Coke Is Trading at Its Steepest Premium to Pepsi in Years. History Says This Is What Happens Next.

Key Points

Coke and Pepsi are supporting their growing dividends with free cash flow.

Pepsi’s gigantic snack business is in the crosshairs of declining demand for packaged foods and snacks.

Pepsi’s yield is higher than Coke’s, and it sports a far cheaper valuation.

- 10 stocks we like better than Coca-Cola ›

Every day, people around the world choose between Coke and Pepsi to quench their thirst for soda. Similarly, income investors may find themselves deciding between investing their hard-earned savings in Coca-Cola (NYSE: KO) or PepsiCo (NASDAQ: PEP).

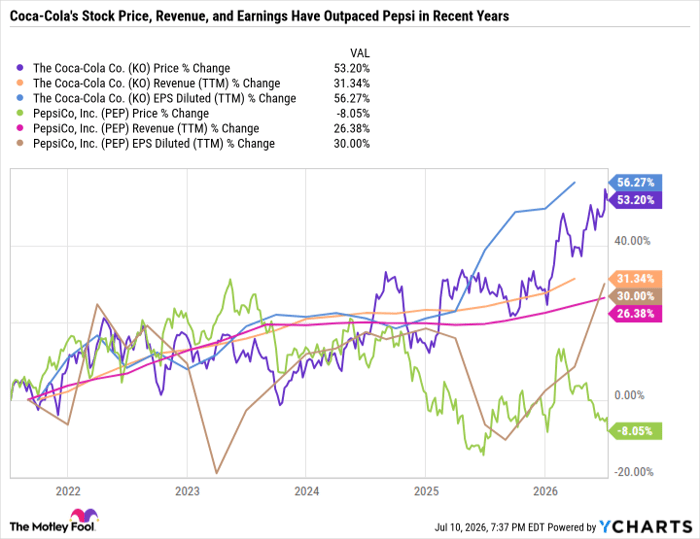

Both stocks have historically fetched premium valuations thanks to their industry leadership, diverse product portfolios, and ultrareliable dividends. But Coca-Cola is crushing Pepsi with a 19.4% year-to-date return, compared with a 4.2% decline in Pepsi stock. And over the past five years, Coke is up 53.2%, while Pepsi is down 8.1%.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Coke's 10-year median price-to-earnings (P/E) ratio is 27.7 -- only slightly higher than Pepsi's 10-year median P/E of 26. But today, Coke's forward P/E is 25.3 while Pepsi's has slumped to just 16 -- the widest disparity in years.

Here's why investors are bubbling about Coke stock, why Pepsi's fizz has fallen flat, and which blue chip dividend stock is the better buy now.

Image source: Getty Images.

Pepsi's North American struggles continue

Pepsi stock was tumbling on July 9 despite decent quarterly results. Investor concerns about declining consumer demand for salty snacks and sugary drinks, as well as inflationary pressures from higher oil prices, may be overshadowing the positives from the quarter.

Pepsi's ownership of Frito-Lay and Quaker Oats, along with its diversified portfolio of beverage brands, gives it a global presence in snacks and nonalcoholic beverages. Pepsi's international segment continues to perform well, with all segments (across product categories and geography) delivering net revenue growth in Pepsi's latest quarter. But Pepsi's North America convenience foods revenue declined, partially driven by lower net pricing, while beverages grew revenue largely thanks to acquisitions made in 2025. When excluding the impact of those acquisitions, Pepsi Beverages North America grew organic revenue by only 1% and saw a 4% decline in beverage volume.

Coke's edge over Pepsi

Pepsi has a lot of moving parts, whereas Coke simply focuses on what it does best: soda, juice, water, sparkling water, tea, coffee, and energy drinks. The beverage category has generally held up better than packaged foods during the slowdown. And Coke's network of bottling partners gives it incredibly high margins.

Coke sells syrups and concentrates to its bottling partners, which mix, bottle, package, and distribute Coca-Cola products. Since Coca-Cola doesn't own or control most of its bottling partners, they effectively function as franchisees in the broader Coca-Cola system, whereas Pepsi's supply chain doesn't have the same operating leverage as Coke. And although it is more diversified in terms of the number of products and categories, Pepsi is heavily affected by shifting consumer preferences. So while Pepsi is well positioned to handle a change in consumer taste for a specific type of snack, the competitive advantage of having so many different products means little if the prevailing trend is an overall decline in snack demand.

KO data by YCharts

Coke has been crushing Pepsi because it's growing its revenue and earnings more rapidly, its margins are far higher, and investors are willing to pay a higher price for Coke stock relative to its earnings than for Pepsi.

