HIMS: When Overvaluation Isn’t What It Seems

- Revenue doubled YoY to $586 million, with net income up 5x and adjusted EBITDA margin expanding to 16% in Q1 2025.

- Average subscriber revenue rose 53% YoY to $84/month, driven by GLP-1 demand and multi-product treatment engagement.

- Deferred revenue jumped $35 million QoQ, indicating front-loaded cash flow and strong cohort retention with long-term monetization visibility.

- CapEx investments in manufacturing and fulfillment build margin insulation and platform control, supporting long-term scalability and valuation re-rating.

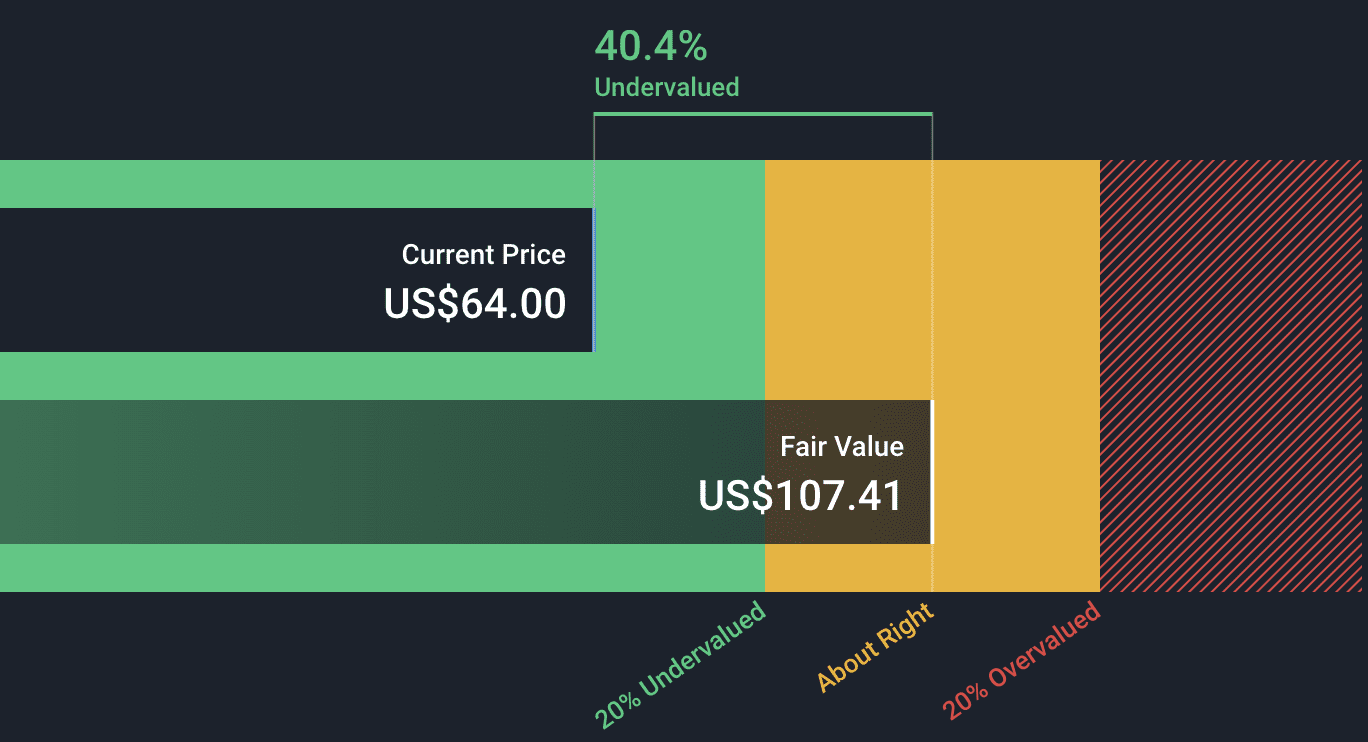

TradingKey - The stock market is sending mixed messages about Hims & Hers Health (HIMS). On the plus side, the shares are trading higher by approximately 16% for the day, continuing a red-hot YTD run; on the other, the stock looks overvalued on paper with GAAP P/E and EV/EBITDA multiples several times the sector median. At first glance, this is a classic case of overvaluation. But that surface-level reading does not capture a greater structural shift. Under the high top-of-page multiples, there is a capital-efficient, vertically integrated telehealth machine, compounding customers and free cash flow at a startup-like pace.

