Today’S Market Recap: Dow Jones Closes Higher, Nasdaq Falls over 1%, Chip Stocks Plunge Nearly 6%, Market Awaits Warsh "Debut"

Tracking the Market Trend

TradingKey - On June 16, Eastern Time, the new Federal Reserve Chair, Wash, will preside over his first monetary policy meeting since taking office. Combined with Japan’s interest rate hike, which has put pressure on carry trades, the U.S. stock market is marked by a strong sense of caution. The three major indices closed with mixed results, with only the Dow Jones Industrial Average posting a gain. Tech stocks led the declines, while the consumer and financial sectors bucked the trend and posted gains.

At the close, the Dow Jones Industrial Average rose 0.64% to 51,999.67; the Nasdaq Composite fell 1.15% to 26,376.34; and the S&P 500 fell 0.57% to 7,511.35.

In terms of sectors and individual stocks, the Philadelphia Semiconductor Index closed down nearly 6%. Intel (INTC) fell more than 8%, and AMD (AMD) dropped over 7%. SpaceX (SPCX), in its third trading day, rose sharply before pulling back; it briefly touched $225.64 during the session and ultimately closed up nearly 5%, surpassing Amazon (AMZN) in market capitalization. AI infrastructure-related stocks came under pressure, with Lumentum (LITE) falling more than 8%.

In the commodities market, the prospect of the Strait of Hormuz reopening continued to weigh on oil prices. Crude oil futures fell for the fourth consecutive trading day, with Brent crude dropping below the $80 mark for the first time in more than three months. During the session, WTI (CL) fell nearly 6.5% at one point, while Brent (BZ) fell nearly 6%. In the precious metals market, gold’s rally moderated somewhat, with COMEX gold futures (GC) posting their third consecutive gain and closing at a more than one-week high.

Market Headline

The Bank of Japan raised its policy rate to 1%, the highest level since 1995, and announced it would suspend its balance sheet reduction starting in 2027. Deputy Governor Shinichi Uchida made it clear that the bank will continue to raise rates in response to economic and inflation conditions and did not rule out the possibility of adjusting the pace of government bond purchases, sending a clear signal of policy normalization.

SpaceX is spending $60 billion to acquire AI programming firm Cursor, ramping up its push into the enterprise-level AI market. According to documents disclosed on Tuesday, the transaction will be settled entirely in stock, with Cursor’s parent company, Anysphere, receiving an equivalent value in SpaceX shares. This acquisition targets the field of autonomous programming agents and aims to help SpaceX accelerate its pursuit of major competitors in the AI sector following its sensational IPO.

Qualcomm(QCOM) is in talks to acquire AI chip startup Tenstorrent, with an offer ranging from $8 billion to $10 billion. According to media reports, the price under discussion could reach as high as $10 billion, but negotiations are still ongoing, and the price remains subject to change; there is also a possibility the deal could fall through. If the deal closes at $10 billion, it would be one of the largest acquisitions in the global AI chip sector in the past three years.

Apple’s(AAPL) product roadmap has come to light: in 2027, the company will launch camera-equipped AirPods and a new generation of foldable iPhones. Also set to debut during the same period are several new products, including an anniversary edition iPhone. Among them, the new AirPods will be Apple’s first AI-centric wearable device, using a computer vision camera to provide Siri with real-world situational awareness. Additionally, Apple is developing several next-generation chips for future devices and plans to launch its first smart glasses as early as the end of next year.

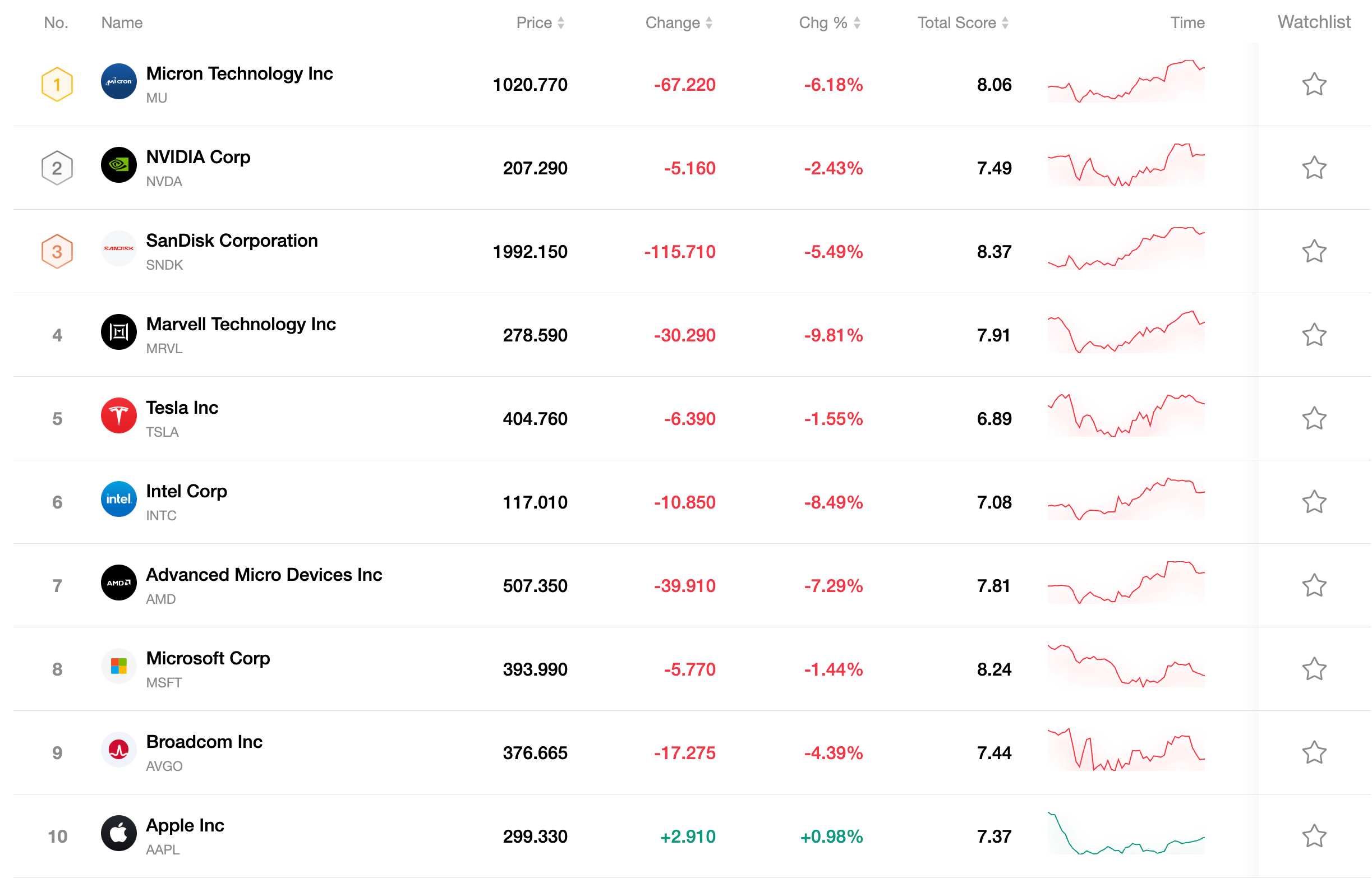

Top 10 Most Traded Stocks

The table below lists the ten most actively traded stocks on Tuesday. With their massive trading volumes and excellent liquidity, these assets have become key indicators for tracking global market trends.

Recommended Articles