Growth in GE Vernova's Q3 Earnings May Not Translate into Stock Gains

TradingKey - After a sharp run-up, GE Vernova (GEV) is starting to wobble. Over the past two weeks, the stock has been whipsawed—caught between speculative sentiment around the “Trump TACO trade” and pressure from recent analyst downgrades.

Now, all eyes are on Wednesday’s Q3 earnings. In a market that’s running high on expectations, this could be the next key catalyst to either confirm, adjust—or counterbalance—the narrative.

Business Makeup: From Generation to Delivery, GE Vernova Wants to Own the Whole Chain

GE Vernova’s business spans three core segments: power, electrification, and wind.

The power segment is the company’s core revenue engine, anchored by its legacy in gas and steam turbines. Electrification is the critical bridge—covering grid networks and smart transmission systems that move energy to the end user. Wind, particularly onshore and offshore turbines, represents its clean energy transition play.

Together, these three form a full “generate–transmit–serve” stack—which gives GE Vernova a level of vertical integration that few can match in global energy systems.

Right now, generation and electrification are pulling the most weight—both in revenue and profit. And given the accelerating buildout of data centers and grid modernization around the world, these segments are riding strong macro tailwinds.

Power: Stable Growth, Strong Backlog, Mid-Cycle Visibility

As of Q2, generation contributed over 50% of GE Vernova’s total revenues. Gas turbine orders continued to rise steadily, and delivery timelines remain long—which gives the business natural visibility.

The company’s order backlog now sits at $128.7 billion—around 3x annual sales—anchoring short- and mid-term revenue outlook with a high degree of certainty.

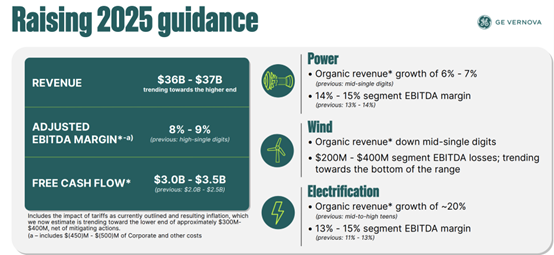

For Q3, management has guided for mid-single-digit organic revenue growth in the generation segment. EBITDA margin is expected to land in the 11%–13% range, which puts GEV at the high end of the peer group globally.

That margin strength has mostly come from successful deliveries of its HA-class gas turbines and the high-margin services business attached to them.

Two events in Q3 could provide further tailwinds: in July, GE Vernova’s 7HA.03 turbines for the Xingda Power Plant in Taiwan officially came online, adding 1.3GW to the local grid. In September, GEV completed the divestiture of its onshore wind blade factory in Szczecin, Poland—freeing up capital and consolidating manufacturing toward its core EU wind hubs.

Electrification: Strong Momentum, Renewed Margin Profile

This division has emerged as the breakout star of late. In Q2, electrification revenue climbed 20% YoY to $2.2 billion, fueled by aging grid upgrades and expanded connectivity infrastructure for renewables. EBITDA margin also jumped sharply—from 7.2% to 14.6%—driven both by operational efficiency and higher-margin product mix.

Total orders dipped from 4.8 billion to 3.3 billion, but backlog grew from 20.7 billion to 27.5 billion—providing solid medium-term visibility.

The company’s “hardware + system” strategy appears to be gaining traction, particularly in the Middle East and Asia. GE Vernova is now delivering fully integrated “generation + grid” packages to clients in Saudi Arabia, South Korea, and other higher-intensity energy markets—including tailored deployments for hyperscale data centers.

For Q3, management expects revenue growth of roughly 20%, with EBITDA margin tracking slightly above Q2’s already-strong performance.

Wind: Onshore Recovery, Offshore Still Under Pressure

Wind energy remains the trickiest part of the story. Revenue in Q2 rose 9% YoY, mainly on the back of improved U.S. onshore deliveries. But deeper structural challenges remain—especially offshore, where project delays, input cost inflation, and soft pricing continue to squeeze margins.

