US Pre-Market: Meta’s Entry Into Cloud Computing Triggers Continued Chip Stock Decline, Micron Drops Over 2%, Key Non-Farm Payrolls Loom

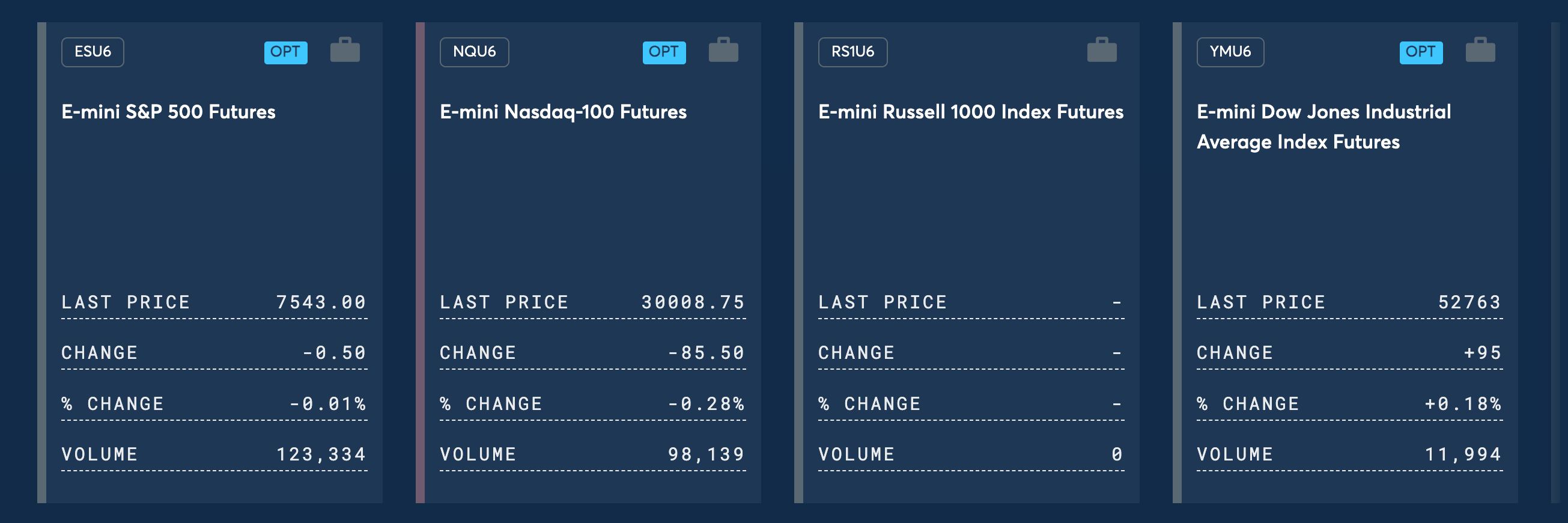

TradingKey - On July 2, Eastern Time, in pre-market trading, the three major U.S. stock index futures showed mixed performance. As of press time, Dow Jones Industrial Average futures rose 0.18%, S&P 500 Index futures fell 0.01%, and Nasdaq 100 Index futures dropped 0.28%.

[Source: CME Group]

In commodities, gold and silver prices rose. As of press time, spot gold ( XAUUSD) was trading at $4,068/oz, up 0.92%; spot silver ( XAGUSD) was trading at $59.83/oz, up 1.21%.

International oil prices continued to trend lower. As of press time, WTI crude oil futures were trading at $67.45/barrel, down 1.66%; Brent crude oil futures were trading at $70.53/barrel, down 1.45%.

In the crypto market, as of press time, Bitcoin (BTC) was trading around $61,240, and Ethereum (ETH) was trading around $1,645. The US Dollar Index was at 101.40.

Unusual Market Movements

The memory chip sector extended its decline premarket. As of press time, SanDisk ( SNDK) fell over 3%, Western Digital ( WDC ), Micron Technology ( MU ), Seagate Technology ( STX) fell over 2%.

The optical communications sector fell collectively premarket. Corning ( GLW ), Coherent ( COHR ), Lumentum ( LITE) fell nearly 2%.

The semiconductor sector was under pressure overall. Marvell Technology ( MRVL) fell about 2.2%, Advanced Micro Devices ( AMD ), Intel ( INTC) fell over 1.5%.

Mega-cap tech stocks diverged premarket. Apple ( AAPL) rose 0.33%, Amazon ( AMZN) rose 0.22%, Microsoft ( MSFT) rose 0.71%, Tesla ( TSLA) rose 0.54%, SpaceX ( SPCX) rose 0.41%, Meta ( META) rose 0.23%, Nvidia ( NVDA) fell 0.74%, Alphabet Class A ( GOOGL) fell 0.79%.

Market Headlines

Meta enters computing power market, sparking a rout in chip stocks. Meta is planning to launch a cloud computing business, with plans to lease or sell its surplus AI computing power. Following the news, Meta shares surged over 8%. However, market concerns that Meta might reduce its future procurement of external computing power triggered a 6.27% plunge in the Philadelphia Semiconductor Index. Micron Technology fell 10.57%, SanDisk dropped over 10%, and Intel slid more than 9%. The panic spread to the Asia-Pacific region, where South Korea's KOSPI index plummeted on Thursday, triggering a circuit breaker, with Samsung Electronics and SK Hynix both suffering heavy losses.

Nvidia launches revenue-sharing model for AI factories. Nvidia announced that it will partner with AI cloud service providers to build large-scale, multi-tenant AI factories through revenue-sharing and credit-support mechanisms. This model aims to lower the financing barriers for AI cloud providers building data centers, while generating recurring revenue for Nvidia tied to computing power usage.

SoftBank establishes SB Neo to enter US AI cloud market. SoftBank Group and SoftBank Corp. announced the creation of a joint venture, SB Neo Inc., with SoftBank Corp. holding a 51% stake and its parent company, SoftBank Group, holding 49%. Leveraging SoftBank Group’s 10-gigawatt-class energy and AI infrastructure, the company plans to officially launch new cloud services in fiscal year 2027. If the expansion goes smoothly, the annual operating profit of SoftBank's telecom unit could rise to between 3 trillion and 4 trillion yen.

OpenAI proposes transferring 5% stake to US government. According to the Financial Times, OpenAI is in discussions to transfer an approximate 5% stake to the U.S. government, which would be valued at around $42.6 billion based on an $852 billion valuation. The proposal aims to ease regulatory pressure and remains in the early stages of discussion.

U.S. June nonfarm payrolls report to be released early tonight. Due to the Independence Day holiday, the U.S. Bureau of Labor Statistics will release the June nonfarm payrolls report tonight at 8:30 PM Eastern Time. The consensus estimate is for payrolls to increase by 113,000, with the unemployment rate at 4.3%. Goldman Sachs projects a gain of 140,000, noting that the World Cup could contribute an additional 40,000 jobs.

Fed Chairman Warsh: Inflation 'still too high'. Speaking at the ECB Forum in Portugal, Warsh stated that current U.S. inflation remains too high, while announcing that the central bank would abandon forward guidance on interest rates in favor of data-dependent decision-making. Warsh did not offer any signals regarding the July policy meeting.

Key Events Calendar

Eastern Time | Event |

July 2, 8:30 AM | U.S. June Nonfarm Payrolls Report (Market expectation: +113,000, unemployment rate: 4.3%) |

July 3 | U.S. Independence Day holiday, U.S. stock markets closed |

July 7 | SpaceX officially added to the Nasdaq 100 Index |

The sector rotation triggered by Meta's cloud business continues to unfold. Chip stocks remain under pressure as capital migrates from AI hardware to the software and internet sectors. Tonight's nonfarm payrolls data is the real focus; if employment beats expectations, Fed rate-hike expectations will heat up, and interest-rate-sensitive tech growth stocks may face another sell-off. If the data is weak, it is expected to provide a breather for the chip sector. Prior to the data release, the market is highly likely to remain range-bound.

Recommended Articles