Source: Simply Wall St.

In Q1 2025, revenue jumped more than two-fold YoY to $586 million, with net income quintupled at $49.5 million, and adjusted EBITDA margin to 16%. Subscriber growth was 38%, but most significant is the 53% jump in online revenue per average subscriber per month. That figure, now $84, is a function not just of higher ticket items like GLP-1s, but also of greater engagement over more extensive treatment plans. The platform is not selling pills, its selling the health journey.

.png)

Source: Hims & Hers Investor Presentation May 2025

Hims' model, control of the demand layer, virtual provider network, prescription fulfillment, and increasingly, its own manufacturing presence, forms a vertically integrated health commerce flywheel. Though traditional valuation multiples (such as 80x GAAP P/E) seem extreme, they hide the structural efficiency and lifetime value growth inherent in the business. With cash flow 321% YoY higher and deferred revenue $35 million QoQ higher, Hims is translating marketing to long-lived customer cohorts with prepaid visibility.

Source: Hims & Hers Investor Presentation May 2025

The genuine risk is not overvaluation but misunderstanding the recurring monetization model and operating leverage that begins to drive normalized headline multiples once GLP-1 headwinds subside. Here, we explore the misunderstood valuation optics, Hims' increasing competitive moat, and how balance sheet stability, vertical integration, and personalized platform economics underpin high-conviction long-term theses even with short-term compression for GAAP-based metrics.

Vertical Integration in Practice, From Pharmacy to Factory Floor

What sets Hims & Hers apart in the competitive space for online health is not brand or ad acumen but control of its value chain on a full-stack basis. As opposed to peers that engage the service of third-party vendors and fulfillment networks, Hims is spending big to own both its supply infrastructure and clinical infrastructure. That verticality is translating to unit economics.

CapEx jumped to $55 million in Q1 2025, including acquisition of peptide manufacturing facilities from C S Bio Co. and lab capacities through Trybe Labs. These are not gambles, they are anchored to the future state of personalized healthcare and GLP-1 production, providing Hims with greater pricing power, supply stability, and gross margin insulation. Already, 56% of $586 million of Q1 revenues was booked from deferred revenues, indicating cash capture at inception and margin control.

.png)

Source: GrandViewResearch

Also noted are the $503 billion license purchase with MedisourceRx and related full acquisition of Apostrophe Pharmacy, which demonstrate a larger theme: end-to-end control of the therapeutic process. Such actions hold down free cash flow in the short run through the invested CapEx along with deferred amortization (e.g., EV/EBITDA of 88x TTM), but allow for future efficiency through the streamlining of costs that would otherwise drive variable COGS upward through intermediaries.

Investments have a positive ROI path: fulfillment synergy at the platform level, shortened tail times for customized medications, and insulation from the GLP-1 constraint. Though GAAP P/E in the headlines may not return to normal quickly, the economics are getting better underneath, gross profit almost doubled YoY, and platform-driven fulfillment is building predictability of the margin. Vertical integration is not a center of costs; it is the moat.

Subscription Cohorts and the LTV Engine

Valuation multiples in SaaS are excused where the dollar retention in the net and the LTV/CAC ratios move in the right direction. The same logic is now extending to Hims, which is increasingly a recurring software business masquerading as a healthcare business. Subscriber count for the company came in at 2.4 million (+38% YoY), but the interesting point to note is the $84 average subscriber online monthly revenue, which is a 53% YoY rise.

That is not driven solely by GLP-1 capture. Hims has quietly transitioned membership to longer-duration, higher-margin tiers. With 30- to 360-day subscription rhythms and pay-in-advance plans fueling $110.8 million of deferred revenue (an increase from $75.3 million in Q4), the revenue stream is front-end loaded with cash and back-end loaded with fulfillment cost. That is a classic configuration for margin growth.