Onshore wind is still dependent on policy incentive continuity (especially tax credits). While tax incentive extensions have helped support U.S. demand, permitting bottlenecks and regulatory friction continue to weigh on pace.

Meanwhile, new tariffs taking effect in 2025 are expected to add 300 - 400 million in incremental costs to the wind business.

For now, management is signaling a cautious tone here: mid-single-digit revenue decline expected in Q3, with EBITDA expected to be near breakeven.

Supply Chain Risk: Still in the Background

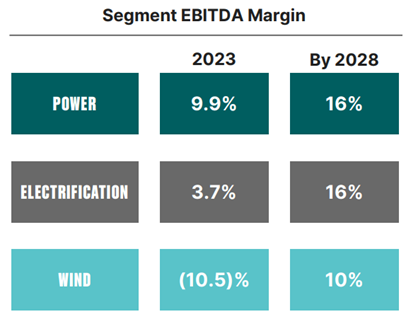

Longer term, management is upbeat about earnings improvement. Back at the 2024 Investor Day, GE Vernova laid out a 2028 margin target: 16% EBITDA for the power and electrification segments, and 10% for wind.

Q3 data suggests GEV is already on track to hit its power target early and is closing in on electrification’s as well—raising market expectations that full targets could be revised upward at the December 2025 Investor Day.

But there’s a wildcard: global supply chains. Like other capital equipment players, GE Vernova remains exposed here. Its procurement footprint spans 100+ countries and over $20 billion in global sourcing. Any meaningful delays in raw materials or high-value parts could impact fulfillment—and weigh on margins temporarily.

Valuation Check: High Expectations Built In

Peer-wise, Siemens Energy is the best comp—competing head-on in gas turbines, grids, and large-scale wind through Siemens Gamesa.

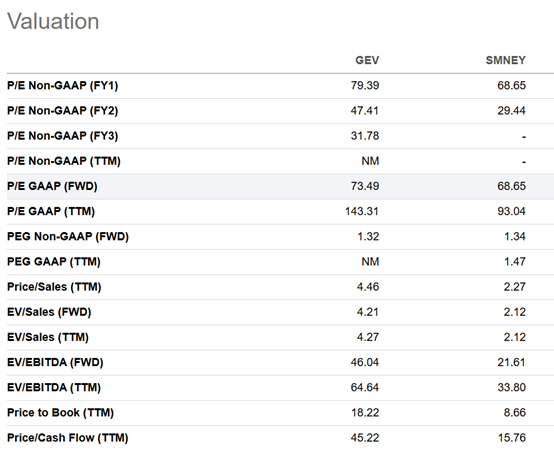

GE Vernova trades at roughly 74x forward earnings, a premium vs Siemens at ~68x. On an absolute basis, valuation is near the upper end of GEV's historical range, reflecting high investor conviction in the long-term growth path.

That said, the setup isn’t extreme. SeekingAlpha data shows GEV’s 2026 revenue growth profile is stronger—and steadier—than Siemens’, which faces a slowdown by then. With electrification margins trending up, GEV’s trajectory supports a more visible profit expansion roadmap, helping justify part of the premium.

GE Vernova Consensus Revenue Estimates

Siemens Energy AG Consensus Revenue Estimates

Street models suggest GEV’s forward PE could normalize to 47x by 2026 as earnings scale.

Still, it’s worth flagging the risk side of the equation. High expectations are already priced in. Any downside surprise—whether from weak wind numbers, supply chain hiccups, or macro factors like higher-for-longer interest rates—could lead to a fast valuation reset. Siemens Energy learned that lesson the hard way in 2023, when quality issues in its wind unit triggered a sudden 30%+ decline. GE Vernova is better diversified and structurally healthier—but in a high-multiple environment, sentiment tends to swing wide.

For existing holders, the setup doesn’t scream panic. The long-term thesis remains intact. But for new entrants, this isn’t low-hanging fruit. With shares near historical highs, waiting for a pullback might be the more risk-aware play.

Recommended Articles