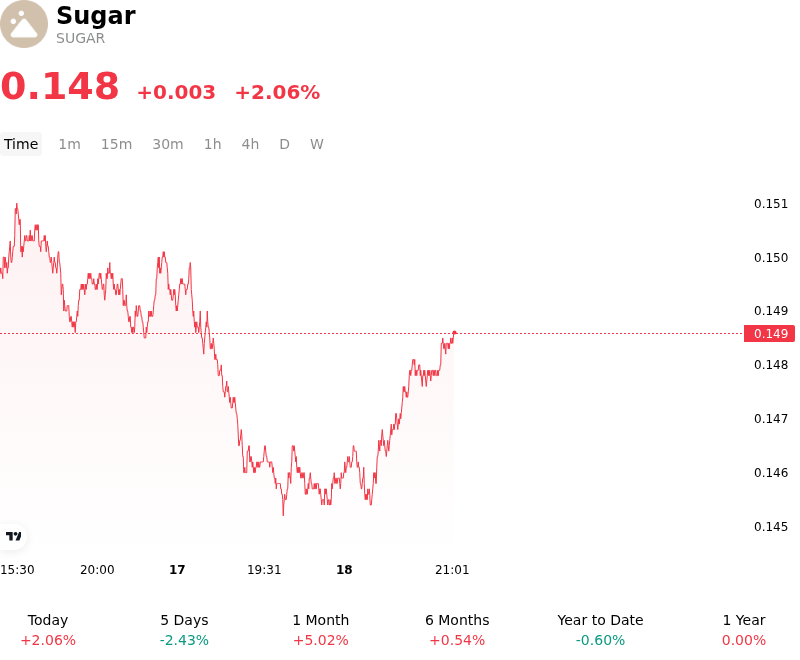

Sugar (SUGAR) Is up 2.06% on Jul 17: Here Is Why

Sugar (SUGAR) is up 2.06% at Jul 17 09:10(ET), now at $0.1485, with a 7-day down of 0.67%.

What is driving Sugar (SUGAR)’s stock price up today?

The upward pressure on sugar prices is primarily driven by immediate supply-side constraints originating from Brazil's Center-South region, the world’s most influential production hub. Unseasonably heavy rainfall across the primary sugar-producing belt has interrupted harvesting and crushing operations, leading to concerns over a temporary tightening of physical supplies. While the overall crop size for the season remains substantial, these logistical delays at the peak of the harvest cycle are forcing a repricing of near-term delivery obligations as mills struggle to maintain the expected pace of production.

Adding to the bullish sentiment is the recent appreciation of the Brazilian Real against the U.S. Dollar. A stronger Real discourages Brazilian producers from selling sugar denominated in dollars, as it reduces their local currency returns. This currency dynamic typically restricts the flow of exports into the global market, providing a firm floor for international prices. Institutional capital flows have responded to this shift, with managed money increasing long exposure as the risk-reward profile favors the upside amid a tightening spot market.

Global inventory outlooks are also being influenced by persistent export restrictions from India. Despite improved monsoon performance, the Indian government’s commitment to its domestic ethanol blending program continues to limit the volume of sugar available for the international market. This policy environment, combined with signs of recovering demand in the Asian refining sector, suggests that the global sugar balance remains more fragile than previously anticipated. Furthermore, aging logistics infrastructure and port congestion in South America are exacerbating the difficulty of moving existing stocks, leading to a build-up of the risk premium in front-month contracts.

Looking forward, investors remain focused on the parity between sugar and ethanol production in Brazil. With global energy prices showing resilience, the incentive for mills to divert more cane to ethanol production remains a structural risk to the global sugar supply. Market participants are closely monitoring upcoming industry reports for confirmation of the extent of recent weather-related disruptions. Any sustained shortfall in the cumulative crush volume could lead to a broader reassessment of the global deficit forecast for the remainder of the marketing year.

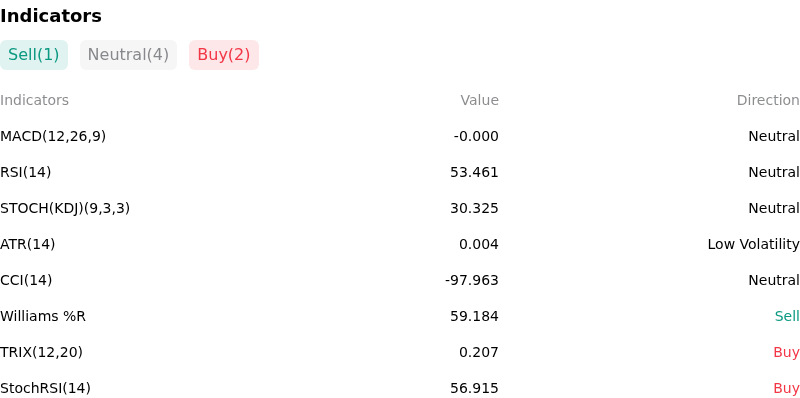

Technical Analysis of Sugar (SUGAR)

Technically, Sugar (SUGAR) shows a MACD (12,26,9) value of -0.000, indicating a neutral signal. The RSI at 53.275 suggests neutral condition and the Williams %R at 60.204 suggests sell condition. Please monitor closely.

More details about Sugar (SUGAR)

Recent Events and Risks:

- Indian Export Policy Speculation: Improved monsoon rainfall across key producing states like Maharashtra and Karnataka has sparked market concerns that the Indian government may reconsider its current sugar export ban for the 2024/25 season, which would introduce a significant volume of supply to the global market and dismantle the prevailing deficit narrative.

- Currency-Driven Selling Pressure: Ongoing volatility and weakness in the Brazilian Real against the U.S. Dollar have incentivized Brazilian mills to increase their hedging and spot sales to capture higher local currency returns, exerting immediate downward pressure on New York raw sugar futures.

- Improving Soil Moisture in Brazil: Recent precipitation in Brazil’s Center-South growing regions, while potentially causing minor delays to the tail-end of the current harvest, is being viewed by analysts as a critical relief for the 2025/26 crop outlook, leading to the liquidation of long positions as drought-related risk premiums begin to erode.

- Production Mix Shift: Data indicating a sustained high "sugar mix" in Brazilian mills—where more cane is diverted to sugar production rather than ethanol due to better relative profitability—is resulting in higher-than-anticipated bi-weekly production figures that are currently testing key technical support levels.

Recommended Articles