Here's What a $25,000 Investment in Nvidia Could Be Worth if History Repeats Itself

Key Points

Nvidia now trades at a much lower earnings multiple than it has in recent years.

Investors are skeptical of the stock's future returns, which already trades at a market cap of roughly $4.7 trillion.

Nvidia's fundamentals this year have never looked better.

- 10 stocks we like better than Nvidia ›

The artificial intelligence chip giant Nvidia (NASDAQ: NVDA) has struggled recently and is now down nearly 13% over the past month (as of July 1). After years of an incredible AI rally, doubts are now creeping into investors' minds.

There are questions about whether the large tech companies can continue to invest hundreds of billions annually in AI infrastructure, which is driving much of the cycle, and whether constraints such as energy and power will eventually have a real impact. For Nvidia specifically, competition in the chip space seems to be intensifying.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

That said, Nvidia hasn't done anything to suggest its business is at risk of slowing, so if the concerns don't materialize, the stock could have upside. Here's what a $25,000 investment in Nvidia could be worth if history repeats itself.

Image source: Nvidia.

Nvidia's valuation looks compelling

While many high-flying AI companies trade at monster valuations, that's not really something you can say about Nvidia.

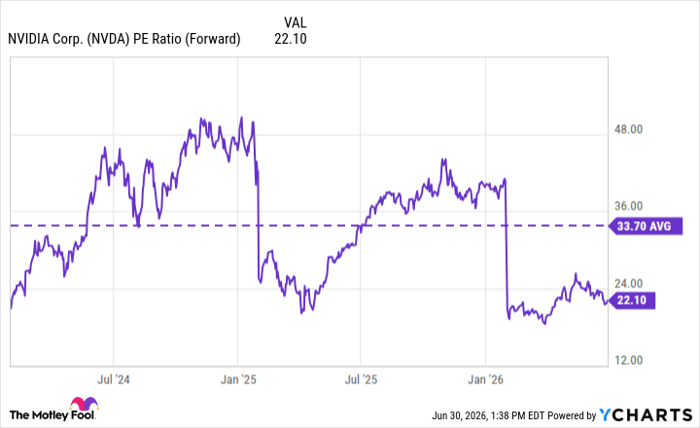

NVDA PE Ratio (Forward) data by YCharts

On the surface, Nvidia trading at roughly 22 times forward earnings looks quite reasonable. In the first quarter of Nvidia's fiscal year 2027, ending April 26, the company grew revenue 85% year over year, while diluted earnings per share soared by 140%.

In March, CEO Jensen Huang said he expects the company's Blackwell and Vera Rubin chips to generate $1 trillion in sales between that time and the end of 2027.

Furthermore, in its first fiscal quarter of 2027, Nvidia announced plans to become much more involved in the central processing unit (CPU) space, which has been in high demand due to the rise of agentic AI. Management said they think they can generate nearly $20 billion of CPU sales, making it an instant industry leader.

Threats to the thesis

Obviously, there are real concerns about Nvidia from an industry perspective and a company-specific perspective.

From an industry perspective, if AI experiences a significant pullback or turns out not to be as consequential as promised, that would significantly impact Nvidia, which is at the center of the AI trade. A pullback could occur if hyperscalers slow capital expenditures or if there are constraints in the AI supply chain, whether in memory, power, or even freshwater.

Now, those could also be temporary, so if one or more of these concerns come to fruition, that doesn't mean it's a complete deal-breaker, particularly for long-term investors.

It's also possible that AI is not capable of doing some of the things it's promised, which could, in fact, be a thesis-breaker. It's hard to know the likelihood of this event and even more difficult to time it, if you do think this is a real threat.

For Nvidia specifically, the challenge to its model could come from a few different areas.

There are competitors like Cerebras and Space Exploration Technologies Corp, which have promised to make more powerful GPUs than Nvidia, and Cerebras already has chips it claims are 15 times faster than some of Nvidia's models.

An even bigger threat would be if a competitor could challenge the operating system Nvidia has built for developers using its graphics processing units (GPUs) to train AI models, called Compute Unified Device Architecture (CUDA).

Nvidia launched CUDA in 2006 and has built a whole ecosystem around it, so this is easier said than done, but it nonetheless represents a substantial part of Nvidia's moat and therefore would be devastating to the company if CUDA loses its grip on the market.

If history repeats itself

As you can see in the chart above, Nvidia has had an average forward price-to-earnings ratio of nearly 34 for the past two years. Wall Street consensus estimates suggest the company will earn adjusted earnings per share of $8.97 in its current fiscal year.

Applying a 34 forward P/E, the stock would be worth roughly $305 per share, implying about 54% upside from current levels. This means a $25,000 investment in Nvidia would be worth over $38,400 if history repeats itself.

Now, investors should understand that there's no guarantee this plays out. Nvidia, at its current market cap, is up against the law of large numbers. As companies get more mature, they typically face lower multiples. Competition could also be a real concern.

However, Nvidia has traded at a 34 forward P/E before, so it could do so again should the company prove investors wrong about their concerns.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $418,761!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,195,804!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 3, 2026.

Bram Berkowitz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles