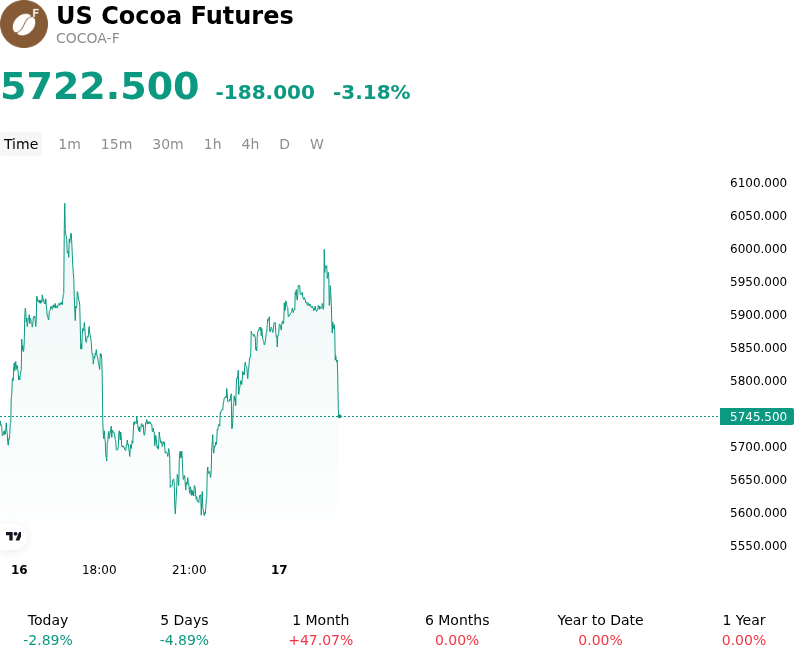

US Cocoa Futures (COCOA-F) Volatility Intensified on Jul 16: What to Watch

US Cocoa Futures (COCOA-F) is down 3.18% at Jul 16 05:20(ET), now at $5722.5, with a 7-day down of 10.03%.

What is driving US Cocoa Futures (COCOA-F)’s stock price down today?

The downward pressure on cocoa futures is primarily attributed to a significant improvement in growing conditions across West Africa, specifically within the Ivory Coast and Ghana. Recent satellite data and regional reports indicate that consistent rainfall and optimal temperatures have bolstered the development of the mid-crop, alleviating prior concerns regarding supply shortages. This shift in weather patterns has prompted a reassessment of the global supply deficit, which had previously underpinned record-high valuations.

On the demand side, institutional investors are reacting to signs of price elasticity within the confectionery sector. Emerging data from major grind processors suggests a contraction in cocoa processing volumes as manufacturers pass higher raw material costs to consumers. This demand destruction is becoming more evident in quarterly earnings reports, leading market participants to adjust their long-term consumption forecasts downward. The cooling demand, coupled with the anticipation of a stronger harvest, has triggered a wave of long liquidation by hedge funds and commodity trading advisors who are now de-risking their portfolios.

Technical factors are also playing a role as the market breaches key support levels. The increased margin requirements and high volatility observed over the preceding months have reduced overall liquidity, making the market more susceptible to sharp corrections when supply-side fundamentals turn bearish. Furthermore, reports of increased port arrivals in San Pedro and Abidjan have provided physical evidence that the logistical bottlenecks seen earlier in the season are beginning to clear, further easing immediate supply constraints.

Market participants are now closely monitoring the preliminary outlook for the next main crop cycle. While structural issues such as tree aging and disease remain long-term concerns, the immediate focus has shifted to the favorable moisture profile across the cocoa belt. Unless there is a significant reversal in weather patterns or a renewed escalation in geopolitical risks affecting shipping routes, the market appears to be transitioning into a phase of price consolidation as the extreme supply-side risk premium continues to erode.

More details about US Cocoa Futures (COCOA-F)

Recent Events and Risks:

- Improving West African Growing Conditions: Recent heavy rainfall across key cocoa-producing regions in Ivory Coast and Ghana has improved soil moisture levels for the upcoming 2024/25 main crop, prompting a wave of technical selling as the outlook for mid-term supply availability shifts from critical to stable.

- Evidence of Demand Destruction: Quarterly grinding data and analyst reports indicate a significant contraction in cocoa processing volumes in Europe and North America, suggesting that record-high terminal prices have finally triggered substantial industrial demand destruction and consumer pushback.

- Narrowing Port Arrival Gaps: Latest data from Ivorian exporters show that the year-on-year deficit in port arrivals is narrowing more quickly than anticipated, leading market participants to reassess the severity of the current season's supply shortfall and increasing pressure on long-positioned speculators.

- Liquidity and Margin Stress: Persistently high margin requirements and reduced open interest on the ICE exchange have created a low-liquidity environment, making the market highly vulnerable to "flash" downside volatility and forced liquidations if key technical support levels are breached.

Recommended Articles