PDD’s Next Growth Engine: Trading Profit for Ecosystem, Technology for Efficiency

TradingKey - Pinduoduo (PDD) Q1 2025 results don’t look good. The stock fell for several days after earnings, with market sentiment taking a visible hit.

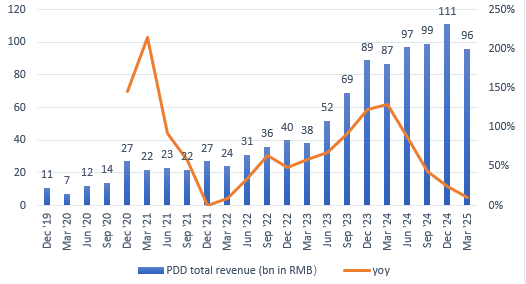

Revenue came in at RMB 95.7 billion, up 10% year-over-year, but still missed expectations by nearly RMB 6 billion. More importantly, this marks the third quarter in a row that PDD has failed to meet revenue estimates—a concerning trend.

Source: PDD earnings

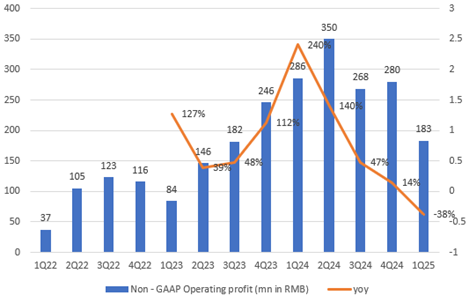

But the real pressure came from the profit side. Operating income dropped 38% year-over-year to RMB 18.3 billion, falling short of forecasts by a wide margin (over RMB 9 billion).

Source: PDD earnings

This isn’t just a one-off miss, either. It’s the second straight quarter where fundamentals are showing clear signs of weakening. Add in the new U.S. tariff headwinds hitting Temu earlier this year, and you can see why investors are starting to question how sustainable PDD’s international strategy really is.

Revenue Under Pressure, But GMV Growth Stays Strong

While the top and bottom lines disappointed, platform activity remained solid. Based on estimates from industry analysts, PDD’s Q1 gross merchandise volume (GMV) reached around RMB 1.07 trillion—up about 16% year-on-year. That’s no small feat, especially in a China e-commerce market that’s gradually maturing and seeing slower traffic growth across the board.

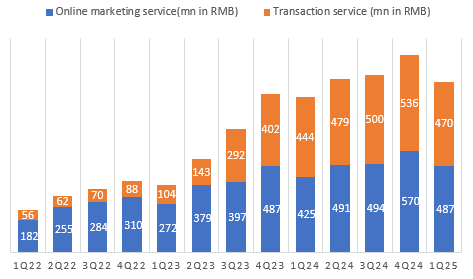

However, with the company stepping up subsidies and profit-sharing with merchants, its commission-based income didn’t rise in line with GMV. Transaction service revenue this quarter came in at RMB 47 billion, with a year-on-year growth rate of just 5.8%. This became one of the key factors dragging down overall revenue performance.

Advertising revenue held up slightly better, growing 14.8% year-on-year this quarter—just above the market expectation of 13%. The platform’s subsidy strategy helped stabilize traffic and merchant engagement to some extent, which in turn supported ad revenue growth. That said, ad monetization efficiency—the ratio of ad revenue to GMV or traffic—showed a clear declining trend. While subsidies played a role in maintaining user traffic and market share, they also put pressure on monetization efficiency from the advertising side.

Source: PDD earnings

Moreover,PDD’s overseas business Temu faced pressure from changes in tariff policy in early 2025, pushing the platform to pivot. It began accelerating its shift toward a semi-managed model while dialing back traffic support for its fully managed model.

In the fully managed approach, Temu books revenue as the difference between sale price and product cost, since it handles upfront logistics and fulfillment. The semi-managed model, by contrast, records only commission income. This accounting shift could lead to a sharp decline in reported revenue

PDD’s Marketing Bill Grows While Payoff Remains Unclear

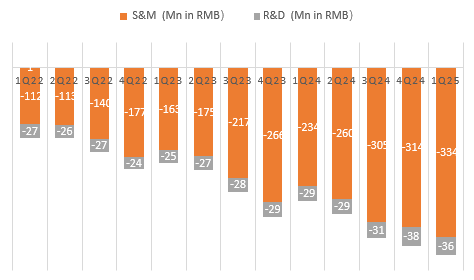

Marketing spend this quarter hit RMB 33.4 billion — up nearly RMB 10 billion from the same period last year, a 43% jump. It even came in higher than Q4, when the company was in the middle of its Double 11 peak season.

Source: PDD earnings

Given that overseas business took a hit this quarter due to tariff issues, Temu’s marketing budget was expected to shrink noticeably. So the fact that total marketing spend still soared suggests that the company has shifted its focus back to its domestic flagship platform.

What really drove the spike was the so-called “subsidy upgrade” at the user level. While JD and Alibaba have been making full use of government-backed incentives, Pinduoduo seems to be throwing in both the national subsidies and its own money — offering real, out-of-pocket discounts to users.

Revenue grew by 10%, while marketing spend jumped 43%. But the subsidies didn’t seem to deliver meaningful growth.

Pinduoduo primarily targets price-sensitive consumers, especially those in lower-tier cities. But many consumer goods eligible for government subsidies tend to flow toward premium e-commerce platforms like Taobao, Tmall, or JD.com. That’s because Pinduoduo's core product categories and user base make it much harder for its merchants to push into higher-end branding. The platform is just fundamentally better suited for affordable, budget-friendly products outside the scope of national subsidies.

So there are 2 reasons why the heavy subsidies might not have translated into stronger growth. One possibility: the incentive just wasn’t strong enough to attract new users, especially when brands on Tmall and JD were also cutting prices and leveraging subsidies. Another key factor could be mounting pressure on household spending power and income expectations.

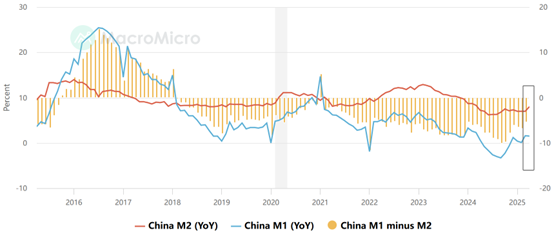

Liquidity data shows a clear trend: M2 — broad money supply — grew around 7–8% year-over-year, but M1 — which better reflects money actually in circulation — was up just 1.0–1.6%. The gap here signals that much of the "liquidity injection" is being saved, not spent. Chinese households are clearly leaning toward saving rather than consumption.

Source: MacroMicro

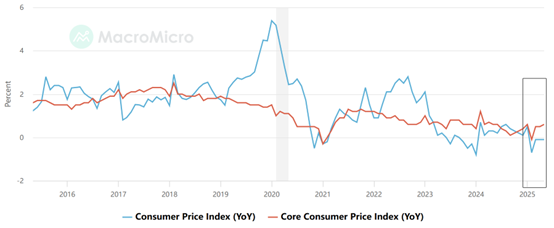

Meanwhile, China’s CPI has hovered around zero and even slipped into negative territory (–0.1%) in recent months, pointing to weak consumer demand. The core issue here is growing uncertainty and concern over future income. As a result, consumer spending power is falling faster than prices are declining — which limits how much impact Pinduoduo’s subsidies can actually have on driving revenue growth.

Source: MacroMicro

PDD Ramps Up AI with Clear Focus on Efficiency

PDD spent RMB 3.58 billion on R&D this quarter, up roughly 23% to 27% from a year earlier — beating market expectations of RMB 3.39 billion. Although the company didn’t specify how much of that investment went into AI, the clear improvement in product efficiency and platform-level performance suggests that AI has become a core focus of its development strategy.

PDD’s AI strategy is notably pragmatic. Instead of competing head-on with companies like Alibaba in building large general-purpose models, it targets high-impact, efficiency-driven applications that deliver measurable returns.

Among those, dynamic pricing has had particularly strong results. The system can now scan prices for 500 million products across the internet in under 30 seconds and adjust its subsidy strategies in real time. During the 2024 Double 11 shopping event, for example, 97% of flash sale prices on the platform were generated by AI.

In addition, AI is playing a key role in refining the platform’s recommendation system. By analyzing full user behavior chains — including when someone clicks, hesitates, and decides not to buy — the system can better predict real demand. As a result, average page views per user rose from 2.3 to 5.8, and time spent on the platform jumped 140% year-over-year.

These scenario-based applications help Pinduoduo boost both user conversion and merchant ROI. At the same time, they allow the company to significantly reduce marketing costs through more accurate targeting — such as offering personalized coupons and smarter subsidies — which in turn support growth in GMV and commission revenue.

PDD Bets on Ecosystem Over Earnings

With e-commerce penetration in China nearing saturation, platforms are shifting from growth-at-all-costs to operating around existing user bases. In this transition, ecosystem health has become a critical factor in sustaining merchant confidence and user engagement.

In Q1 2025, facing a challenging macro environment, Pinduoduo reaffirmed its commitment to “sharing profits to protect the ecosystem.” Co-CEO Zhao Jiazhen introduced a RMB 100 billion merchant support initiative, including commission reductions and subsidies, designed to help sellers weather the economic cycle. This echoes earlier signals from management as early as Q2 2024 — that the company is willing to invest real capital in exchange for long-term structural resilience.

This ecosystem-first thinking extends globally. Although tariff tensions in North America have eased for now, Temu is diversifying its market focus toward Europe, Japan, and South Korea, with moves to localize operations and shorten delivery times in those regions. While regulatory headwinds remain in the U.S., Chinese goods continue to hold an irreplaceable position in global trade, supporting a positive long-term outlook.

Temu also began transitioning to a semi-managed model last year. While this approach shifts more daily operations to merchants, it gives those with supply chain advantages a new way to compete — with better margins, prioritized traffic, and faster logistics infrastructure. In response to Amazon’s commission cuts and the rise of low-cost channels like Amazon Haul, Temu offers merchants a cost-effective “dual-use” model: reuse FBA inventory, fulfill orders locally, and reduce cross-border expenses.

Merchants are now choosing fulfillment models based on product traits — fully managed for standardized, low-ticket items seeking volume; semi-managed for high-value or non-standard SKUs looking to preserve margins and avoid price wars. If semi-management exceeds 50% penetration in the next 1–2 years (2025 target: 40%), it will mark a key inflection point in Temu’s shift from scale to sustainability.

For Pinduoduo, unlocking new growth comes down to differentiated supply. In an overcrowded marketplace where user attention is scarce, the core issue isn't having “too many products,” but a lack of offerings that meet real, personalized needs. Product differentiation depends on supply chain strength and a willingness to innovate — both costly and risky. By lowering the burden for sellers, Pinduoduo makes room for experimentation and encourages merchants to offer more customized, demand-aligned products.

PDD’s Valuation Still Leaves Room to Run

Pinduoduo's growth may be moderating, but its profitability remains a key strength. Net margin is over 25%, above Alibaba’s 10%–15% and JD’s 5%–10%. GMV rose around 16% in Q1, significantly outpacing the 5%–10% growth seen among other domestic platforms. As the company improves platform efficiency, expands into new categories, and further ramps up ad monetization, revenue elasticity in the medium term remains visible.

At less than 10 times earnings today — and just 8 times forward — the stock trades well below industry averages. Its current valuation ranks near the bottom 10% of its historical range, signaling clear undervaluation. Although Alibaba and JD also look inexpensive, Pinduoduo’s stronger earnings trajectory and lower multiple offer better value relative to peers.

Source: SeekingAlpha

Wall Street hasn’t exactly been subtle—most analysts have pinned their targets around $170–190. That’s like saying the stock, even at today’s price, still hasn’t caught up with the fundamentals they’re anchoring to.

Challenges Ahead: Heavy Spending, Strategy Shifts, and Policy Risks

Despite its strong domestic foundation, Pinduoduo is entering a more complex phase of development, marked by several emerging structural headwinds. These include a natural deceleration in growth as China’s e-commerce market matures—a pattern previously seen with both Alibaba and JD.com. Moreover, rising cost pressure from sustained subsidy-driven user acquisition is weighing on margins. And with returns on such aggressive spending still unclear, long-term efficiency and payback remain open questions.

Meanwhile, its overseas expansion via Temu remains in flux: the shift from a fully managed to a semi-managed model—still at an early stage—introduces elevated logistical and supply chain execution risks, while regulatory uncertainties, especially related to cross-border compliance, continue to amplify both financial and reputational exposure.

Compounding these issues are lingering concerns over platform integrity—particularly with respect to counterfeit prevention and quality assurance—which, if not addressed meaningfully, could erode user trust and drive away higher-quality merchants, thereby undermining the very ecosystem that supports its growth

Recommended Articles