Meet the Dividend King Stock That's Up 20% in 2026. Here's Why It Can Continue Outperforming the S&P 500 and Nasdaq-100 in the Second Half.

Key Points

Colgate-Palmolive doesn’t depend on the U.S. market to drive sales growth.

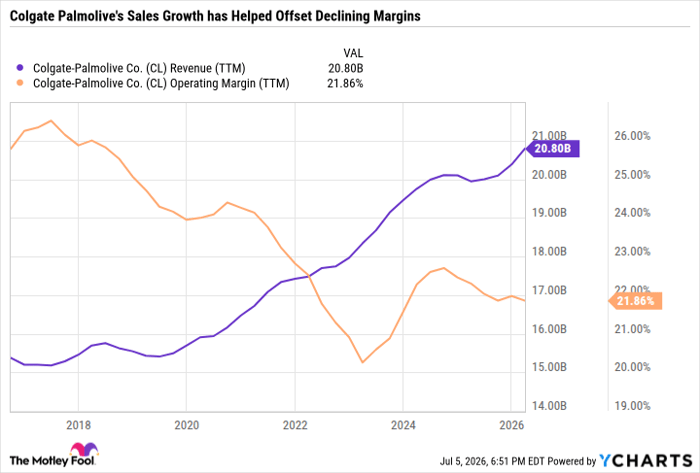

The company’s margins are strong, although they have ticked down in recent years.

Colgate-Palmolive is expensive for all the right reasons.

- 10 stocks we like better than Colgate-Palmolive ›

As of market close on July 3, the S&P 500 (SNPINDEX: ^GSPC) and the Nasdaq-100 are up 9.3% and 16.2%, respectively, year to date (YTD). This is well ahead of their historical average annual gains. The tech sector, especially semiconductor stocks, has been the driver of broader market returns. But that doesn't mean all value stocks are underperforming the major indexes.

Colgate-Palmolive (NYSE: CL) is up 20.4% YTD. And it's also an ultra-reliable dividend stock that has paid uninterrupted dividends since 1895 and has increased its payout for 63 consecutive years. That streak earns Colgate-Palmolive a spot on the list of Dividend Kings, which are companies that have paid and increased their dividends for at least 50 consecutive years.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Here's why Colgate-Palmolive remains a top buy now even after its recent run-up.

Image source: Getty Images.

Colgate-Palmolive is at the top of its game

Colgate-Palmolive has been a standout in the household and personal products industry. The company is guiding for 2026 net sales growth of 2% to 6% and organic sales growth of 1% to 4% at a time when many of its peers are experiencing sales declines. And even with margins under pressure, Colgate-Palmolive remains one of the most profitable companies in its industry. By comparison, Unilever, Kenvue, Church & Dwight, Clorox, Kimberly-Clark, and Estee Lauder all have operating margins under 20%.

CL Revenue (TTM) data by YCharts

The industry has been dealing with inflationary pressures and consumer resistance to price increases. But Colgate-Palmolive has done a masterful job of navigating these challenges through its elite brand portfolio, highly efficient supply chain and operations, and geographic diversification.

In addition to its flagship Colgate and Palmolive brands, the company owns Softsoap, Irish Spring, Tom's of Maine, and Speed Stick, among others. One of Colgate-Palmolive's top brands, Hill's Pet Nutrition, made up 23% of total 2025 sales.

Without factoring in Hill's, Europe, Middle East, and Africa (EMEA), Latin America, and Asia Pacific sales are more than triple those of North America, which has helped make Colgate-Palmolive resistant to U.S.-specific inflationary pressures. In the first quarter of 2026, North America was the only region that reported declining net and organic sales, while Latin America and EMEA posted double-digit growth and total company net sales rose 8.4% year over year.

A dividend you can count on

Colgate-Palmolive is far from cheap -- trading at 25 times forward earnings -- because the stock price has been rising faster than the company's earnings growth. But Colgate-Palmolive deserves its premium valuation because its results are solid despite a difficult operating environment. This resilience is particularly appealing to risk-averse folks seeking a stable passive income stream to help supplement retirement income. If inflationary pressures ease and consumer spending improves, a rising tide will lift the broader household and personal products industry. But Colgate-Palmolive isn't dependent on those factors to drive sales growth.

Colgate-Palmolive yields 2.2%, which is good but not quite high-yield territory. Many of its peers offer higher yields because they distribute the vast majority of their cash flow to shareholders through dividends, whereas Colgate-Palmolive's dividend is highly affordable. Its trailing-12-month free cash flow per share is at an all-time high of $4.66, well over double its $2.06 per-share annualized dividend.

So while Colgate-Palmolive could easily afford to pay a higher dividend, the company prefers a balanced approach of using cash to reinvest in the business, paying a steadily growing (and manageable) dividend, and buying back stock. Colgate-Palmolive has reduced its share count by 10% over the last decade, which has helped make the stock a better value.

Investing in a market leader

Colgate-Palmolive's geographic diversification and portfolio of leading brands across pet nutrition and oral, personal, and home care make it highly recession resistant. The company continues to deliver solid growth through volume and price increases, while many of its peers face a difficult trade-off: either cutting prices to drive volume or keeping prices high at the expense of lower sales volumes.

All told, Colgate-Palmolive stands out as one of the most reliable dividend-paying stocks on the market. It's a top buy for the second half of the year for investors who don't mind paying a premium price for a quality company.

Should you buy stock in Colgate-Palmolive right now?

Before you buy stock in Colgate-Palmolive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Colgate-Palmolive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $418,761!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,195,804!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 7, 2026.

Daniel Foelber has positions in Estée Lauder Companies, Kenvue, and Kimberly Clark. The Motley Fool has positions in and recommends Colgate-Palmolive. The Motley Fool recommends Kenvue and Unilever. The Motley Fool has a disclosure policy.

Recommended Articles