Notably, GLP-1-derived products accounted for ~$230 million in Q1 online sales, up from close to zero last year. Even stripping out GLP-1, the residual $346 million is still exhibiting almost 30% YoY growth. This refutes the bear theory that Hims is a single-trick GLP-1 pony. Rather, we have a core subscriber set compounding product usage (augmented by personalized treatment plans along with AI-driven onboarding).

Retention is equally strong. Hims internally has a high LTV to CAC ratio, propounded by front-loading acquisition investment ($201 million of Q1 spend on marketing) countered by deepening products per customer. Gross margin, although declining YoY due to the launches of GLP-1s, is healthy at 73%, and adjusted EBITDA margin grew to 16%. That is to say, more marketing dollars are translating to prepaid, multi-product, low-churn customers. That is to say, Hims' earnings quality is obscured by top-line multiples but supported by depth of subscription, operating leverage, and retention-driven monetization.

.png)

Source: Hims & Hers Investor Presentation May 2025

This Isn’t Overvaluation—It’s Misunderstood Growth

Hims & Hers Health, Inc. appears excessively pricey on paper, but better scrutiny reveals a much richer picture. Its GAAP P/E multiples of 94.82x trailing and 93.25x forward dwarf the sector median, with EV/EBITDA (TTM) at an eye-popping 103.22x. These superficial multiples, which have triggered low grades across the board, ignore several salient facts: back-end-loaded revenue growth, non-cash stock compensation accounting, and front-loaded capital expenditures related to infrastructure buildout. Evaluating valuation ignoring these forces is akin to valuing a house by just looking at the roofing tiles.

More enlightening are the actions behind the curtain. Deferred revenue climbed $35 million quarter to quarter, reserves grew to $273 million, and the company has yet to dip into its new $175 million credit facility. Revenue has doubled more than once year on year, meanwhile, and net income margin has widened to 8% from 4%, a very healthy sign of increasing operating leverage. These are not signs of bloat, but of an efficient scaling business. Traditional valuation frameworks don't capture this subtlety, particularly in platform-like businesses with recurring revenue and steep cost-loading curves.

With the addition of Hims' strategic moats, vertically integrated pharmacies, proprietary fulfillment software, and end-to-end compliance control, it's easier to see why the market is putting a premium on it. Most of its peers farm out what Hims has opted to own. Even with forward EV/revenue of approximately 6.07x (versus Teladoc's 1.5x), the premium seems justified in light of Hims’ cash generation, user retention, and margin slope. On that basis, a reasonable valuation would be between $75–$85 per share on the assumption of ongoing monetization of its GLP-1 pipeline and strong cash generation. This is not an overheated stock, it's one which is fundamentally misjudged by conventional valuation models.

Regulatory and GLP-1 Risk Management

A core bear thesis is around the FDA coming to an answer regarding the semaglutide shortage in February 2025 that restricted compounded GLP-1 supply. But this overlooks two things. One, Hims saw this change coming ahead of time and is now putting capital to work in licensed production and other compounds like tirzepatide through MedisourceRx and C S Bio Co. Two, brand penetration and long-term subscriber acquisition are driven by GLP-1 demand, and even if compounded supply moderates.

Even stripping out GLP-1, online sales grew ~30% YoY, indicating stickiness of the platform independent of this category. Hims also has high-margin visibility through in-house fulfillment and is diversifying across dermatology, mental health, and weight loss subsegments.

Financially, Hims is well set up for a post-GLP-1 surge. Peak CapEx on fulfillment assets is occurring, cash reserves are favorable, and the business has optionality through its $175 million undrawn revolver. Pressure on the gross margin is likely to continue short term due to cycling price changes for personal weight loss products, but SG&A leverage and manufacturing scale should counteract the volatility in the margin.

Conclusion

With 16% adjusted EBITDA margins already delivered in Q1 and marketing expenditure likely to return to normal, the business is positioned to re-expand margins and accelerate FCF in H2 2025. Hims & Hers might appear to be costly based on traditional measures, but that is a function of backward-looking accounting, not forward-looking business momentum. The firm’s vertically integrated platform, subscriber LTV engine, and infrastructure investment support re-rating, especially with overhangs decreasing.

Recommended Articles