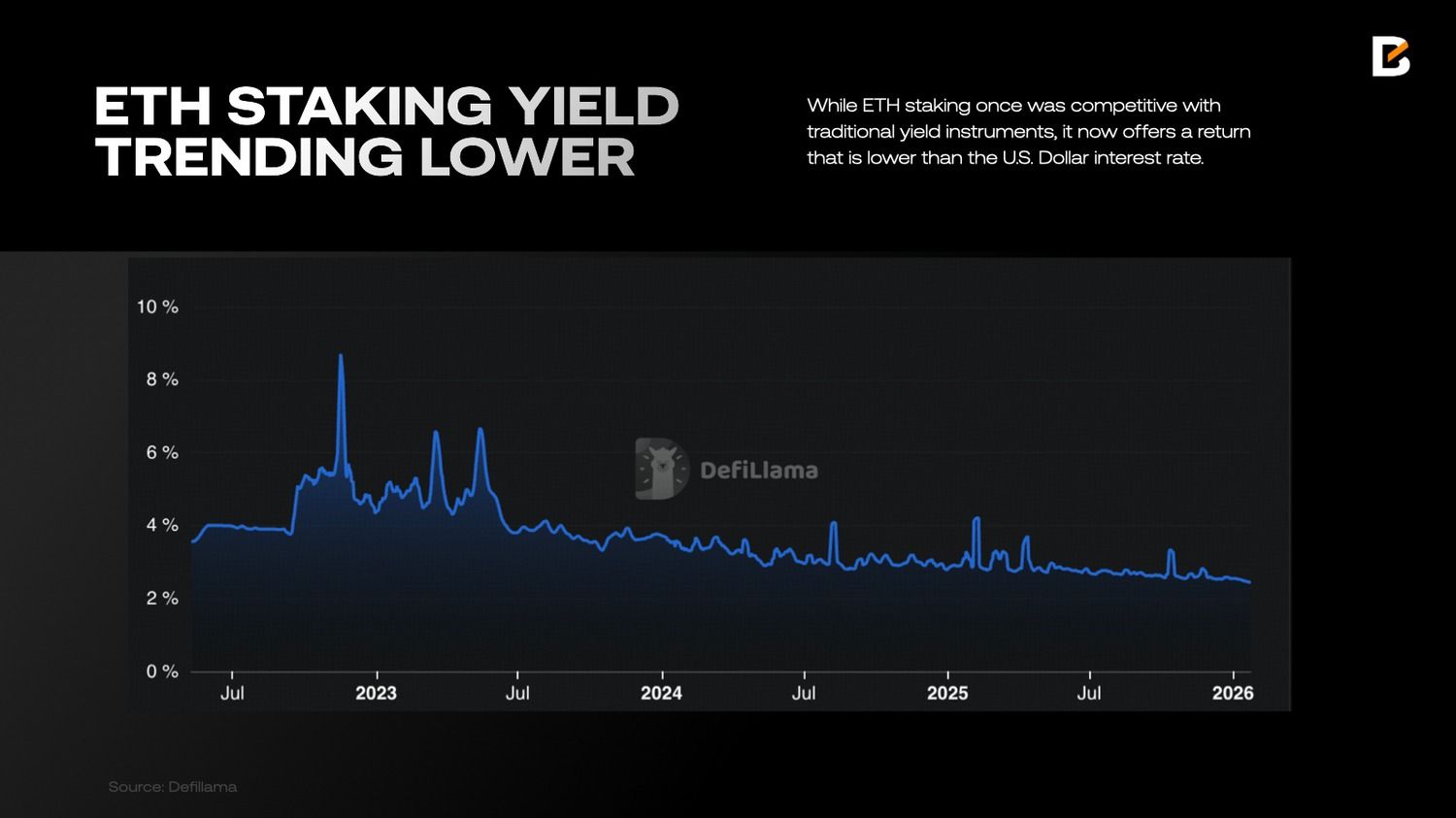

However, this yield-based thesis currently faces headwinds as well. Staking returns are closely tied to network revenue, which is largely driven by transaction fees. As Ethereum intentionally reduced gas cost on both Layer 1 and Layer 2, the ETH staking yield has trended lower. While ETH staking once was competitive with traditional yield instruments, it now offers a return that is lower than the U.S. Dollar interest rate.

Taken together, ETH is neither a store-of-value nor a high-yielding asset. It functions as a productive commodity with yield characteristics that fluctuate with network economics.

Layer-1 Smart Contract Platforms: A Purely Competitive Market

The Layer 1 blockchain landscape has become increasingly competitive. Major chains such as Ethereum, Solana, and XRP continue to play central roles, while a new wave of Layer 1s, often backed by institutions, has entered the market. Circle’s Arc, Tether-related Stable and Plasma, and Wall-street backed Canton are some prominent examples, with each one designed to optimize for specific functions around compliance, performance, or integration with traditional finance.

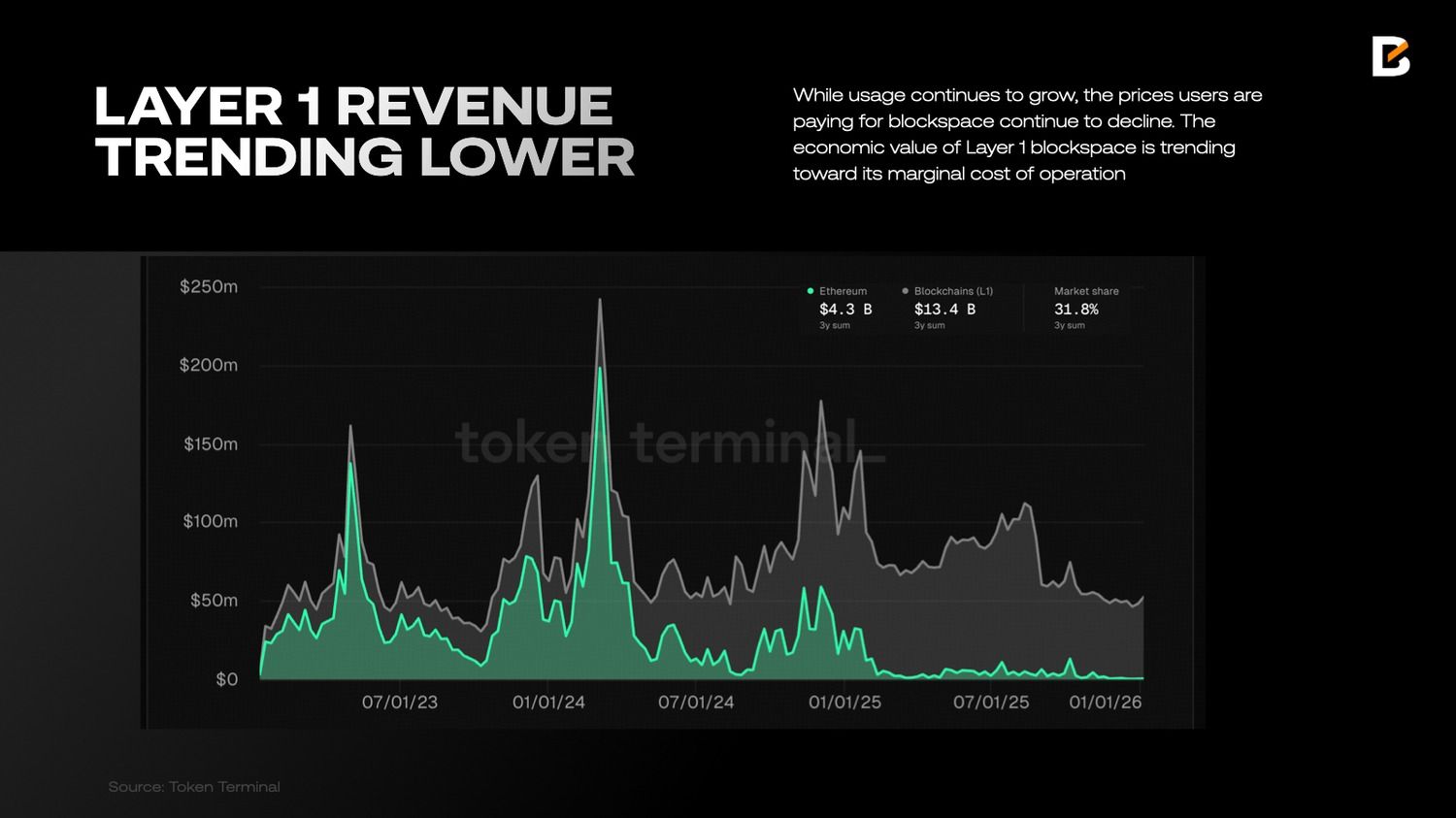

While Ethereum still maintains an advantage in decentralization, developer ecosystem, and network effect, most Layer 1s now compete aggressively on similar technical dimensions, block times, transaction throughput, and transaction cost. As a result, the economic value of Layer 1 blockspace is trending toward its marginal cost of operation.

According to data from Token Terminal, revenue across Ethereum and other Layer 1s has been trending lower. While usage continues to grow, the prices users are paying for blockspace continue to decline. This forces all Layer 1s to rely on ongoing token inflation to compensate validators and stakers in order to maintain network security.

From an economic perspective, the Layer 1 market now resembles a textbook case of perfect competition. The products are functionally similar and barriers to entry, while nontrivial, are low enough for new chains to emerge regularly. At the same time, users are increasingly abstracted away from the base layer through wallets or application interfaces.

An interesting analogy here is the stock exchange industry. The equity market in the U.S. is worth more than $60 trillion, with the vast majority of that value trading on the New York Stock Exchange and Nasdaq. Daily trading volumes reach hundreds of billions of dollars. At first glance, one might think that stock exchange is a lucrative business with high valuation.

The reality is quite the contrary. Intercontinental Exchange, the parent company of the NYSE, has a market capitalization of roughly $90 billion. Nasdaq’s parent company is valued at just over $50 billion. Combined, they are worth less than half of Ethereum’s current market capitalization.

The reason behind this is that exchange business models generate revenue through transaction fees. These are typically a tiny percentage of each trade’s value. And exchanges also face high competition. There are multiple trading venues beyond NYSE and Nasdaq, including alternative platforms like Cboe, dark pools, and electronic communication networks (ECNs), which pressure the overall transaction fee down, exchanges can’t charge high fees without losing business.

Like stock exchanges, Layer 1s provide essential settlement and coordination infrastructure. They enable enormous volumes of economic activity but operate in highly competitive environments where pricing power is limited. In this sense, the future of Layer 1 blockchains may look less like monopolistic technology platforms and more like competitive utilities: indispensable, widely used, and economically constrained by the very efficiency that makes them successful.

Privacy Coins: A Structural Comeback

In late 2025, privacy coins made a surprising return to the center of the crypto industry. The two largest privacy coins, Zcash and Monero, both recorded eye-catching returns in the past year. Their performance is especially interesting given that the broader crypto narrative is moving in a very different direction. In the 2024/2025 cycle, the crypto dominant theme has shifted away from censorship resistance and decentralization toward regulated stablecoins and real-world finance, both of which are largely centralized use cases. At the same time, Bitcoin is increasingly integrated into traditional finance and custodied by regulated financial institutions. Despite the industry drifting away from the original cyberpunk ethos, privacy remains a foundational human need, and as surveillance and compliance requirements intensify, the demand for privacy has not disappeared.

While the privacy sector is often treated as a single category, we believe it actually comprises two very different branches.

- Private Money: These are cryptocurrencies focused on private, censorship-resistant payments. The two most prominent examples are Zcash (ZEC) and Monero (XMR). Both use advanced cryptography to conceal transaction data, but a key difference lies in their privacy models: Monero enforces privacy by default for all transactions, while Zcash offers opt-in privacy through shielded addresses. Projects in this category are typically proof-of-work blockchains. They are competing with Bitcoin as a privacy-focused version of store-of-value assets.

- Programmable Privacy: A newer wave of Layer-1 blockchains is bringing privacy to decentralized applications by enabling confidential smart contracts and tokens. Examples include Digital Asset’s Canton Network and Cardano’s Midnight, both of which leverage technologies such as zero-knowledge proofs to support private code execution. Crucially, many of these platforms are designed for compliant confidentiality, allowing selective disclosure to regulators when required. They are competing with Layer 1 smart contract platforms such as Ethereum and Solana, which are now lacking privacy functions.

Why Zcash Is Better Positioned Than Monero

In the private money branch of the privacy sector, we favor Zcash over Monero. At a technical level, both use advanced cryptography to offer strong privacy, but differ meaningfully in how privacy is implemented. Monero enforces privacy by default, all transaction amounts, sender addresses, and recipient addresses are always obfuscated. Zcash, in contrast, adopts an opt-in privacy through its shield addresses, where users can choose between transparent and shielded transactions.

Uniquely, Zcash supports “view keys” for its shielded addresses, which are read-only keys that users can share with auditors or exchanges to selectively disclose their private transaction details for compliance or reporting purposes. This feature means Zcash users can prove specific transactions or balances to regulators or third parties without exposing their entire history, making Zcash’s privacy more compatible with institutional and legal requirements.

These technical differences have led to significant regulatory consequences. Monero has faced significantly far greater regulator scrutiny, with major centralized exchanges delisting XMR due to compliance concerns. On the contrary, Zcash is traded on most major crypto exchanges, including the most regulatory stringent one – Coinbase. This difference means Zcash can be accessed by a larger group of investors, and potentially can be considered by institution capital as an allocation choice.

The Case for Programmable Privacy

Fully transparent public ledgers are fundamentally incompatible with the traditional financial system. Financial institutions require confidentiality regarding balances, counterparties, pricing, and contractual terms, while also ensuring that all transactions comply with relevant regulations, including AML and other reporting requirements. Privacy-focused smart contract platforms address this demand that currently cannot be met by top Layer 1 chains such as Ethereum and Solana.

While this branch is still in its early development stage, market validation for this thesis is already visible, with Digital Asset’s Canton Network standing out as a leading example. The network has secured partnerships with major financial institutions, including the Depository Trust & Clearing Corporation (DTCC), Nasdaq, BNY, and Goldman Sachs. Privacy in the Canton Network is achieved using a special technical design. Each participating institution operates its own private ledger, where sensitive data is stored locally. These private ledgers are connected via a Global Synchronizer, forming a shared public ledger, which coordinates transactions without revealing underlying details to unauthorized parties.

Another notable example is Midnight, which launched in late 2025 and achieved a successful token debut, despite its ecosystem still being in an early stage of development.

Overall, as the industry shifts from retail-driven playgrounds toward institutionally led financial infrastructure, platforms that can reconcile confidentiality with compliance are well positioned to grow substantially.

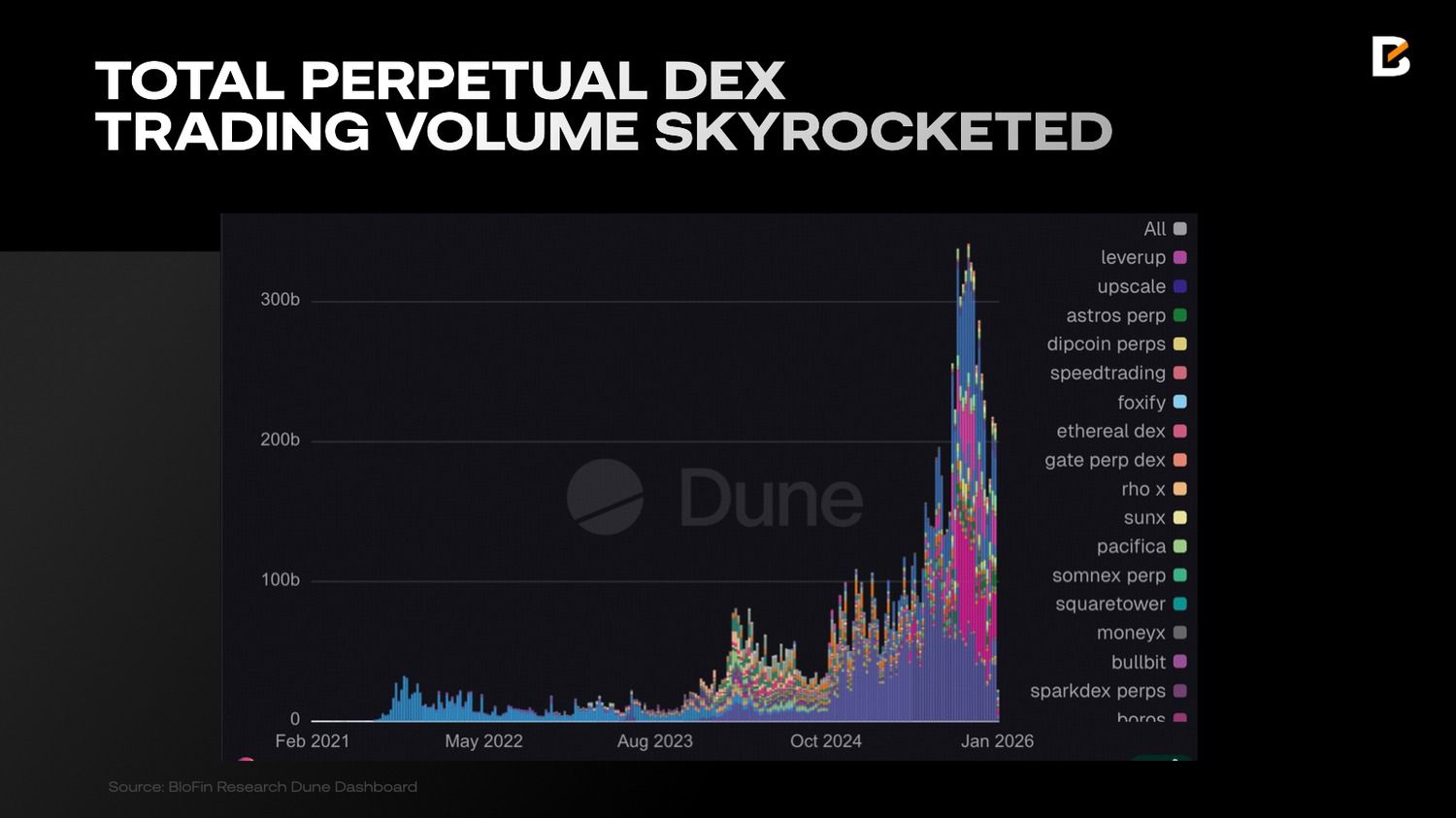

Perp DEX: Growth, Constraints, and the Path to Hybrid Markets

In 2025, Hyperliquid ignited the Perp DEX sector with weekly volumes surging from $81B in 2024 to $314.7B, while monthly volumes repeatedly broke $1T, making Perp DEXs the hottest sector in the crypto industry. This has also driven a wave of institutions starting to build their own PerpDEX: Amber has incubated EdgeX; Binance has introduced Aster and StandX; Revolut launched Extended; and Bain Capital alongside Sequoia India has backed Variational.

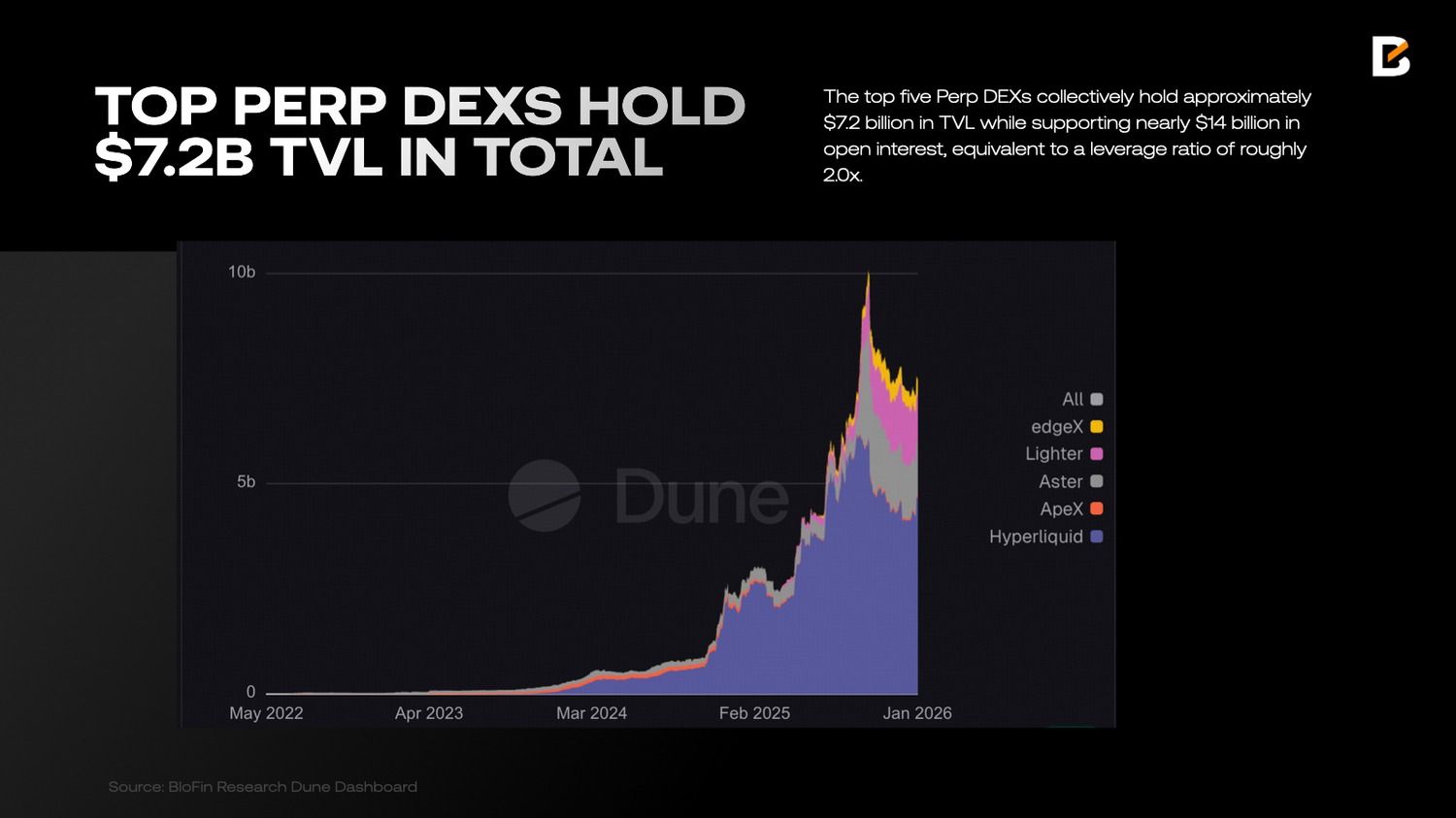

Despite the rapid expansion, PerpDEXs’ capital base remains structurally shallow. Data indicates that the top five Perp DEXs collectively hold approximately $7.2 billion in TVL while supporting nearly $14 billion in open interest, equivalent to a leverage ratio of roughly 2.0x. In contrast, Binance has more than $200 billion in parked and margin capital against around $30 billion in OI. This disparity reflects a difference in risk-absorption capacity.

We believe that Perp DEXs will not displace CEXs as the primary trading venue in the near term for the following reasons:

- Auto-Deleveraging (ADL) Risk: The leverage ratio of mainstream Perp DEXs sits around 2.0x (with some emerging protocols exceeding 3.0x). In periods of extreme market volatility, this poses a high risk of triggering ADL or insolvency, as the protocol’s TVL is too thin relative to the outstanding Open Interest.

- Cross-Margin Capabilities: CEXs can seamlessly provide Unified Margin accounts across multiple assets and products (Spot, Futures, and Options). Instead, DEXs are hindered by the complexities of cross-chain protocols and liquidity fragmentation, making it difficult for users to efficiently manage collateral across multiple markets within a single interface.

- Low-Latency Matching: While Hyperliquid has significantly reduced latency, they still cannot compete with the microsecond-level matching engines of centralized exchanges. For HFT and institutional-sized orders, CEXs maintain a definitive advantage in slippage control and order book depth.

- Fiat On/Off-Ramp Accessibility: CEXs remains the primary global gateway for fiat currency entering the crypto ecosystem. For the vast majority of new capital, the path to purchase assets via bank transfers or P2P services on platforms like CEXs is significantly shorter and more user-friendly.

