Marvel: This Chipmaker Isn’t What It Seems

- Marvell's data center revenue surged 88% YoY in FY25, now representing 75% of total sales, up from 33%.

- Non-GAAP Q4 FY25 EPS grew 40% QoQ to $0.60, with gross margin stable at 60.1% despite volume growth.

- The company’s PEG ratio of 0.49 signals undervaluation relative to a sector average of 1.66, despite GAAP valuation concerns.

- Custom silicon for AWS, Meta, and Microsoft positions Marvell as a core AI infrastructure enabler with long design cycles.

Marvell's (MRVL) valuation now looks extended to conventional investors, with a 22.87x forward non-GAAP earnings multiple and 60.04x forward GAAP P/E. On the surface, this looks overdone, particularly with a D- grade for valuation and price-to-sales ratios over 135% above the industry average. Yet this surface-level snapshot obscures a profound, underlying corporate transformation. Marvell is no longer a cyclical, broad-based chip supplier. In the 18 months since then, it's repositioned as a bespoke silicon and speed-up infrastructure partner to the AI titans, the hyperscalers AWS, Microsoft, and Meta.

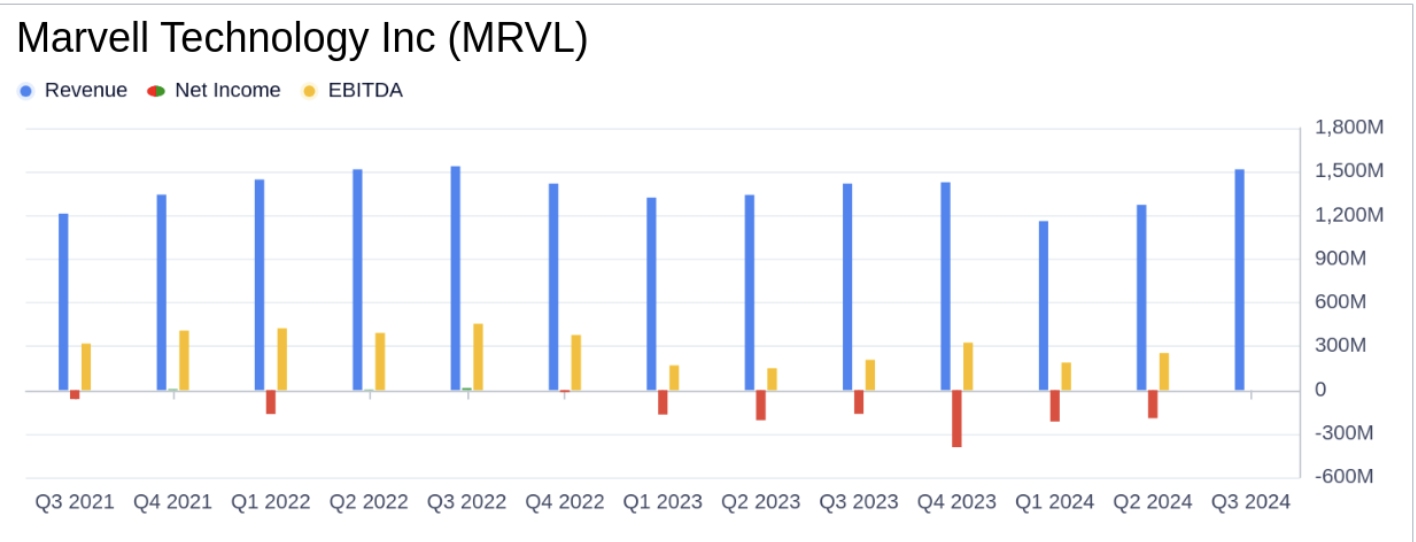

Revenue from the data center, which represented only 33% of overall sales in the early part of FY24, now accounts for a dominant 75% as of Q4 FY25. This is not a theoretical shift; it translates to the numbers: Q4 FY25 revenue rocketed 27% year-over-year and 20% quarter-over-quarter, led by 78% YoY growth in the data center. Headline valuation multiples look rich, however, because they do not factor in the stickier economics, longer design periods, and co-optimized AI silicon that now characterize Marvell's path.

Source: GuruFocus

Source: Marvell Technology, Inc.

In this context, apparent multiple expansion might be actual multiple compression against Marvell's reconfigured business mix. The firm is stealthily converting to a recurring AI infrastructure play with asymmetric leverage, but the market continues to treat it as a commodity semiconductor supplier. The resulting mispricing is an opportunity for long-term investors, particularly those who are willing to look through sector-average multiples and drill down into Marvell's changing margin structure, end-market transitions, and monetization quality.

The AI-Powered Core: From Mixed Market to Mission-Critical Silicon

It is not a marketing storyline, however, but rather a re-architecting of the entire business model. For FY25, Marvell had total revenue of $5.77 billion, up 5% YoY, which hides a breathtaking compositional change under the topline. Data center revenue rose 88% YoY to $4.16 billion, with legacy segments, carrier infrastructure, consumer, and enterprise networking falling 38% to 68%. The implication is striking: Marvell is now decisively a data center and AI company.

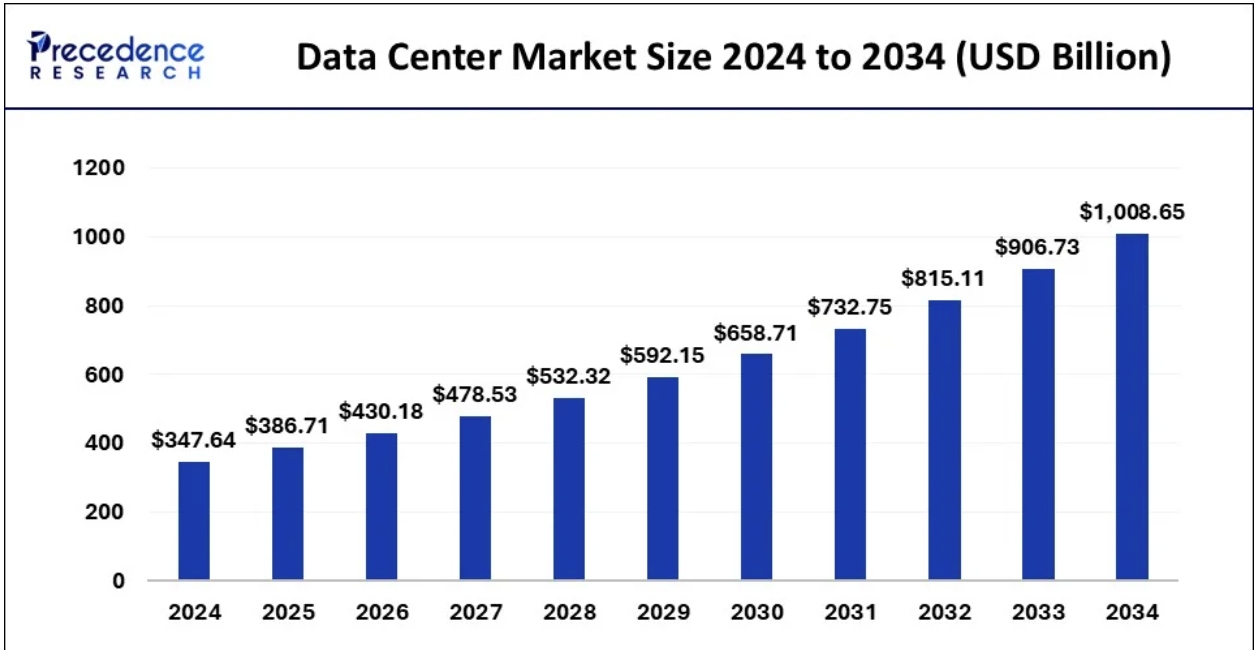

Source: Precedence Research

The underlying cause for this reacceleration is Marvell's increasing emphasis on custom silicon, such as its AI XPU and Arm-based CPU. In Q4 FY25, the company produced multiple hyperscaler-custom chips in volume. They are not off-the-shelf products; rather, they are cloud partners' co-designed chips, which are optimized for latency, power consumption, and bandwidth with the incorporation of HBM memory, PAM4 optical I/O, and coherent DSPs for native AI workloads. Such a level of integration contributes to longer design-in periods, increased gross margins, and deep switching expenses.

At the same time, Marvell's use of its 2nm silicon and co-packaged optics designs highlights its competitive moat in custom interconnects and custom compute. Those are not incremental steps, those are the basic building blocks for hyperscale AI infrastructure. Marvell's 800G PAM and 400ZR DCI product offerings, which are already in strong demand, further solidify Marvell in the high-growth spaces of network connectivity in AI datacenters.

At the consumer end, the weakness is structural. Marvell's consumer revenue declined 38% YoY and is now down to 5% of sales in Q4 FY25. Instead of fighting the decline, the management is tactically allowing the lower-margin verticals to contract and redeploying the R&D in AI. It is a conscious focus, not a failure.

Source: Marvell Technology, Inc.

Peers, Positioning, and the Unpriced Custom Edge

Marvell operates in a crowded semiconductor industry with leading positions by Nvidia (NVDA) in the domain of GPUs, AMD in x86+AI acceleration, and Broadcom (AVGO) in custom silicon. What differentiates Marvell is its focus on domain-specific architecture and interconnects, which are typically underappreciated by retail investors but are mission-critical to the hyperscalers.

In contrast with Broadcom, with its custom ASIC business servicing an equally large hyperscaler client base, Marvell trades at a discount with greater exposure to the data centre (75% of sales vs. ~50% for Broadcom).

Nvidia and AMD act further up the AI stack, but Marvell’s strength is in horizontal integration between switching, optical DSPs, and co-packaged optics. Marvell is infrastructural, supporting rather than substituting for the AI model providers. As Nvidia moves further into the network space with Spectrum-X, Marvell's existing customer base and in-production custom silicon provide a buffer against encroachment. Investor complacency about encroachment, however, particularly from the threat of Nvidia's vertical integration, is a long-term threat.

Profit Leverage, Quality of Monetization, and The Real Margin Story

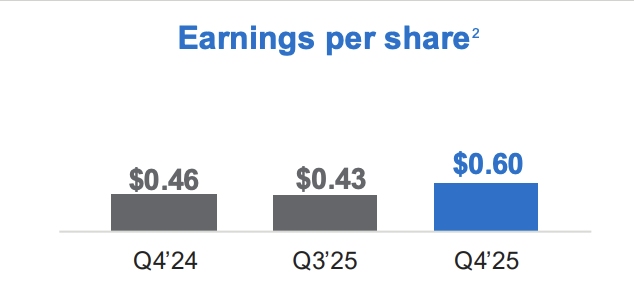

Despite noisy GAAP earnings from restructuring and amortization expenses, Marvell's non-GAAP figures paint a different picture: Non-GAAP Q4 FY25 EPS was $0.60, up 40% QoQ, and FY25 EPS $1.57. Non-GAAP gross margin was 60.1%, flat year-over-year despite a steep increase in volume and inventory movements. Operating margin also returned to 33.7% in Q4, an indication of leverage from the company's growing scale as well as product mix.

Source: Marvell, Financial and Business Results

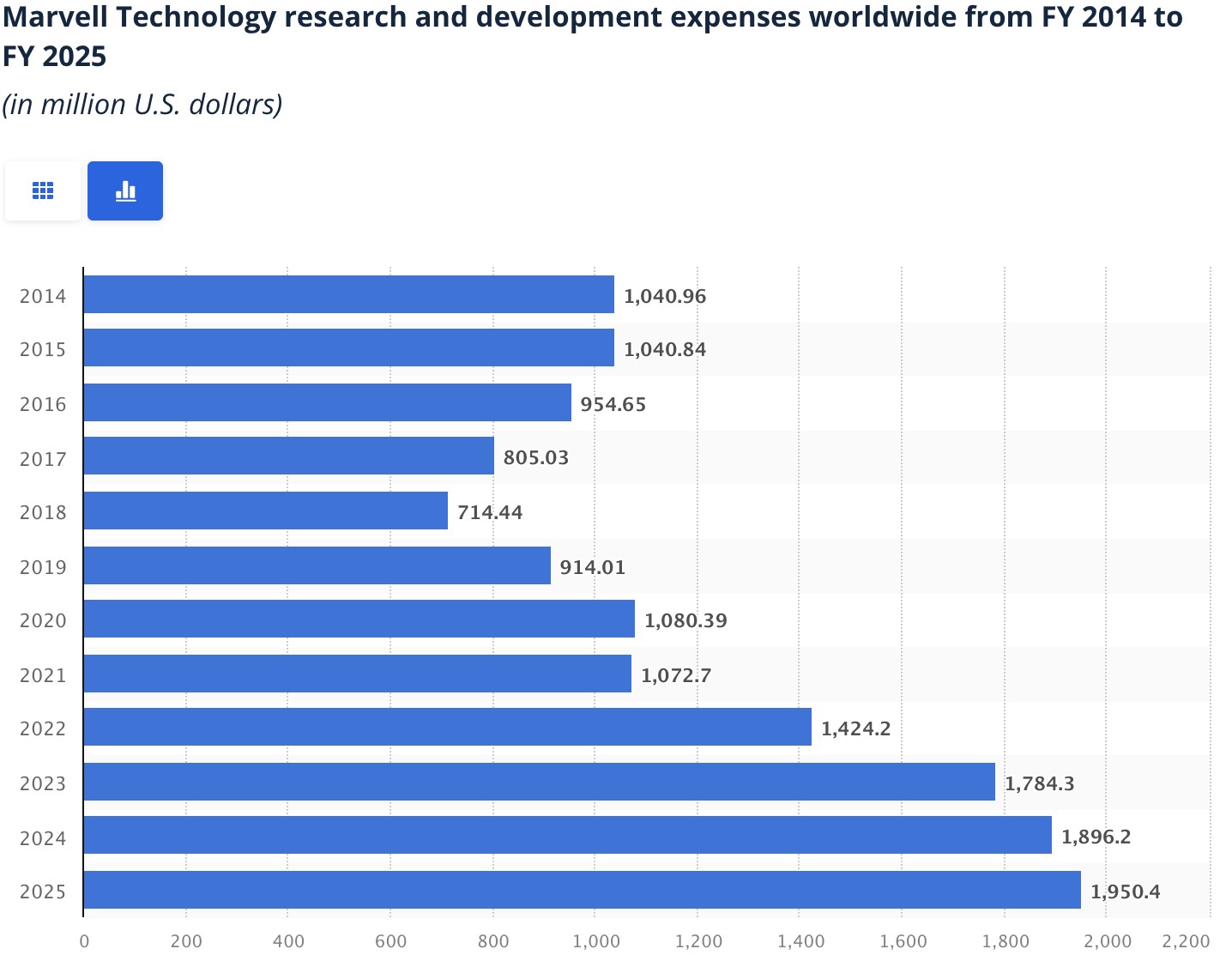

These gains were achieved even as R&D spending remained high, a reflection of ongoing investment in bespoke silicon creation. CapEx was minimal at $69.9 million for Q4, as management was clearly maintaining a focus on asset-light scalability. Inventory turns decreased to 3.5x but are solid by the move towards longer-cycle hyperscaler sales.

Source: Statista

Free cash flow trends are also revealing. Marvell's twelve-month trailing (TTM) free cash flow yield is 0.38%, which is well under the industry average. Yet this is also distorted by the capital return cycle. With capital returning to normalized ranges and product mix strengthening, FCF conversion is likely to reaccelerate in FY26 provided non-core segments continue to decline.

With the minimal dividend yield and share repurchases of ~$200 million in the Q4 period, Marvell is still managing a disciplined balance sheet with $948 million in cash and $4.06 billion in debt. The net leverage ratio is still manageable, and with the $531 million of non-GAAP net income realized in Q4 alone, the company is well-positioned to fund future innovation by itself.

Valuation Compression by Stealth

The market assigns Marvell a D- valuation grade, largely driven by its 60.04x forward GAAP P/E and 43.90x EV/EBITDA (TTM). But a deeper look shows this framing is misleading.

First, the non-GAAP forward P/E of 23.14x is close to the sector median (23.14x) and is 41% lower than Marvell's 5-year average of 39.28x. The stock is not overvaluing Marvell; it is devaluing it at the exact same timing when its fundamentals are also strengthening.

Second, the firm's EV/Sales multiple of 7.22x (FWD) also looks rich when you factor out Marvell's 75% AI-related revenue. The implied per-unit multiple of hyperscale infrastructure exposure is very compelling when you make this adjustment. Nvidia is 21x EV/Sales and Broadcom ~9x. Marvell's multiple now looks constricted versus the market's desire for infrastructure enablers.

Further, its 0.49 PEG ratio is a rarity in the current AI bubble atmosphere. The ratio is a reflection of a firm generating strong earnings growth without the multiples of hype, a possible arbitrage for growth investors interested in values.

Our model implies a reasonable FY26 fair value band of $85–$95 per share, applying a 28x multiple to estimated $3.04 non-GAAP EPS (Q1 guidance of $0.61 actualized and repriced modestly). We believe this implies 30–45% upside, not from multiple expansion, but from earnings growth converging with narrative compression.

Risk Profile: Is Valuation Mirage or Headwind?

The main risk lies in Marvell’s increasing concentration. With 75% of sales now coming from data center clients, primarily hyperscalers, any slowdown in cloud CapEx or shift toward in-house silicon could materially impact results. Nvidia’s push into full-stack systems, including networking, is a medium-term threat that could compress Marvell’s ASPs or design wins.

Marvell’s GAAP losses, while narrowing, still reflect substantial amortization and restructuring charges tied to past acquisitions. The ability to sustain its non-GAAP earnings quality will hinge on continued demand from Tier 1 cloud providers, successful execution of the AI custom silicon roadmap, and avoidance of pricing erosion as competition intensifies. Another structural threat is inventory normalization. The inventory level of the company rose to $1.03 billion in Q4 FY25, a 20% sequential increase, which might suggest the possibility of demand overshoot or lead misalignment in manufacturing. Finally, the stock's low dividend yield and subdued share-buyback policy reduce its near-term appeal to capital-return or income-oriented investors.

Conclusion

Marvell is not a valuation outlier; it is a strategic outlier. While the surface multiples indicate overvaluation, dig a little deeper and you'll find a company that is in the process of transitioning to high-margin, long-cycle, AI-native infrastructure. With ramping hyperscaler design wins, scaling custom silicon volume, and a PEG ratio that betrays deep undervaluation, Marvell presents asymmetric upside for institutional investors. The market is still valuing it as a commodity chipmaker. Smart capital should view it as a platform infrastructure provider, one that merits rerating.

Recommended Articles