Tech Giants' Financial Reports Fall Short: What's Next for the US Stock Market?

- US President Donald Trump says Iran talks to begin Monday after canceling attack

- Gold Price Forecast: Can Gold Still Rise Above $4,300 Ahead of July Non-Farm Payrolls?

- Gold rallies to two-week high as USD softens on Iran deal hopes, receding Fed hike bets

- Australian Dollar remains calm following Trade Balance data

- WTI holds firm near $77.50 as escalating Middle East tensions threaten oil supply routes

- WTI trades with positive bias below mid-$79.00s on Iran uncertainty, supply concerns

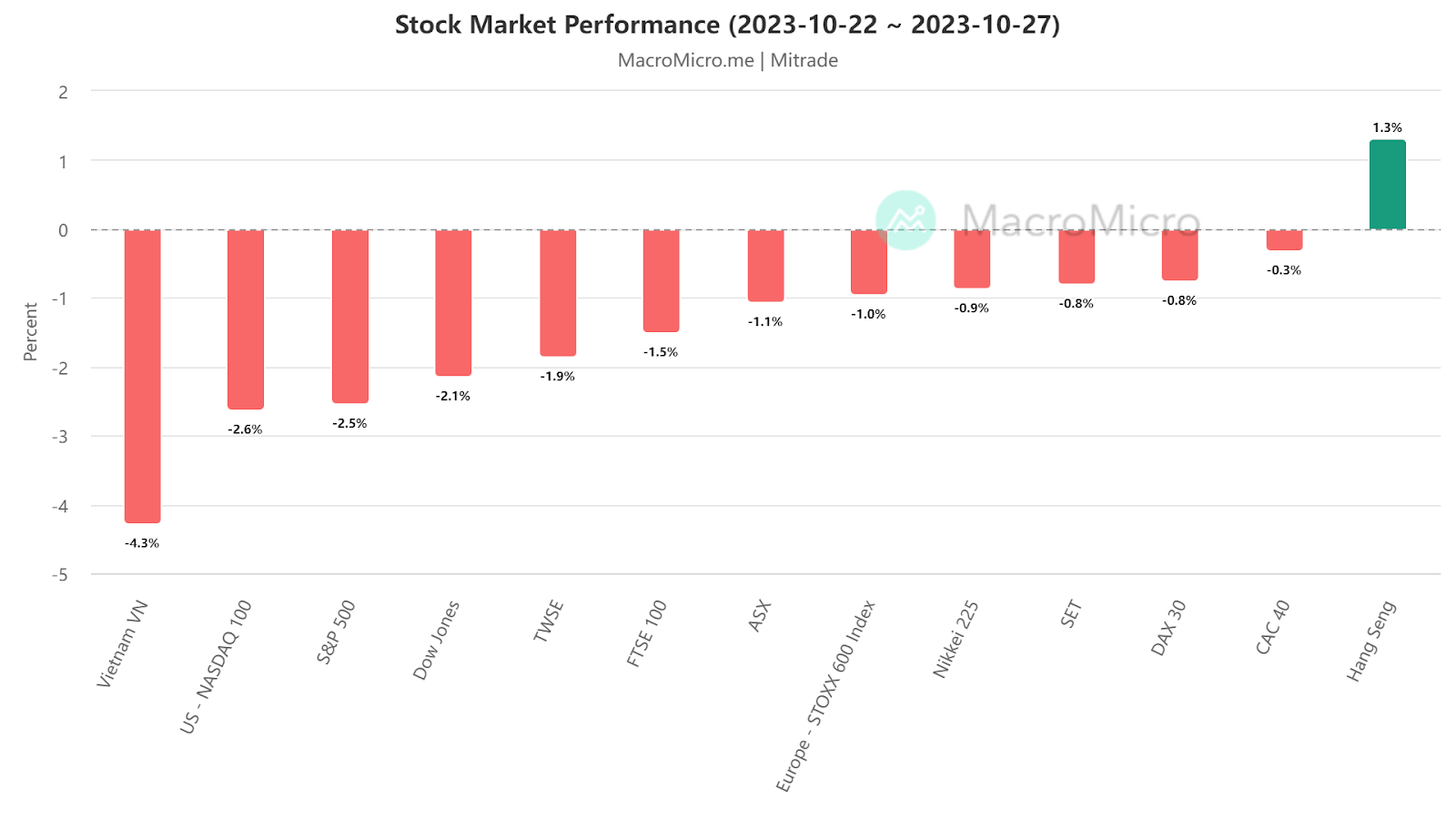

Market Review

Last week (10/23-10/27), most global markets experienced declines. In the US, the S&P 500 index dropped by 2.53%, the Dow Jones Industrial Average fell by 2.14%, and the Nasdaq 100 index declined by 2.61%. In Europe, the STOXX 600 index decreased by 0.96%. Among Asian stocks, the Hong Kong Hang Seng Index performed the best, rising by 1.33%.

【Source: MacroMicro;Date2023/10/23-2023/10/27】

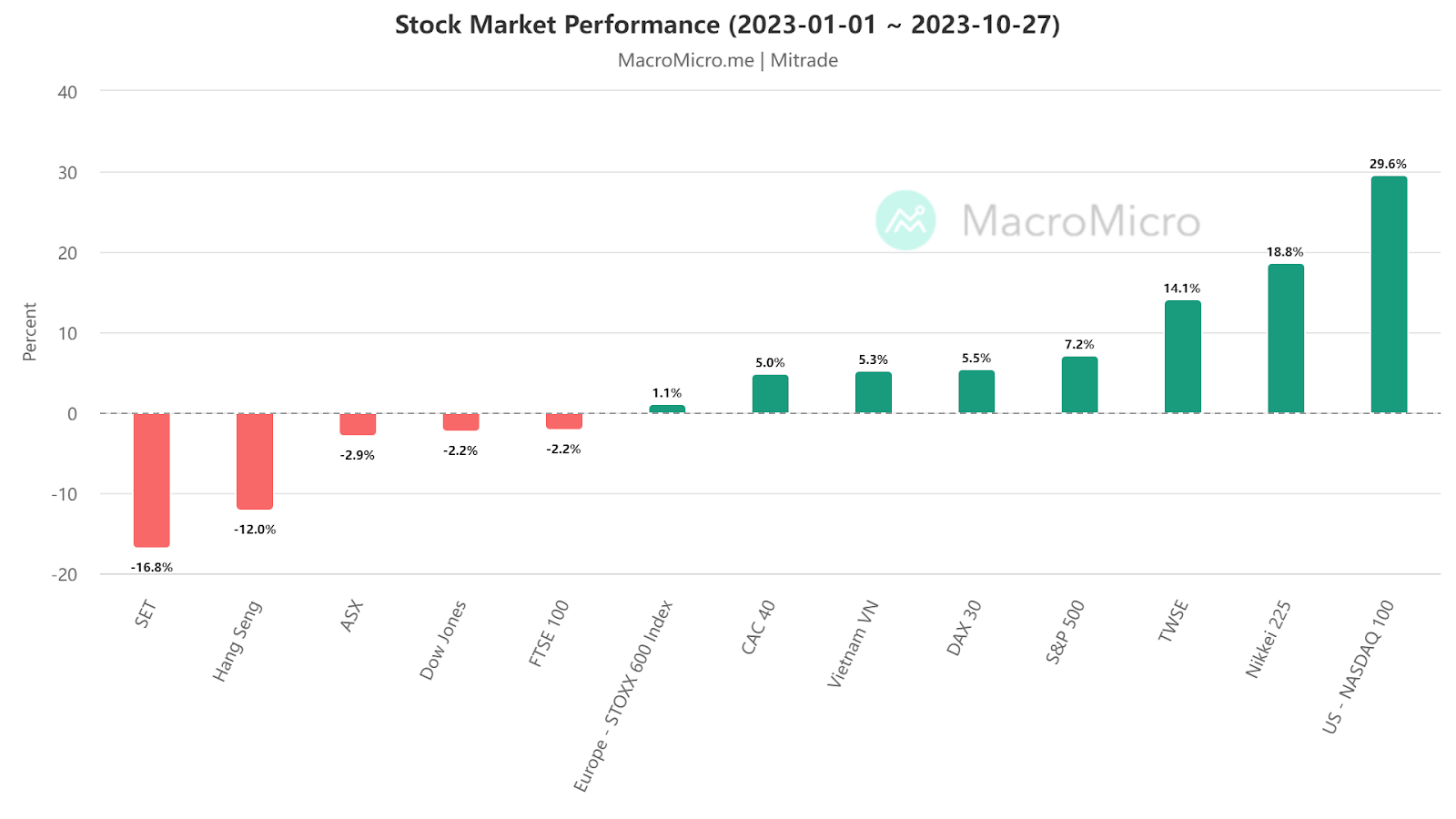

【Source: MacroMicro;Date2023/1/1-2023/10/27】

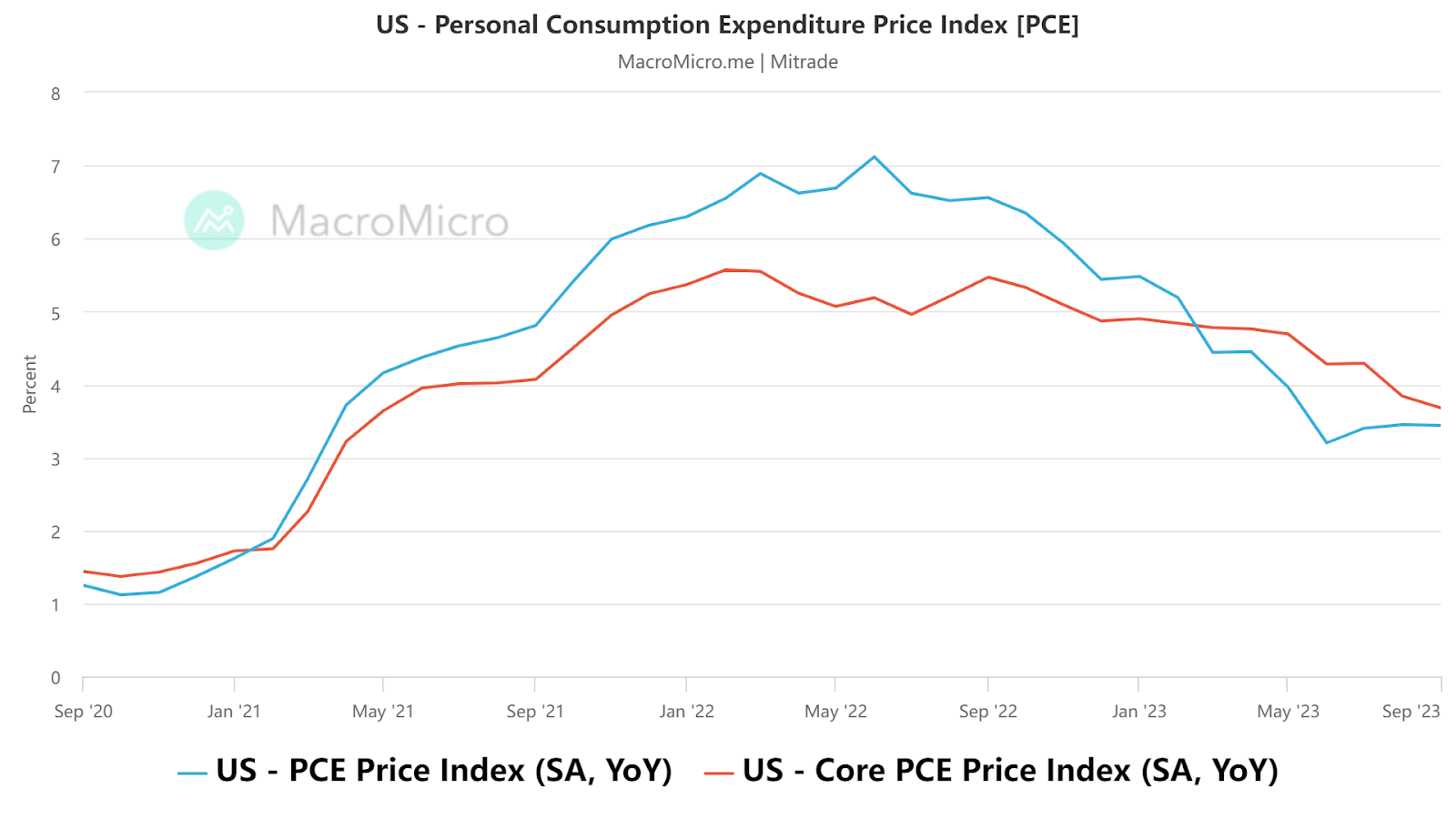

1.US September PCE Data Mixed, Minimal Shift in Probability of Interest Rate Hike

According to data on October 27th, the US September PCE price index increased by 3.4% year-on-year. The core PCE price index, excluding food and energy, decreased from 3.9% in August to 3.7% year-on-year, both in line with market expectations. However, the month-on-month growth of PCE in September was 0.4%, and the month-on-month growth of core PCE was 0.3%, slightly exceeding expectations.

【Source:MacroMicro】

In addition, personal income slowed down while spending accelerated. Personal income growth declined from 0.4% month-on-month in August to 0.3%, but personal consumption expenditure (PCE) increased by 0.7% month-on-month, significantly higher than the previous month's 0.4%. This led to a decrease in the personal savings rate, dropping from 4.0% to 3.4%, reaching a new low since December last year.

The economic forecast released by the Federal Reserve in September indicated that the year-end core PCE is expected to reach 3.7%, which has already met the target, further supporting the notion of ending rate hikes. However, the rebound in consumer spending may imply a back-and-forth pattern of inflation, and institutional analysis suggests that the possibility of a Fed rate hike has not been completely eliminated.

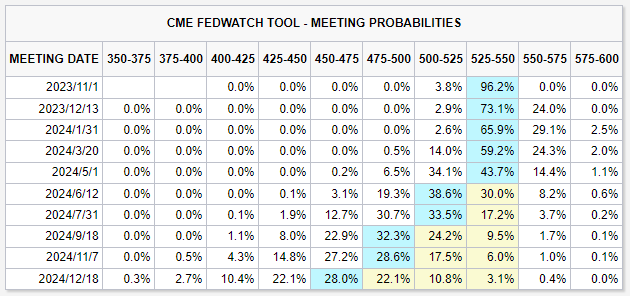

According to CME data, the market's expectation for a rate hike by the Federal Reserve in December is currently at 24%, with little change compared to last week.

【Source:CME】

Mitrade Analyst:

The impact of inflation data on interest rate hikes will be diminishing unless there is a significant surprise. Currently, the Federal Reserve's actions to raise interest rates are constrained by the Treasury Department as it would exacerbate US fiscal pressures. In the future, we should not solely rely on economic fundamentals to assess the Fed's actions but also pay more attention to external market conditions.

Investors should keep an eye on Chairman Powell's remarks during this week's Federal Reserve policy meeting, as they could have an impact on the market.

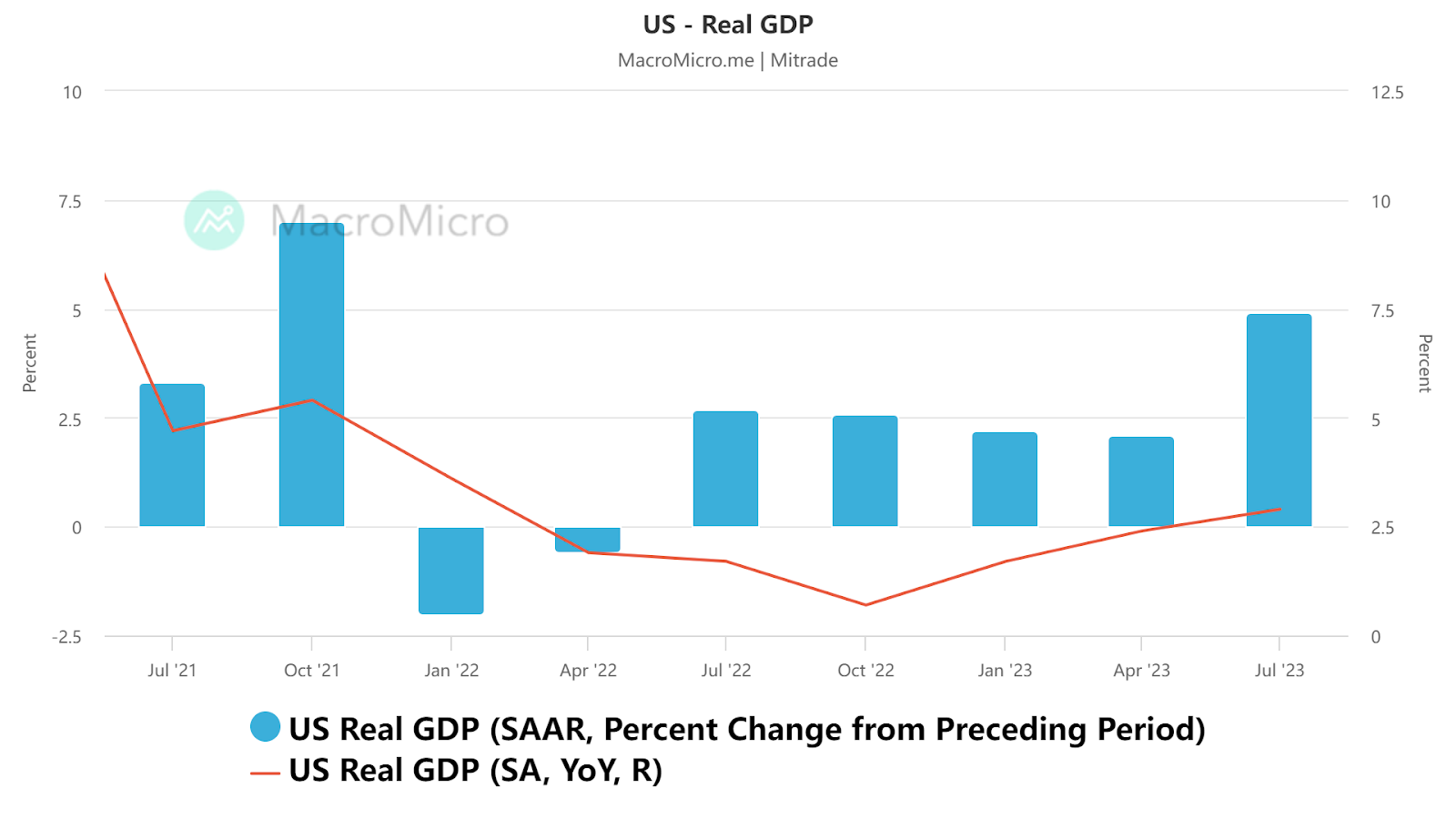

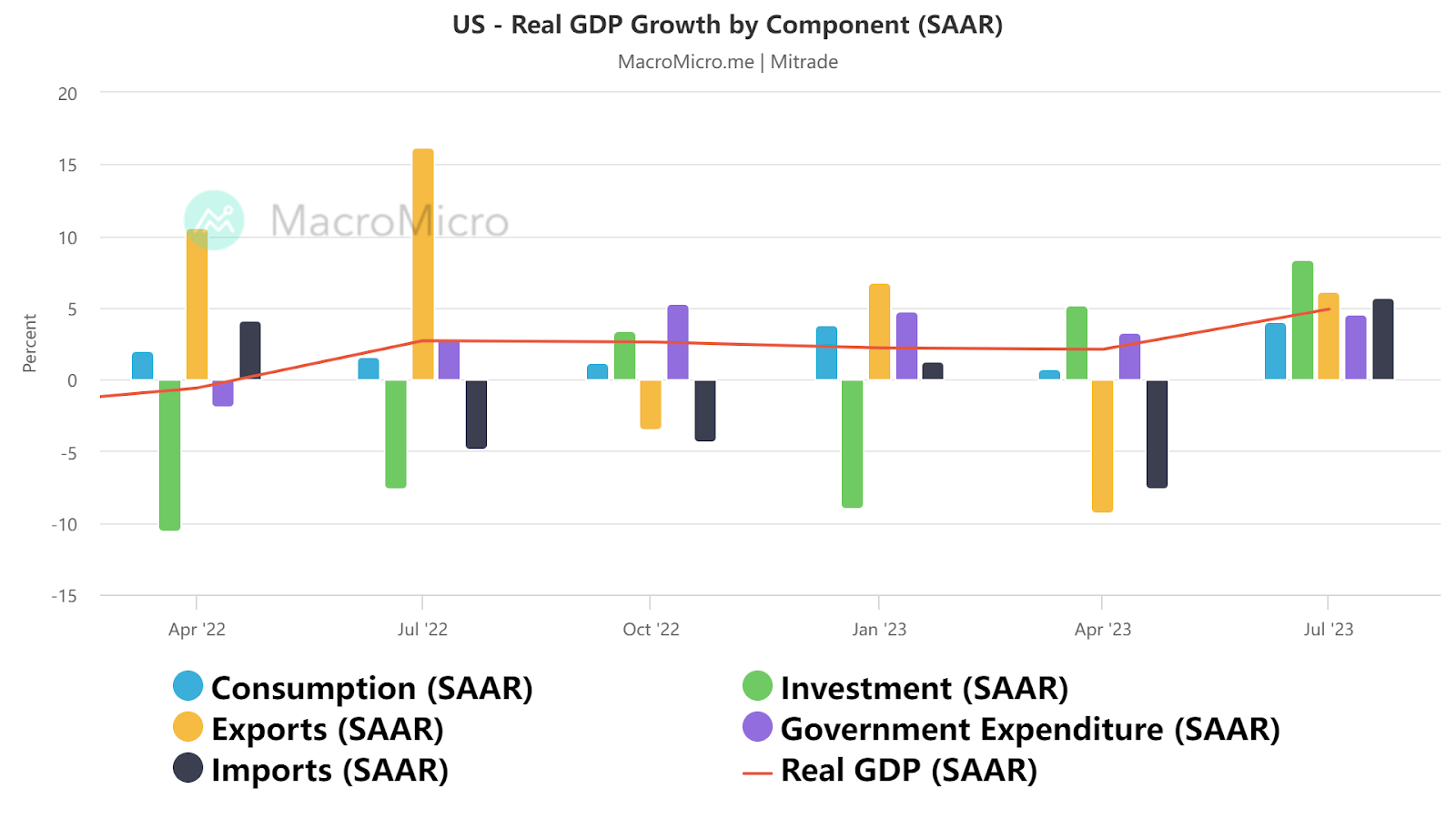

2. US GDP Beats Expectations in the Third Quarter, Is Recession Off the Table?

Data released on October 26th shows that the US real GDP for the third quarter grew at an annualized rate of 4.9%, surpassing market expectations of 4.7%.

【Source:MacroMicro】

Breaking down the data, consumer spending, which holds the largest share, surged by 4%, significantly higher than the previous quarter's 0.8% growth. Investment also saw a substantial increase of 8.4%, surpassing the previous quarter's 5.2%. Government spending made a significant contribution to GDP, rising by 4.6% in the third quarter.

Based on the detailed data, the robust growth in US GDP during the third quarter was primarily driven by strong durable goods consumption, a rebound in residential investment, and substantial military expenditure.

【Source:MacroMicro】

Many economists have doubts about the sustainability of growth in the fourth quarter and anticipate a slowdown in economic expansion in the last few months of the year due to constraints on borrowing costs impacting the purchase of big-ticket items and the phasing out of federal student loan relief. Standard & Poor's Global Ratings preliminarily forecasts that economic growth in the fourth quarter could drop to 1.7%.

Mitrade Analyst:

Behind the stronger-than-expected GDP growth in the United States lies a significant amount of fiscal stimulus and deficits, with the US budget deficit surging by 20% in the 2023 fiscal year. In terms of durable goods data, consumer optimism towards the economy is evident, with a decrease in recession expectations.

The robust state of the US economic growth implies that the Federal Reserve may keep interest rates at elevated levels for a longer period, which could unfavorably impact the stock market.

3. US Stocks Hit by Financial Report Week

Last week, tech giants Microsoft, Google, Meta, and Amazon released their latest financial reports. Following the announcements, Microsoft and Amazon saw minor increases, while Google and Meta experienced significant declines, with Google falling more than 9%, dragging down the Nasdaq index.

【Source:TradingView;Stock Price Trends of Tech Giants Last Week】

This year, as the AI frenzy spreads, the Big Seven of technology (Apple, Microsoft, Google, Amazon, NVIDIA, Tesla, and Meta) have become the main players in the US stock market. However, the continuously rising interest rates are dampening investor optimism, with the Nasdaq 100 index falling nearly 10% since August.

Morgan Stanley has cautioned that profit forecasts for the fourth quarter of this year and 2024 in the US stock market remain too high, which will reduce the likelihood of a year-end rebound.

Mitrade Analyst:

The reasons behind the pullback of tech giants are twofold. On one hand, investors had overly high expectations for financial performance, and on the other hand, rising interest rates have put pressure on valuations. As valuations gradually normalize, market sentiment is expected to improve. We maintain our view that stock indices will rebound by the end of the year.

This week, Apple will release its financial report. If it exceeds expectations, it will boost market sentiment; however, if it falls short, there is an increased possibility of further adjustment in the stock indices.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.