Current Performance

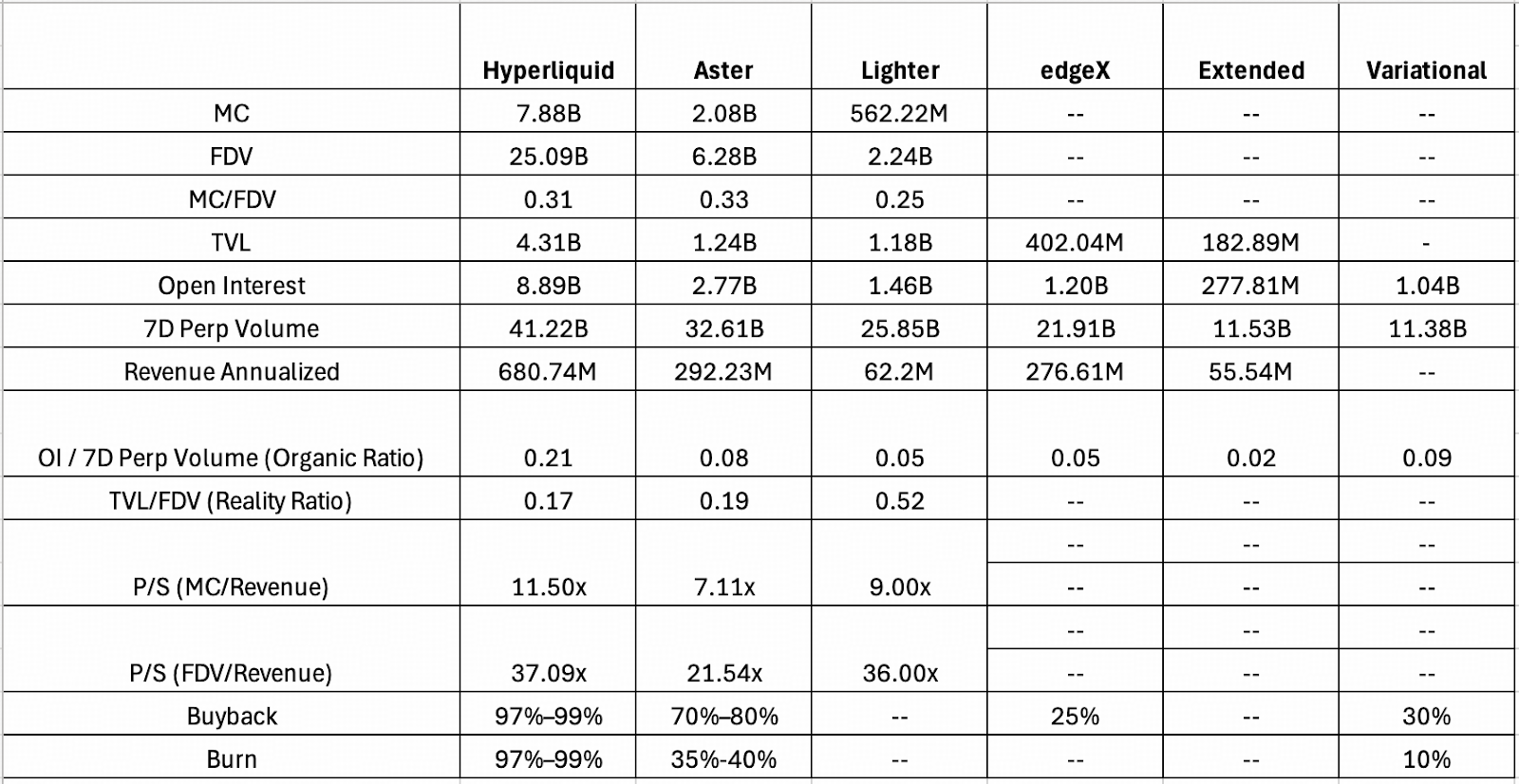

Key performance metrics have been compiled across six leading perpetual DEXs. To evaluate whether a project’s activity reflects organic demand or incentive-driven volume, the analysis focuses on the OI-to-7-day volume ratio, open interest relative to recent trading turnover. A higher ratio implies stronger capital efficiency and a greater share of organic positioning, while low readings tend to coincide with wash trading and points-driven farming.

Hyperliquid remains the clear benchmark, posting an OI/7d Volume ratio of 0.21. By comparison, pre-token protocols such as EdgeX, Extended, and Variational register materially lower ratios, consistent with heavy airdrop-driven activity. Extended is the most extreme case, with a ratio of just 0.02, indicating that the majority of its volume is likely wash trading. Variational, however, presents a more nuanced picture. Its ratio of 0.09 exceeds EdgeX (0.05) and Aster (0.08), suggesting a higher share of real positioning despite still operating within a points-farming environment. On this basis, Variational appears relatively underpriced in the points market and may represent an opportunity for participants targeting outsized airdrop outcomes.

From a revenue perspective, Lighter continues to lag Hyperliquid and Aster. This gap is largely structural. Lighter’s zero-fee retail model eliminates taker-side revenue, leaving the protocol almost entirely dependent on maker fees paid by market makers and Lighter Liquidity Pool. This dynamic helps explain its relatively elevated TVL/FDV ratio of 0.52, a proxy for how much real capital is backing each dollar of implied valuation.

In terms of fundamentals, Lighter’s valuation appears reasonable: roughly $0.52 of locked assets support every $1 of market value. However, revenue-based metrics tell a more constrained story. Both the P/S multiple and annualized revenue suggest that the market is already pricing in optimistic growth assumptions, especially when benchmarked against Aster. The limiting factor remains revenue efficiency. Compared with Hyperliquid and Aster, Lighter generates materially less revenue per unit of TVL, which in turn places a hard ceiling on its achievable FDV.

The perpetual DEX landscape has become increasingly commoditized. In an effort to gain market share, newer entrants such as Extended, Lighter, and Variational have converged toward near-zero retail fees. While this improves short-term user acquisition, it also compresses protocol revenue and weakens the effectiveness of buyback-and-burn token models. Unlike Hyperliquid, whose strong cash flow materially reinforces token value, most emerging Perp DEXs lack the revenue base needed to support aggressive value accrual mechanisms.

| Scenario | Logic / Benchmark | Reality Ratio | Estimated FDV |

| Bearish | Lighter (High Asset Backing) | 0.52 | ~$773M |

| Base | Tier-2 Market Average | 0.35 | ~$1.15B |

| Optimistic | Aster (Market Premium) | 0.19 | ~$2.12B |

As a result, FDVs across the sector appear structurally capped, with TVL/FDV ratios remaining elevated. Using Lighter’s 0.52 ratio as a reference point, EdgeX’s eventual launch valuation may struggle to exceed the $1 billion threshold under current market conditions.

Perp DEX in 2026

Looking toward 2026, the convergence between on-chain and off-chain finance will continue to deepen. Perpetual DEXs are unlikely to replace centralized exchanges outright. Instead, they are evolving into a complementary layer, with their core value centered on transparent, auditable liquidation and risk management.

- From Trading Tools to Trading Ecosystems

At present, leading platforms such as Hyperliquid operate with very high effective leverage, reflecting a user base dominated by high-risk, incentive-driven on-chain traders. Friction in fiat on- and off-ramps, alongside still-maturing infrastructure, has limited broader adoption beyond crypto-native traders. Breaking through this ceiling will require a shift in product positioning. Rather than functioning purely as execution venues, Perp DEXs will need to develop into integrated ecosystems, prioritizing user experience, capital efficiency, and operational stability in order to attract lower-cost, more persistent institutional capital.

- The Emergence of Hybrid Market Infrastructure

CEXs are increasingly approaching decentralized protocols less as competitors and more as infrastructure complements. From a first-principle perspective, derivatives traders consistently prioritize asset custody, liquidation transparency, and risk isolation. As a result, the strategic direction for major CEXs is gradually shifting toward hybrid architectures, where on-chain perpetual protocols are embedded into centralized trading stacks. This approach allows exchanges to leverage on-chain transparency while retaining the execution performance and capital efficiency of CEXs.

- The Expansion into RWA Perpetuals

Another structural inflection expected in 2026 is the expansion of perpetual markets into RWA. As the scope of eligible underlyings broadens, RWA derivatives are beginning to fill gaps in traditional markets. Hyperliquid’s introduction of Ventuals under HIP-3, designed to support pre-IPO trading, illustrates this trend by addressing the absence of perpetuals in stock market. Extending the perpetuals to equities and other RWA categories is likely to become a key growth driver for trading platforms, reshaping how global derivatives markets are accessed and structured.

Prediction Market: From Fringe Experiments to Probabilistic Infrastructure

By 2025, prediction markets had largely completed their shift from a peripheral experiment to a meaningful component of financial infrastructure. The turning point was the aftermath of 2024 U.S. presidential election. During the election, platforms such as Polymarket demonstrated a consistent edge over traditional polling firms and media commentary, both in timeliness and directional accuracy.

