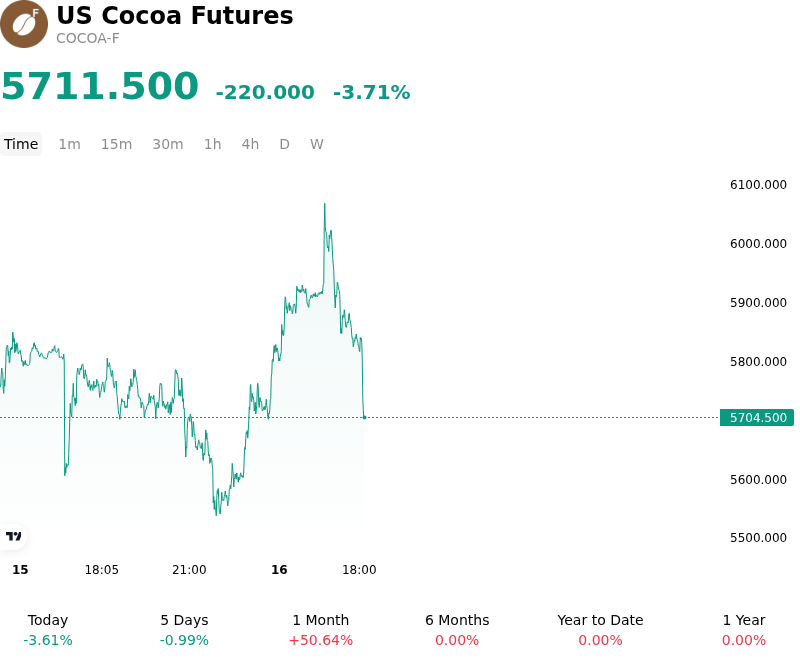

US Cocoa Futures (COCOA-F) Volatility Intensified on Jul 15: What to Watch

US Cocoa Futures (COCOA-F) is down 3.71% at Jul 15 06:10(ET), now at $5711.5, with a 7-day down of 5.35%.

What is driving US Cocoa Futures (COCOA-F)’s stock price down today?

The downward pressure on cocoa futures is primarily driven by improved weather conditions in West Africa, which have significantly bolstered the outlook for the 2026/27 main crop. Recent precipitation patterns across key growing regions in Ivory Coast and Ghana have alleviated concerns over soil moisture deficits, leading to a higher-than-expected forecast for pod development. This shift in the supply outlook follows a period of historical tightness, suggesting that the structural deficits observed in previous seasons may finally be easing as production levels normalize.

Concurrent with the favorable weather reports, the market is reacting to preliminary second-quarter cocoa grind data, which serves as a critical proxy for global demand. The figures indicate a sharper-than-anticipated contraction in processing volumes across Europe and North America, signaling that the high price environment of the past year has finally triggered meaningful demand destruction. Manufacturers appear to be optimizing inventories and reducing throughput as retail consumer resistance to higher chocolate prices begins to materialize in volume sales data.

Institutional capital flows have exacerbated the price retreat as hedge funds and commodity trading advisors accelerate the liquidation of long positions. The technical breakdown below key psychological support levels has triggered automated sell orders, further depressing prices in a market that had been heavily positioned for continued scarcity. As port arrivals in San Pedro and Abidjan show a steady recovery compared to the same period last year, the urgency for commercial hedgers to maintain long coverage has diminished.

The combination of a stabilizing supply chain and waning demand momentum suggests a transition toward a more balanced global market. While long-term structural issues such as aging tree stocks and crop diseases remain a background concern, the immediate focus of market participants has shifted toward the bearish implications of the upcoming harvest and the softening of the premium previously baked into the forward curve. Investors are now closely monitoring the next round of official crop estimates to determine if the current correction represents a temporary pullback or the beginning of a broader cyclical downturn.

More details about US Cocoa Futures (COCOA-F)

Recent Events and Risks:

- Favorable West African Weather Patterns: Recent reports of increased rainfall and improved soil moisture across key growing regions in Ivory Coast and Ghana are easing immediate supply concerns for the mid-crop and the 2024/25 main crop, potentially triggering a bearish price correction as the extreme supply deficit narrative softens.

- Accelerating Demand Destruction: Sustained high prices are leading to significant demand deterioration, with chocolate manufacturers reporting reduced processing volumes and a shift toward cocoa substitutes, which threatens a sharp decline in global grinding figures over the coming quarters.

- Market Liquidity and Margin Stress: Extreme intraday volatility has led to elevated margin requirements on the ICE exchange, causing a sharp reduction in open interest and leaving the market vulnerable to erratic, liquidity-driven price swings as commercial participants and hedge funds reduce their exposure.

- EUDR Implementation Uncertainty: While a delay to the EU Deforestation Regulation has been proposed, the lack of a finalized timeline and clear certification protocols is creating logistics bottlenecks and uncertainty regarding the deliverability of existing stocks into European warehouses, heightening spot price risk.

Recommended Articles