TradingKey 2025 Markets Recap & Outlook | Fed Rate Cuts and End of QT: Is the Strong Dollar Cycle Turning?

TradingKey - The U.S. dollar in 2025 is undergoing a fundamental shift. The 'triple trump cards' that once underpinned the dollar's strength—high interest rate differentials, leading absolute returns, and its favored status among global safe-haven flows—are simultaneously weakening. As the Federal Reserve gradually exits its tightening cycle and fiscal pressures intensify, the relative attractiveness of U.S. assets in international markets is quietly declining.

The Dollar's Ascent and Retreat in 2025

In early 2025, the U.S. Dollar Index (DXY) decisively broke above the 110 mark, extending the 'Trump trade' wave that emerged after the late 2024 elections.

This surge stemmed from market expectations for President Trump's new term policies—namely, that protectionist trade measures, expansionary fiscal policies, and deregulation would stimulate U.S. economic growth beyond forecasts. With Republicans controlling both chambers of Congress, investors generally favored asset classes poised to benefit from an environment of high growth, high inflation, and 'America First' policies.

However, by April, this expectation-driven trading logic rapidly dissipated. The primary reason was that the Trump administration's proposed large-scale tariff plans were deemed overly aggressive and even chaotic, fueling escalating concerns about recession and a global trade war. 'America Greatness' rhetoric gradually faded, while the Federal Reserve, facing increased political pressure, found it challenging to independently stabilize monetary tools, signaling a decline in policy credibility to the outside world.

Concurrently, U.S. economic data increasingly indicated a slowdown in growth, and the job market was no longer as robust as before. Against this backdrop, the Federal Reserve cut the federal funds rate target range three times from September (each by 25 basis points), with the year-end rate range settling at 3.50%-3.75%. Combined with the cumulative 100-basis-point reduction in 2024, the 'interest rate differential premium' that had long supported the dollar gradually weakened.

In addition to lowering interest rates, the Federal Reserve made another decision at year-end: formally ending its multi-year balance sheet reduction (i.e., quantitative tightening) operations. Effective December 1st, the Fed ceased actively withdrawing liquidity, marking the official conclusion of the extensive monetary tightening phase initiated since the outbreak of the pandemic.

Some analysts believe this indicates the Federal Reserve is attempting to mitigate a certain degree of liquidity depletion risk within the system, though it remains distant from true easing (such as restarting quantitative easing).

Historical experience shows that changes in the Federal Reserve's balance sheet size often have a critical impact on the U.S. Dollar Index (DXY).

Quantitative tightening (QT) strategy acts like a 'vacuum cleaner' constantly drawing liquidity from the financial system. This mechanism helped push up real interest rates and relevant yield curves, thereby indirectly supporting the dollar's rebound. However, when QT operations officially conclude—meaning this 'suction machine' is turned off—the 'draining' mode shifts to a 'still water' state. Even if the central bank does not directly inject funds, the new liquidity supply structure still experiences marginal easing. In this scenario, the theoretical impact on the dollar is neutral, or even slightly bearish.

The U.S. Dollar Index displayed a distinct pattern of a 'strong start, weak finish' in 2025. Although the dollar could still briefly serve as a safe haven during periods of geopolitical tension, its overall downward trend for the year proved irreversible. The DXY has fallen over 9.6% year-to-date, trading near 98.00, marking its lowest point for the year.

【U.S. Dollar Index (DXY); Source: TradingView】

As the Federal Reserve's rate-cutting cycle deepened, the yield advantage of U.S. dollar assets gradually diminished, prompting investors to seek out other higher-yielding currency regions. Particularly after the formal conclusion of quantitative tightening in December, market expectations for a further easing of dollar liquidity accelerated the shift of capital from dollar assets towards globally diversified allocations.

USD/JPY: Policy Adjustments Behind Wide Swings

In 2025, USD/JPY generally exhibited wide-ranging volatility. Influenced by heightened risk aversion in the first half of the year and persistently high U.S. Treasury yields, the Japanese Yen notably strengthened, appreciating over 12% against the dollar cumulatively in the first four months.

However, this rally proved unsustainable, fully reversing in the second half. By September, following Sanae Takaichi's election as Japan's Prime Minister and the introduction of new fiscal stimulus plans, the market bet that the Bank of Japan would accommodate by delaying its rate hike trajectory. This exerted pressure on the yen, causing the dollar to strengthen rapidly in the short term. By year-end, USD/JPY had fallen slightly by approximately 1% for the full year.

【USD/JPY; Source: TradingView】

From a full-year policy perspective, unlike the Federal Reserve which initiated its rate-cutting cycle in September, the Bank of Japan maintained unchanged interest rates for most of the period, reiterating its cautious stance that 'policy needs to await inflation gaining endogenous momentum.' Constrained by factors such as unfulfilled wage growth and still-modest domestic consumption, the BOJ's tightening pace notably lagged that of the Federal Reserve.

Notably, some Bank of Japan board members suggested that Japan's current real policy rate remains among the lowest globally, and exchange-rate-driven imported inflation risks have not been fully dissipated. This provides scope for future interest rate hikes.

Concurrently, another perspective suggests that with government stimulus measures extending over the next one to two years and real wages projected to achieve positive growth in the first half of 2026, economic fundamentals are steadily improving. Such expectations reinforced market assessments that the Bank of Japan would consistently pursue monetary normalization around 2026, driving Japanese government bond yields higher and reducing the uncertainty of a sudden 'hawkish pivot to dovish' policy shift.

In contrast, the dollar itself lacked sustained rebound momentum. With expectations rising for potential further rate cuts by the Federal Reserve in 2026, its asset return advantage came under pressure.

Against the backdrop of diverging monetary policy expectations, the trend of narrowing U.S.-Japan interest rate differentials has become increasingly clear.

Caught in Safe-Haven Sentiment Swings

Repeated global trade frictions and geopolitical risks in 2025 further exacerbated the volatility of the USD/JPY exchange rate.

When the market interprets tariff escalations as 'the U.S. being relatively less affected, while other economies face greater impact,' or when U.S. economic data remains consistently strong, capital typically tends to flow into dollar assets, bolstering the U.S. Dollar Index and consequently driving USD/JPY higher.

During periods of tight dollar liquidity and rising funding demand, risk aversion also tends to boost the dollar's intrinsic value, creating a transmission chain of 'risk event → buy dollar → USD/JPY rise.'

Conversely, when tariff policies directly impact U.S. credit or growth prospects, and the market believes a 'tariff storm' will harm both the U.S. and global economies, capital may be divested from dollar assets, shifting towards traditional safe-haven currencies like the Japanese Yen, leading to a weaker dollar, stronger yen, and a corresponding decline in USD/JPY.

This bidirectional transmission mechanism made USD/JPY susceptible to demand swings as a 'dual safe-haven currency,' driving significant volatility for the pair multiple times throughout 2025.

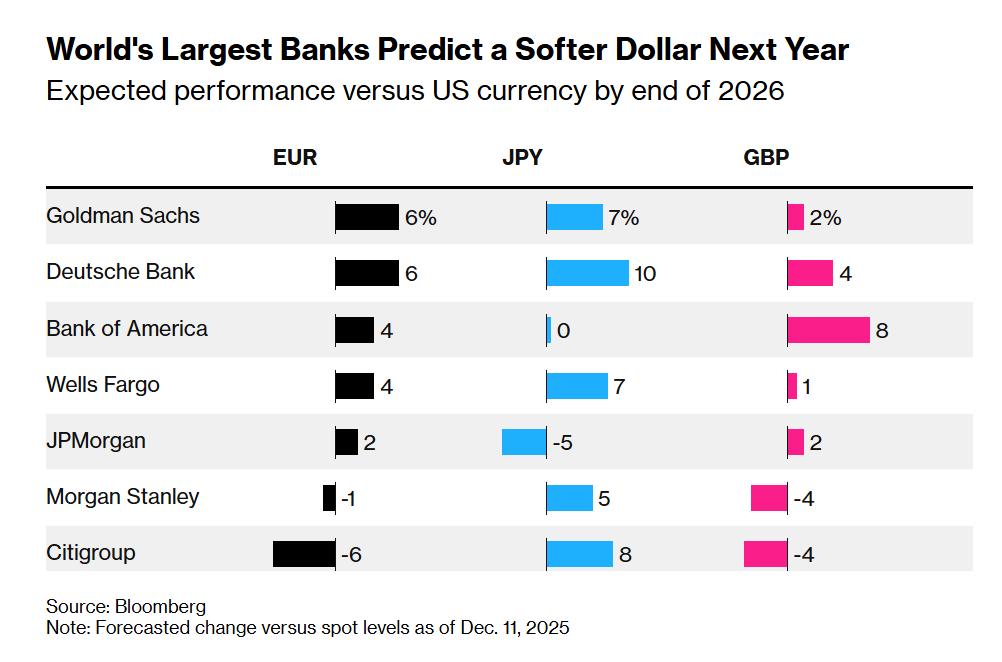

Wall Street Unanimously Bearish: Is the Dollar's Decline Irreversible in 2026?

As the Federal Reserve continues its rate-cutting campaign, being the first among major global central banks to signal easing, several top investment banks predict a renewed weakening of the dollar in 2026, with depreciation pressures significantly increasing.

A Bloomberg survey reveals that over six major investment banks broadly anticipate the dollar will continue to weaken against major currencies such as the euro, yen, and pound, with the Dollar Index potentially falling by another approximately 3% by the end of 2026.

Deutsche Bank, Goldman Sachs, JPMorgan Chase, and other investment banks state that given the Federal Reserve's inclination for further rate cuts, while other major economies such as the European Central Bank and the Bank of Japan may choose to hold steady or even gradually raise rates, this monetary policy 'divergence' will erode the dollar's relative yield advantage.

George Saravelos, Deutsche Bank's Global Head of FX Research, emphasized that the dollar's current valuation remains in a historically high range, inconsistent with its economic fundamentals.

Meanwhile, the team of Goldman Sachs analyst Kamakshya Trivedi pointed out that the market is gradually pricing in improving growth prospects for non-U.S. economies into exchange rates. Historical patterns indicate that when the growth momentum of major global economies strengthens in unison, the dollar typically tends to depreciate relatively.

Concurrently, a segment of analysts holds an opposing view. They believe that driven by the artificial intelligence innovation cycle, the United States may still maintain a leading growth trajectory, thereby attracting more investment inflows and stabilizing the dollar's valuation.

For instance, analysts at Citigroup and Standard Chartered both mentioned that the U.S. technology dividend supports its manufacturing and capital expenditure expansion, providing continuous impetus for unit capital output. This structural advantage could offset some of the adverse effects arising from rate cuts.

“We foresee signs of a ‘dollar cycle resurgence’ potentially emerging in mid-to-late 2026,” wrote Daniel Tobon, head of Citigroup’s analysis team, in their annual outlook. He noted that if the AI revolution persists and drives improved real growth, the U.S. would retain its ability to attract capital, thereby mitigating the aforementioned depreciation pressures. “The continued advancement of technology-driven prosperity will be a significant force for sustained expansion in the capital account balance.”

Recommended Articles