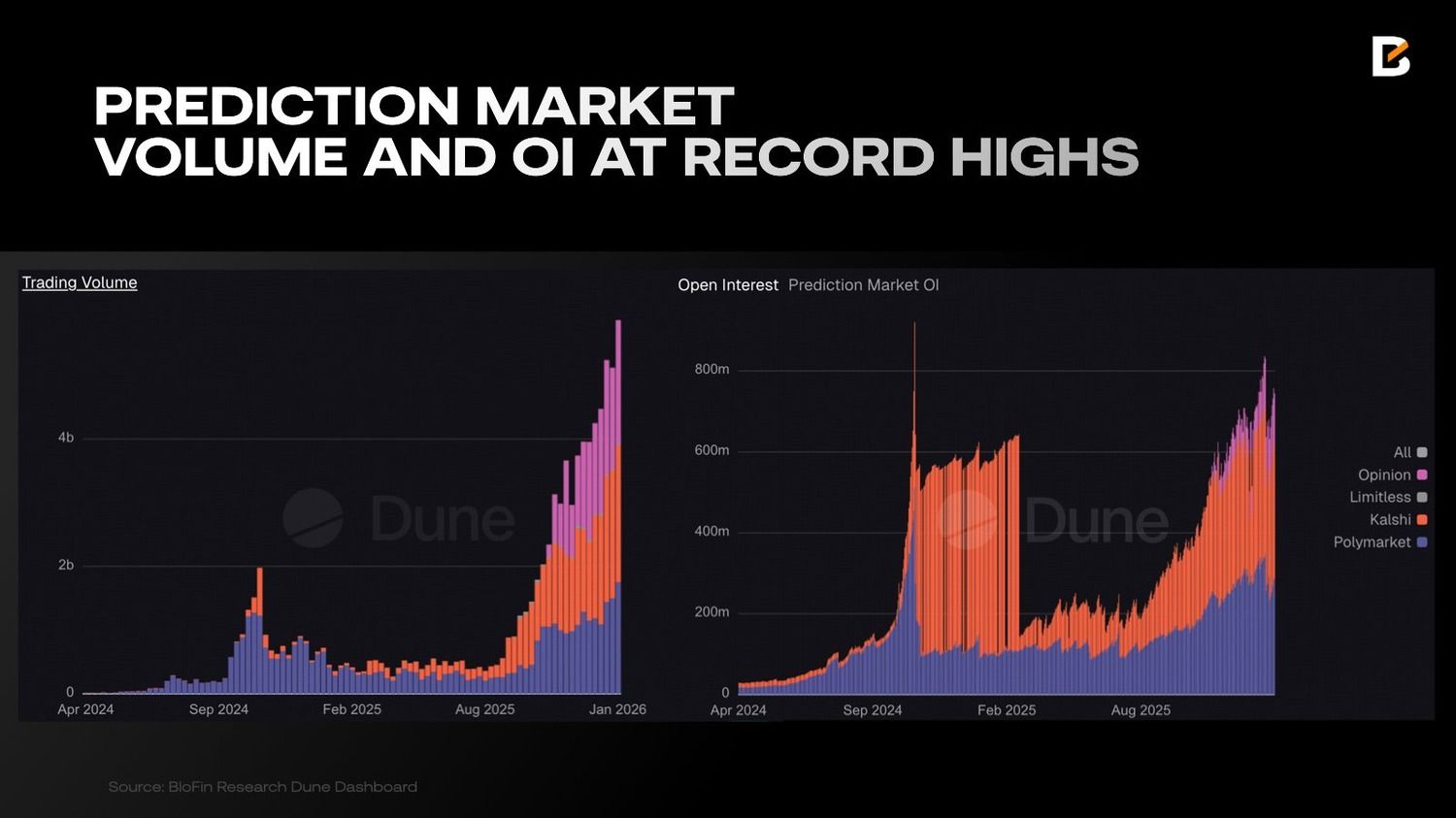

The prediction market landscape is becoming increasingly concentrated. Polymarket and Kalshi now dominate the sector, with combined weekly trading volumes exceeding $3.5 billion and aggregate open interest surpassing $620 million. At this scale, prediction markets are no longer peripheral instruments; they are influencing how expectations are priced across political, economic, and social outcomes.

The Competitive Edge of Prediction Markets:

- Superior Accuracy: Multiple independent backtests indicate that prediction market prices tend to outperform traditional tools such as phone-based polling and expert surveys. Because prices continuously incorporate dispersed information, they often converge on outcomes earlier than conventional methods. As a result, prediction market data has increasingly become a reference point for mainstream media and institutional observers.

- Unstructured Exposure: Prediction markets allow users to invest in or hedge against “unstructured” events and real-world outcomes that lack standardized financial instruments.

- P2P Transparency vs. Opaque House Odds: Unlike traditional bookmakers, where odds are calculated internally and the counterparty is often hidden, prediction markets are built on a peer-to-peer architecture. This shift ensures market-driven pricing and fundamental fairness.

The Mechanism Issue

These unique advantages offer a new frontier for trading, positioning prediction markets to potentially disrupt the traditional gambling industry. The institutional pivot is already well underway. On December 19, 2025, DraftKings, a top US online sports betting platform, launched its proprietary prediction market. Its primary rival, FanDuel, followed suit within the same month through a strategic partnership with the CME Group.

Despite this positive expansion, PMs still face significant structural hurdles, most of which are rooted in their reliance on binary contract mechanics.

- Lack of Outcome Continuity: Current PMs operate on an “All or Nothing” basis. Much like binary options, they settle at either 0 or 1. While this format answers “yes or no,” it fails to capture the continuity. The lack of granularity often forces platforms to launch multiple, fragmented markets just to simulate a continuous range of outcomes.

- The Market Maker Dilemma: The extreme volatility inherent in binary outcomes makes market making exceptionally difficult. As a market nears settlement, prices can snap violently toward 0 or 1. Without effective derivatives to hedge the cliff-edge risk, MMs are often reluctant to provide depth, specifically leading to poor liquidity for long-tail markets.

- Low Capital Efficiency: Under current designs, capital is typically locked in smart contracts until the event is settled. For events spanning months, this represents a massive opportunity cost as the capital remains idle and non-interest-bearing. This friction has historically deterred institutional entry. To mitigate this, some markets have begun offering fixed APR incentives on event positions to compensate for the lack of capital turnover.

- Semantic Incompatibility: Liquidity is currently siloed due to a lack of standardization. For instance, an “A wins” contract on one platform and a “B loses” contract on another are fundamentally different. This semantic non-fungibility prevents the pooling of liquidity across the broader ecosystem.

- Underdeveloped Derivative Tooling: In mature financial markets, traders can bet on both direction and volatility. In the current PM landscape, users are largely limited to directional “Yes” or “No” bets. The absence of sophisticated tooling means there is no efficient way to trade the volatility of an event without picking a side.

Predication Market in 2026

The Prediction Market sector is currently prioritizing solutions for long-standing frictions: cross-chain liquidity, sophisticated derivatives, hedging mechanisms, and capital efficiency. In 2026, we expect the PM landscape to reach full maturity, supported by the following pillars:

- AI Agent Trading: Because PM outcomes are hyper-sensitive to news, they offer significant news-trading opportunities. AI agents like Polybro and Alphascope specialize in identifying sentiment and executing trades with a speed and accuracy that manual traders cannot match.

- Next-Gen Terminals & Execution Bots: Institutional-grade terminals now offer consolidated market data, deep analytics, and multi-platform execution triggers. Betmoar has emerged as the dominant player in this space, with trading volumes reaching $970 million.

- On-Chain Intelligence & Monitoring: Tools such as Polysights and PolyAlertHub function as the “Nansen of Prediction Markets,” providing transparency into Smart Money flows, whale positioning, and potential insider activity.

- Arbitrage & Structured Funds: Tools like ArbBets now support automated arbitrage between platforms like Polymarket and Kalshi, while PolyFund has introduced decentralized fund structures to the space.

- Unified Infrastructure & APIs: Developers are increasingly utilizing standardized data interfaces like Dome, which allows for the rapid deployment of custom trading tools and cross-platform integrations.

Prediction markets are gradually entering the mainstream. An increasing number of traditional information and data institutions are beginning to treat probability pricing from prediction markets as an important reference signal for assessing macro-level events. Institutions such as Google News, Yahoo Finance, and Bloomberg have, to varying degrees, started to monitor and cite prediction market probabilities when evaluating political, economic, and broader public outcomes.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

Recommended Articles