3 Lucrative Stocks to Buy Now and Hold Forever

Key Points

As the retail auto industry consolidates, Carvana is positioned to thrive and expand.

Ferrari spent decades building its racing technology and a winning brand that would be near impossible to replicate.

Nvidia is becoming the backbone of booming AI development in multiple areas.

- 10 stocks we like better than Nvidia ›

Buying stock in companies with competitive advantages and holding it forever seems like a simple strategy -- until it isn't. Consider that more than half of the current S&P 500 components weren't a part of the index two decades ago. In fact, since 1980, roughly one-third of them have turned over every decade.

Investors may remember in 2000 when Blockbuster said "no thanks" to buying Netflix for $50 million. By 2010, Netflix had disrupted the industry and sent Blockbuster packing into bankruptcy.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

That's all to say that finding lucrative stocks to hold forever is not all that easy. The following three unique companies, however, may just be well-enough positioned to thrive indefinitely.

Bring on consolidation

Carvana (NYSE: CVNA) emerged from potential restructuring or bankruptcy scares over the past three years and has turned into a more efficient, vertically integrated, and profitable company as a result.

Image source: Carvana's Q4 2025 letter to shareholders.

The good news is that the used-car industry is incredibly fragmented and poised to drastically consolidate in the coming years, and Carvana should be in position to thrive. Consider that there are over 43,000 used-car dealerships in the U.S., and the largest dealer brand's market share is 2.3%. And the aggregate market share of the top 100 used-car dealer groups barely tops 11%.

Industry consolidation is already happening, and when it accelerates, the better business models will almost certainly emerge as winning investments -- and Carvana is ready. Until recently, its business model was pure e-commerce with car "vending machines" sprinkled across the nation.

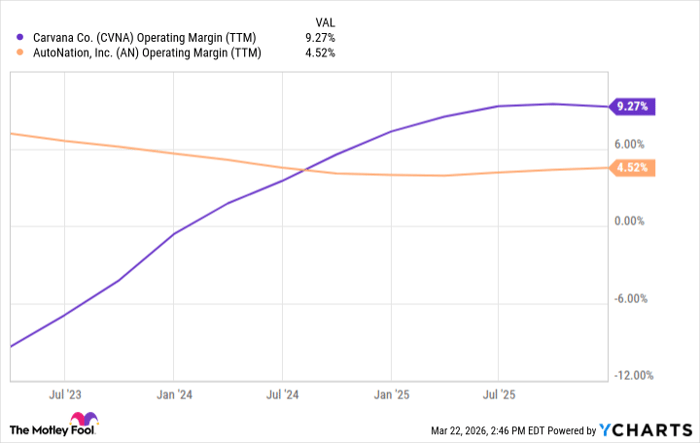

Its national vehicle acquisition strategy, optimized for large-scale inventory and seamless online transaction and pickup options, can build up scale much more quickly than traditional dealership groups -- and it does so at better margins (which are still growing with improved scale) than the largest dealership group, AutoNation.

CVNA Operating Margin (TTM) data by YCharts; TTM = trailing 12 months.

Carvana has built a better mouse trap in an industry where scale matters and competitors are fragmented. It is poised to thrive amid industry consolidation -- all investors need to do is wait patiently.

Win on Sunday, sell on Monday

Even with Ferrari's (NYSE: RACE) overblown roughly 34% sell-off over the past six months, its stock has nearly tripled S&P 500 returns over the past decade. It is arguably the best automotive stock in the world, one of the best luxury stocks, and owns competitive advantages that would take decades to replicate, if ever.

Ferrari has done almost everything the opposite way from the traditional auto industry. For decades, it spent next to zero on traditional advertising, instead relying on racing results and reputation.

While traditional automakers prize high-volume and scale, Ferrari limits its sales and production to drive its exclusivity and pricing power to unthinkable heights. Auto investors loathe dealing with industry cycles and economic downturns, but the Italian automaker is resilient to both, thanks to its large, loyal, and wealthy customer base and long list of returning buyers.

The business consistently ranks among the world's most powerful brands, building its core image over a three-decade span between 1930 and 1960. It had a racing-first strategy, and after dominating many forms of competition in the Fifties and Sixties, the company slowly transitioned from a specialized racing team into a global luxury and performance brand.

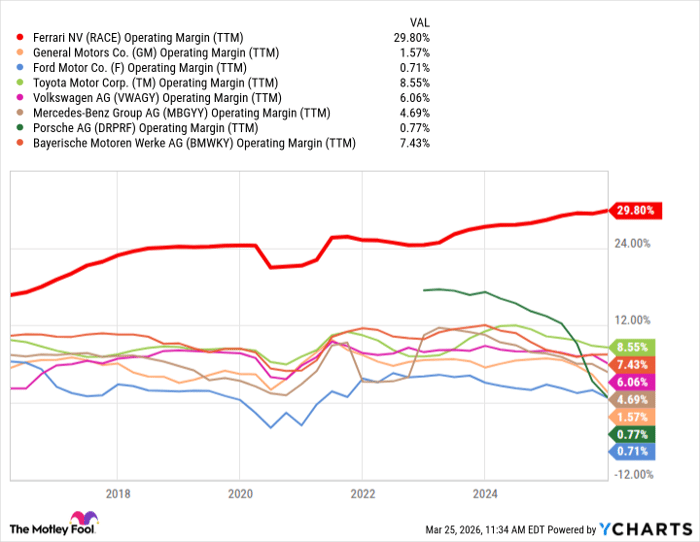

If there's one graph that can summarize how impressive Ferrari's combination of competitive advantages are, it's a long-term graph of operating margins versus industry stalwarts.

RACE Operating Margin (TTM) data by YCharts.

Not only does its operating margins dwarf the competition, but you can also see consistent growth over the past decade, because the company is still building its brand, pricing power, and scale. Ferrari races and wins on Sunday, sells lucrative vehicles on Monday, and investors can take that to the bank for a long, long time.

A strong backbone

There are many reasons to buy into Nvidia (NASDAQ: NVDA) for the long term, including its high growth rates and exceptional gross and operating margins. And there's the fact that it is continuously topping analysts' estimates and expectations, the company's durable competitive advantages, and the built-in developer dependence on its ecosystem. Despite a huge market cap that tops $4 trillion, its valuation is considered fair by most analysts -- and even a bargain to some.

Image source: Getty Images.

Right now, however, a primary reason to buy into Nvidia and hold forever is because of its dominance in artificial intelligence (AI), as it provides the graphics processing units (GPUs) that power AI data centers across the globe. Demand for its chips is strong, and with data center demand expected to grow substantially through 2030, the company is set up to become the backbone of AI infrastructure expansion.

Nvidia even has a growth story that revolves around automaking. The chipmaker's auto business is poised for significant growth driven by surging demand for AI in vehicles.

Driverless vehicles that are rising in levels of autonomy and more software-defined vehicles on the road set the stage for this segment of its business to become a much more significant part of the company's top and bottom lines for decades.

Buy forever

Buying and holding forever isn't as simple as many investors think, and it can honestly be a bit scary to imagine holding forever when the turnover of top businesses happens so frequently. That said, Ferrari, Nvidia, and Carvana are unique, with competitive advantages poised to last for a long time. Investors might be wise to start a position and watch these businesses do the talking.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $503,861!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,026,987!*

Now, it’s worth noting Stock Advisor’s total average return is 884% — a market-crushing outperformance compared to 179% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 30, 2026.

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Ferrari, Netflix, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles