Japan: Yen Likely to Rise or Stabilise, Unlikely to Fall, with High Odds for Bulls

Executive Summary

TradingKey - We anticipate a high likelihood of the Japanese yen appreciating in the short term (0-3 months). This outlook is driven by two key factors: First, the diverging monetary policies of the U.S. and Japan (Federal Reserve rate cuts paired with Bank of Japan rate hikes) will support the yen against the U.S. dollar. Second, Japanese bond yields are expected to remain relatively elevated, further bolstering the yen's exchange rate. In the medium term (3-12 months), the yen is likely to enter a period of stability against the dollar. Historically, significant yen appreciation against the dollar has required one of the following conditions: 1) a U.S. economic recession; 2) a sharp decline in U.S. inflation; 3) substantial Federal Reserve rate cuts; or 4) a global crisis amplifying the yen’s safe-haven appeal. Looking ahead, as these conditions are unlikely to materialise, sustained yen appreciation appears improbable. In summary, the Japanese yen will initially appreciate against the US dollar before stabilizing.

Source: TradingKey

* Investors can directly or indirectly invest in the foreign exchange market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Recent Forex Trends

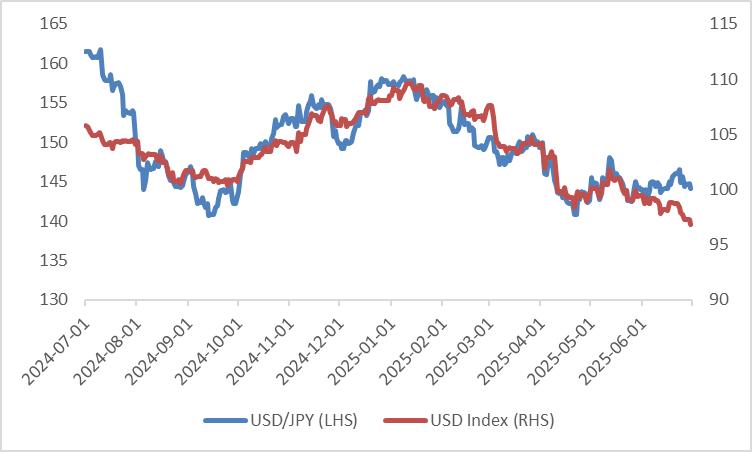

From the start of this year until early May, the Japanese yen steadily appreciated. This was primarily driven by the weakening of the U.S. dollar index, influenced by Trump’s tariff policies and the global trend toward de-dollarisation, which indirectly bolstered the yen (Figure 1). However, since May, the yen has entered a relatively stable phase against the dollar due to a combination of factors: narrowing yield spreads between U.S. and Japanese government bonds, delayed expectations for Bank of Japan rate hikes, the signing of a U.S.-UK agreement, and easing U.S.-China tensions. Looking ahead, will the yen continue to fluctuate within a range, or will it embark on a unilateral trend? Our analysis concludes that in the short term (0-3 months), the yen is highly likely to appreciate. In the medium term (3-12 months), however, the yen is expected to stabilise against the dollar. The detailed analysis follows.

Figure 1: USD/JPY and USD Index

Source: Refinitiv, TradingKey

* For related information, refer to the article published on 1 July 2025, titled ““Golden July” for the Yen? Market Bets on JPY Strength — Could USD/JPY Return to 140?”

2. Short-Term Forex Outlook

In the short term, we are bullish on the Japanese yen, driven by two key factors. First, the divergence in U.S. and Japan monetary policies. Elevated rice prices and persistent inflation in the services sector have driven both Japan’s headline and core CPI well above the Bank of Japan’s 2% target. This high inflation has already begun to weigh on Japan’s economic growth, resulting in negative real GDP in the first quarter. Looking ahead, however, sustained wage growth is expected to boost aggregate demand, fostering a virtuous demand-inventory cycle. This should help Japan’s economic growth turn positive in the coming quarters. Against a backdrop of robust growth and elevated inflation, we anticipate the Bank of Japan will continue to raise interest rates, supporting the yen’s appreciation against the U.S. dollar.

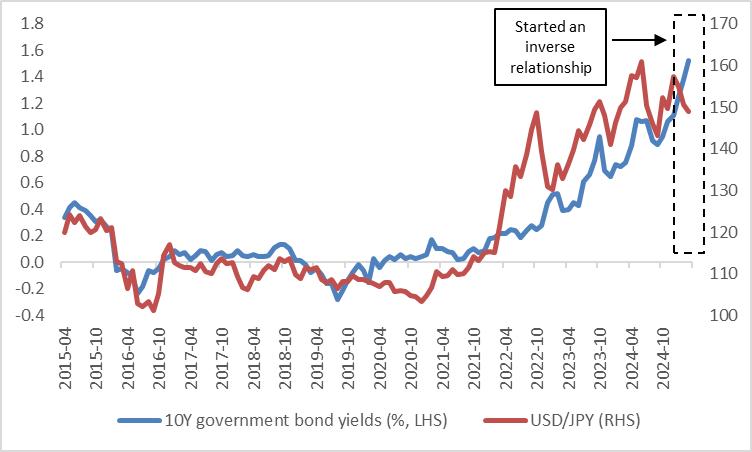

Second, the normalisation of monetary policy is expected to sustain elevated Japanese government bond (JGB) yields. In theory, higher yields attract foreign capital inflows, improve economic expectations, and shift risk preferences, thereby supporting yen appreciation. Over the past decade, however, the correlation between JGB yields and the yen’s exchange rate has been weak, and at times contrary to theoretical expectations, due to the Bank of Japan’s prolonged negative interest rate policy. With the end of negative rates, Japan’s market dynamics have realigned with theoretical models (Figure 2). Looking forward, elevated JGB yields are likely to further drive the yen’s appreciation.

Figure 2: Japan Government Bond Yields and USD/JPY

Source: Refinitiv, Tradingkey.com

3. Mid-Term Forex Outlook

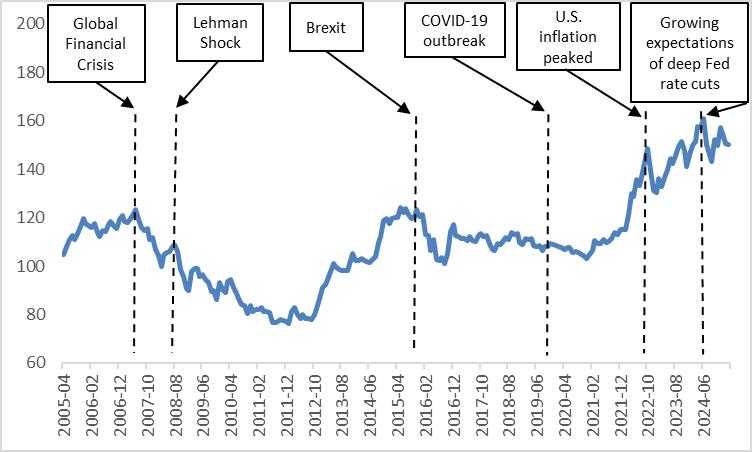

Will the Japanese yen sustain significant appreciation in the medium term? Historically, substantial yen appreciation against the U.S. dollar has required one of the following conditions: 1) a U.S. economic recession; 2) a sharp decline in U.S. inflation; 3) significant Federal Reserve rate cuts (all of which weaken the dollar); or 4) a global crisis amplifying the yen’s safe-haven appeal (Figure 3). Looking ahead, the U.S. and global economies are expected to slow but not enter a recession. As these conditions are unlikely to materialise, sustained yen appreciation appears improbable. Furthermore, in the medium term, a weaker U.S. economic outlook will dampen global growth. As both the dollar and the yen are safe-haven currencies, a global economic slowdown is likely to support both, leading to a stable yen-dollar exchange rate within a range.

Figure 3: External Factors Caused the Yen to Sharply Appreciate

Source: Refinitiv, TradingKey

* For further details supporting our foreign exchange market views, please refer to the macroeconomic section below.

4. Macroeconomics

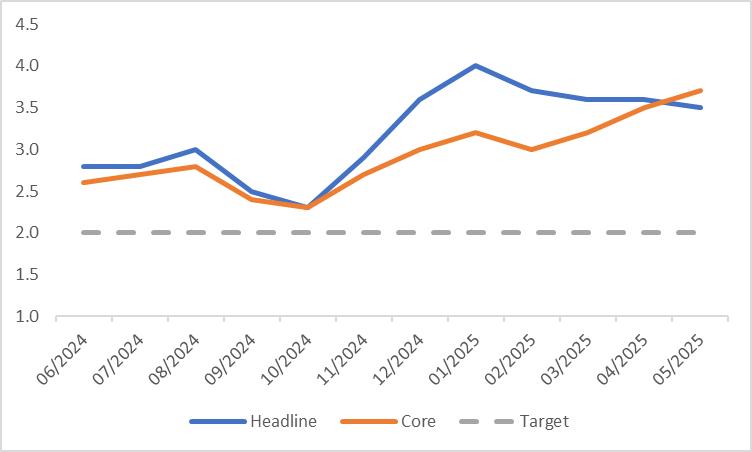

Japan’s economy currently faces its greatest challenge in the form of high inflation. Regarding headline CPI, although this inflation metric has eased from 4% earlier this year, the latest May reading remains elevated at 3.5%, well above the Bank of Japan’s 2% target. The primary driver is the soaring price of rice, which has more than doubled compared to the previous year despite government measures such as releasing emergency rice reserves and reforming distribution systems. Meanwhile, core CPI, which excludes energy and food, has been rising steadily since February (Figure 4.1). This increase is largely attributed to wage growth driving up prices in the core services sector.

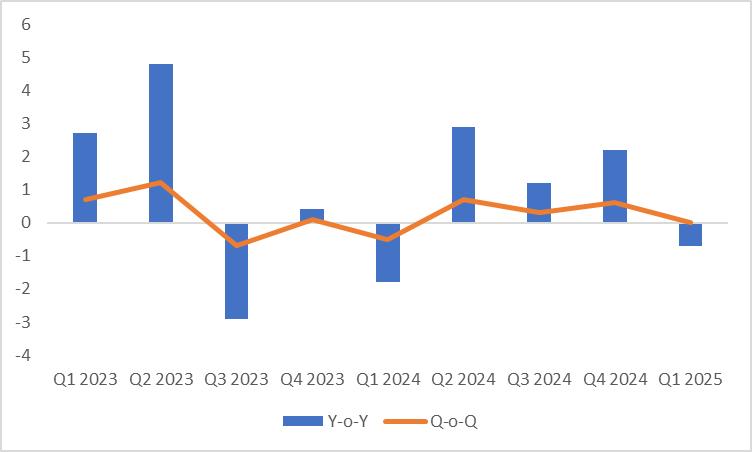

High inflation has significantly impacted Japan’s economic growth. Despite rising private sector incomes, personal consumption has declined by 0.5%, driven by concerns over persistent price increases and future uncertainties. Additionally, weak global demand, coupled with trade tensions, has led to a recent decline in Japanese exports. Combined with manufacturing slowdowns and reduced investment, these factors contributed to negative year-on-year real GDP growth in the first quarter (Figure 4.2). Looking ahead, we remain optimistic about Japan’s macroeconomic outlook. Continued government releases of emergency rice reserves are expected to ease inflationary pressures. Coupled with sustained wage growth, this should boost real household incomes. Rising incomes will support increased aggregate demand, sustaining the inventory replenishment cycle. Through this virtuous demand-inventory cycle, Japan’s economic growth is projected to turn positive in the coming quarters.

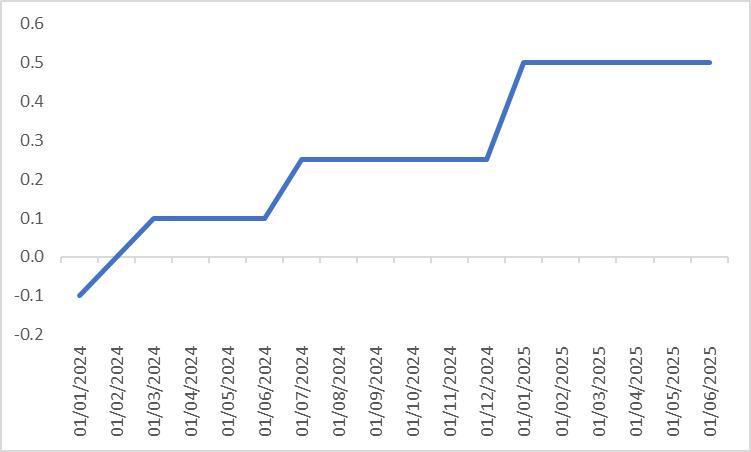

Since the Bank of Japan (BoJ) ended its negative interest rate policy in March 2024, it has raised rates by a total of 60 basis points (Figure 4.3). On 17 June 2025, the BoJ maintained its policy rate at 0.5% and announced a reduction in its balance sheet runoff pace from ¥400 billion per quarter to ¥200 billion per quarter starting April 2026. While this measure appears dovish, we believe it is unlikely to persist. Given inflation remains above the target and the relatively positive economic outlook, we expect the BoJ to shift to a hawkish stance, resuming its rate-hike cycle in the third or fourth quarter of 2025.

Figure 4.1: Japan CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 4.2: Japan Real GDP (%)

Source: Refinitiv, TradingKey

Figure 4.3: BoJ Policy Rate (%)

Source: Refinitiv, TradingKey

Recommended Articles