Coke and Pepsi can afford their growing dividends

Coke is guiding for only 4% to 5% organic revenue growth for the full year 2026. But its margins remain high, and earnings continue to grow faster than revenue. It also plans to generate $12.2 billion in 2026 free cash flow (FCF), which is plenty to cover its dividend.

By comparison, Pepsi is forecasting 2% to 4% fiscal 2026 revenue growth. It plans to convert 80% of earnings into FCF. Analyst consensus estimates have Pepsi earning $8.64 per share in fiscal 2026, which would be $6.91 in FCF based on the 80% conversion -- plenty to cover Pepsi's run rate annualized dividend of $5.92.

So while Coke is certainly performing better, it's not running laps around Pepsi to the point where it should trade at a significant premium. It's also worth noting that both companies have strong track records of increasing dividends. Coke has boosted its payout for 64 consecutive years, compared with 54 years for Pepsi. That gives both companies a seat at the table of Dividend Kings, which are companies with at least 50 consecutive years of dividend increases.

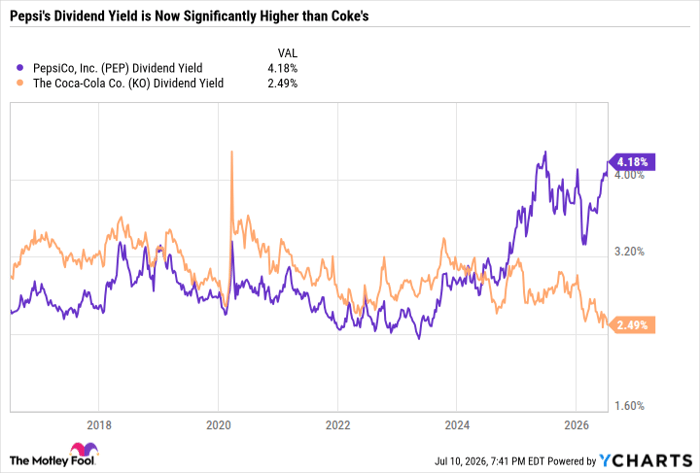

As mentioned, Coke and Pepsi have historically traded at similar valuations. And they have also generated similar earnings and dividend growth rates. But Pepsi's drastic underperformance relative to Coke has pushed Pepsi's dividend yield significantly above Coke's. So not only is Pepsi trading at its deepest discount relative to Coke in years, but the difference in their dividend yields is also at a 10-year high.

PEP Dividend Yield data by YCharts

Pepsi's road to recovery

Historically, when Coke or Pepsi has gotten too expensive, their stock prices have cooled off, giving earnings time to catch up. Or when they're undervalued, the stock price may grow faster than earnings, which is exactly what has happened to Coke in recent years -- bringing its valuation close to its historical average.

Pepsi could enjoy the same recovery if it can regain investor confidence in its turnaround. Pepsi has made efforts to diversify its product portfolio to address wellness trends by introducing healthier versions of its top brands, as well as through major acquisitions focused on healthier products and mini-meals. But even with those efforts, there's no denying that the vast majority of Pepsi's success depends on salty snacks and sugary drinks.

Last September, activist investor Elliott Investment Management took a $4 billion stake in Pepsi, representing roughly 2% ownership of the company. Elliott argued that margin erosion and poor execution across North America have led to Pepsi falling short of its potential. And that reorganizing the business, product portfolio, supply chain, bottler network, and management team could lead to accelerated revenue, earnings growth, and margins. Pepsi received the news well. In December, with Elliott's help, Pepsi announced new strategic objectives to improve the overall business.

Pepsi has progressed on some parts of that plan -- including adjustments to its food and beverage supply chains to lower costs in North American warehouses and fleet delivery. But ultimately, Pepsi will remain in prove it mode until its margins and earnings growth can return to the levels where investors are willing to give it a premium valuation.

Two excellent dividend stocks to buy now

Coke and Pepsi are both great buys now, but for different reasons.

Coke is executing better than Pepsi and is better positioned to endure a prolonged shift in consumer preferences toward wellness options. But Coke is far from cheap, whereas Pepsi's valuation reflects investor uncertainty.

Investors who believe in Pepsi's turnaround are getting an incredible opportunity to buy the value stock while it's in the bargain bin. However, it's understandable if some investors want to wait and see whether Pepsi shows measurable progress toward its turnaround before backing up the truck and loading pallets of Pepsi stock into their portfolios.

Should you buy stock in Coca-Cola right now?

Before you buy stock in Coca-Cola, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Coca-Cola wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $395,679!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,294,805!*

Now, it’s worth noting Stock Advisor’s total average return is 929% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 13, 2026.

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles