Better AI Growth Buy: Broadcom vs Oracle

Key Points

Broadcom and Oracle both are delivering enormous levels of growth thanks to their AI strengths.

These companies are likely to play a major role in the AI story moving forward.

- 10 stocks we like better than Broadcom ›

A couple of years ago, everyone wanted to get in on artificial intelligence (AI) stocks. These players roared higher week after week as companies spoke of the technology's potential -- and in some cases, even started delivering spectacular revenue growth. AI companies continue to deliver fantastic growth, but in recent times, investors have cooled on this investment theme.

Why the change? Investors have worried about the high AI spending levels, and general economic and geopolitical concerns have also weighed on sentiment. But it's important to remember that the long-term AI growth story remains intact: Demand for AI products and services continues to march on, and the technology is delivering results for many companies that apply it to their needs.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Two stocks that are benefiting and should continue to benefit are Broadcom (NASDAQ: AVGO) and Oracle (NYSE: ORCL). But which one makes the better AI growth buy today? Let's find out.

Image source: Getty Images.

The case for Broadcom

Broadcom is a networking giant, offering customers routers and switches that drive connectivity across a variety of devices. And in recent years, the company has put a focus on delivering these solutions as well as custom chips, known as XPUs, to AI customers. This has proven to be a wise decision, as it's supercharged growth.

In the recent quarter, for example, Broadcom's AI revenue surged more than 100% to $8.4 billion, topping the company's forecast. The tech giant predicts this to increase to more than $10 billion in the current quarter. This is as customers rush to get in on networking equipment and XPUs.

Broadcom has carved out an interesting niche in the accelerator space because its XPUs aren't general purpose like those of market giant Nvidia. Instead, they are designed to suit specific tasks -- this differentiation helps Broadcom avoid direct competition with Nvidia, and is leading to an AI win.

The case for Oracle

Oracle has built a database management empire, and this has opened the door to an exciting growth opportunity. The company has developed its own cloud over the years, and today, customers are rushing to it for capacity. But Oracle also made the wise decision to become a multi-cloud player, so that its database customers may harness the power of their Oracle database on all of the major clouds -- from Amazon's AWS to Microsoft Azure. In the recent quarter, Oracle's multi-cloud database revenue soared more than 500%.

And the company's focus on cloud infrastructure has also proven to be a smart move, as this business is booming amid AI demand. Oracle's remaining performance obligations (RPO) are a good sign of what's to come, because they reflect future revenue on services that have been contracted but not yet delivered. RPO jumped more than 300% in the quarter to $553 billion.

As companies shift into the phase of applying AI to their businesses, they will need capacity -- and Oracle is well-positioned to deliver.

Should you buy Broadcom or Oracle?

Both Broadcom and Oracle are delivering explosive growth thanks to the AI boom, and this should continue. So both represent solid additions to an AI portfolio right now. But to determine the better buy, let's start by looking at valuation.

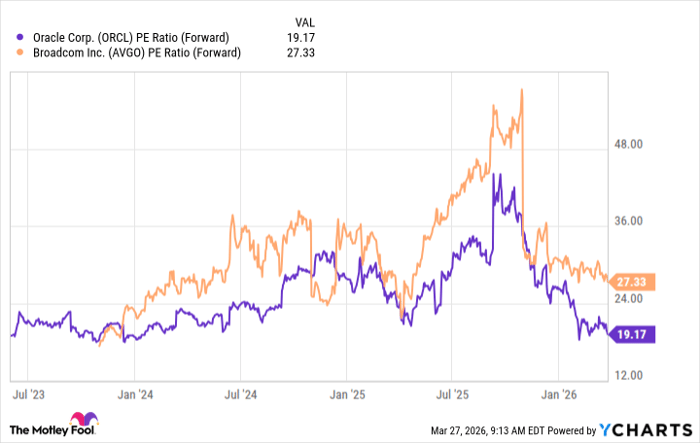

ORCL PE Ratio (Forward) data by YCharts

Oracle and Broadcom each look cheap at today's levels, but Oracle, in particular, looks like a steal. The stock is trading near its lowest in relation to forward earnings estimates in almost two years. So, from a valuation perspective, Oracle offers the best buying opportunity.

Now, let's consider the business opportunity. Oracle and Broadcom should see soaring revenue in the quarters to come as their customers seek capacity from the former and chips and related products from the latter.

But investors may like Broadcom's higher growth rate: Analysts expect the company, which recently completed the first quarter of its fiscal year, to increase revenue by 65% in the current year. Oracle is further along in its fiscal year, having recently reported third-quarter earnings. The company is expected to increase revenue by about 18% in the year.

So, which is the better buy? This depends on your focus. If you're a bargain hunter, you may prefer Oracle, while investors aiming to get in on the biggest growth player might opt for Broadcom right now.

Should you buy stock in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $503,861!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,026,987!*

Now, it’s worth noting Stock Advisor’s total average return is 884% — a market-crushing outperformance compared to 179% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 30, 2026.

Adria Cimino has positions in Amazon and Oracle. The Motley Fool has positions in and recommends Amazon, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles