1 Unstoppable Stock To Buy Right Now Before It Soars 91% to Join Nvidia, Apple, Alphabet, and Microsoft in the $3 Trillion Club

Key Points

Demand for semiconductors and the ancillary products needed to support the data center build-out has surged in recent years.

Broadcom's dizzying assortment of customizable chips and infrastructure products is helping sustain the data center boom.

Despite its critical role in the data center space, the stock is still attractively priced.

- 10 stocks we like better than Broadcom ›

There are currently 11 companies worth $1 trillion or more (as I write this), but only four are members of the vaunted $3 trillion club: Nvidia at $4.4 trillion, Apple at $3.7 trillion, Alphabet at $3.6 trillion, and Microsoft at $3 trillion.

Mounting evidence suggests that Broadcom (NASDAQ: AVGO) will join these tech titans in the years to come. The company's products play a crucial role in data centers -- where most artificial intelligence (AI) processing occurs -- and unprecedented demand is fueling robust financial and operating results.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

The semiconductor and data center specialist has a market capitalization of $1.6 trillion (as of this writing), so investors who buy Broadcom right now are looking at potential returns of 91% if the company joins the $3 trillion club. I believe that day is fast approaching.

Image source: Getty Images.

AI is just the beginning

One of the biggest byproducts of the rapid adoption of AI has been the ongoing expansion of data centers needed to support the technology. While Broadcom is widely known for its semiconductors, the company is also a supplier of networking components and accessories that are critical to the operation of data centers.

The biggest contributor to the company's recent success has been the unrelenting demand for its Application-Specific Integrated Circuits (ASICs). These specialized chips can be customized to be more efficient in specific use cases.

As cloud and data center operators look to rein in costs, ASICs have emerged as a viable alternative to Nvidia's flagship graphics processing units (GPUs), which are the gold standard and currently underpin the AI data center market. Google, for example, relies on Broadcom to design and manufacture the high-performance cores at the heart of its Tensor Processing Units (TPUs). The company is also developing a custom AI accelerator for Meta Platforms.

The results are undeniable

Broadcom's financial results tell the tale. In its fiscal 2026 first quarter (ended Feb. 1), the company generated record revenue of $19.3 billion, up 29% year over year, driving adjusted earnings per share (EPS) of $2.05, a 28% increase.

Management believes the company's growth will continue to accelerate. For the second quarter, Broadcom is guiding for revenue of $22 billion, which would represent an increase of nearly 47%, fueling adjusted EBITDA of $15 billion, up 50%.

Broadcom's mathematical path to $3 trillion

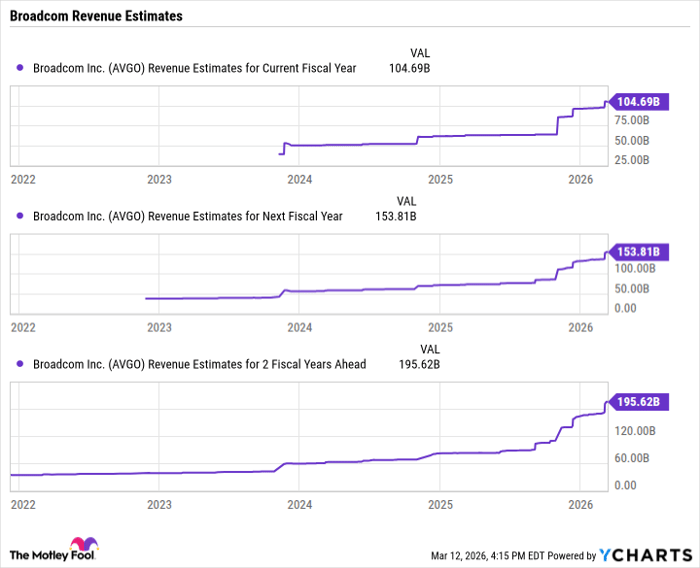

Wall Street expects Broadcom to generate revenue of nearly $105 billion in fiscal 2026, giving the stock a forward price-to-sales (P/S) ratio of 15. Assuming its P/S ratio remains constant, the company will need to generate revenue of $200 billion to support a $3 trillion market cap.

Data by YCharts

As the chart above illustrates, Wall Street predicts Broadcom's revenue will grow to $196 billion by 2028, putting it within striking distance of the $200 million needed for a $3 trillion market cap. However, Broadcom's tendency to beat analysts' consensus estimates and raise its guidance is well-documented, so it will likely reach that benchmark even sooner.

The data center boom continues to gain momentum, with global capital expenditures expected to reach roughly $7 trillion by 2030, according to global management consultants McKinsey & Company. As a leading supplier of data center components and infrastructure, Broadcom is well-positioned to benefit from this trend. Moreover, ASICs are increasingly viewed as a viable, less expensive alternative to GPUs, thereby increasing Broadcom's opportunity.

Despite the blistering rise in its stock price, Broadcom still trades at 30 times forward earnings. Valuing the stock using the more appropriate price/earnings-to-growth (PEG) ratio yields a multiple of 0.44, when any number less than 1 is the standard for an undervalued stock.

Given the available evidence, I think it's clear that Broadcom stock is a buy -- before it joins the $3 trillion club.

Should you buy stock in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $514,000!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,105,029!*

Now, it’s worth noting Stock Advisor’s total average return is 930% — a market-crushing outperformance compared to 187% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 15, 2026.

Danny Vena, CPA has positions in Alphabet, Apple, Broadcom, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Apple, Meta Platforms, Microsoft, and Nvidia and is short shares of Apple. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles