CoreWeave Shares Fall for Five Days, 7x Leverage Becomes Concern, Memory Long-Term Agreements and Customer Concentration Risks Highlighted

TradingKey - As one of the most closely watched emerging cloud computing companies in the AI infrastructure sector in recent years, CoreWeave ( CRWV) once, with the strong support of Nvidia ( NVDA ), its GPU computing power leasing business, and the high-speed growth driven by the AI wave, quickly entered the spotlight of the capital markets.

However, as the market enters a new phase with a greater focus on earnings quality and financing capabilities, this AI-native cloud service provider is facing its toughest test since going public.

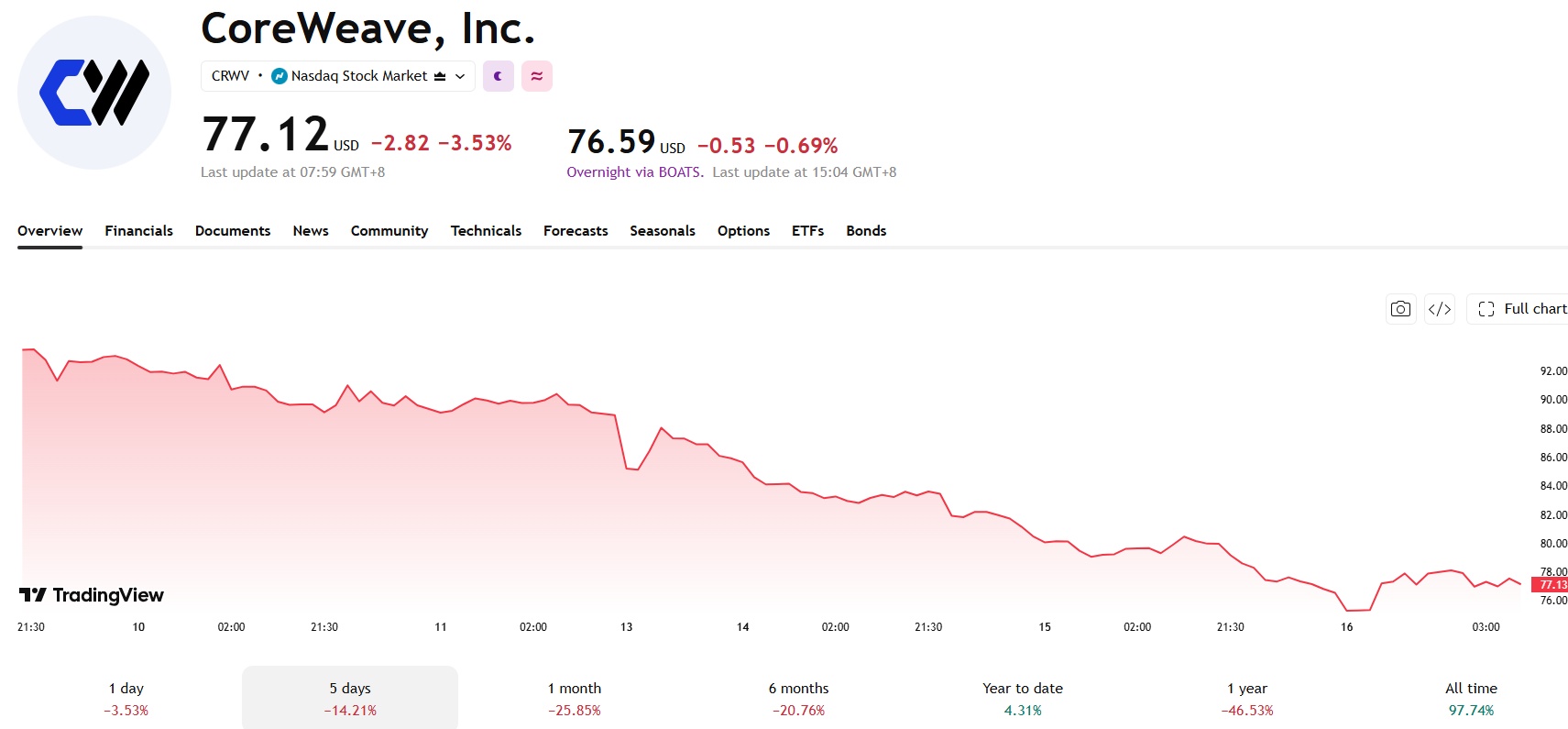

Recently, CoreWeave's stock price has continued to weaken. On Wednesday, the company's shares fell another 3.5%, closing down for the fifth consecutive trading day, with a cumulative decline of over 14% over those five trading days.

Source: TradingView

Looking at a longer timeframe, in less than a month, the company has twice experienced sharp multi-day corrections; previously, during six consecutive trading days ending at the end of June, the stock price had fallen by nearly 20% cumulatively.

Although many Wall Street institutions still maintain positive ratings, with the average target price still showing significant upside potential compared to the current stock price, short-term market sentiment has clearly turned cautious.

Behind Rapid Growth, High Leverage Becomes the Biggest Concern

From an operational perspective, CoreWeave continues to maintain an extremely rapid pace of growth. Over the past year, the company's revenue grew by more than 130% year-over-year. Benefiting from the continuous explosion in demand for AI computing power, its GPU cloud services and AI infrastructure leasing business have expanded rapidly, driving the company to become a major player in the global AI cloud computing market.

However, the flip side of this rapid growth is massive capital investment.

To build large-scale GPU clusters and data centers, CoreWeave has long relied on debt financing to support its business expansion. Currently, the company's asset-liability ratio remains at a high level, with its debt-to-equity ratio exceeding 7 times, and the capital pressure brought about by continuous expansion continues to accumulate.

Market research firms have pointed out that the company's cash burn rate remains fast, while its highly leveraged financing model makes it extremely sensitive to changes in financing costs. Once interest rates remain high or even rise further, increased financing costs will directly squeeze future profit margins and may also affect the pace of subsequent infrastructure construction.

Gil Luria, an analyst at D.A. Davidson, believes that compared with other AI infrastructure companies, CoreWeave's biggest specific risk lies in its significantly higher reliance on debt financing; therefore, the impact of changes in the interest rate environment will be more direct.

Last week's Fed minutes revealed that officials had discussed reasons for a rate hike in June, which temporarily triggered market concerns over rate increases. Although subsequent inflation data came in lower than expected, cooling those rate-hike expectations, the potential risk of rising financing costs still hangs over the heads of highly indebted companies like CoreWeave, directly eroding the company's financial flexibility.

Memory Price Fluctuations Bring New Operating Risks

In addition to interest rate pressures, significant volatility in memory prices has also become a new challenge for CoreWeave.

To secure a stable supply of AI computing infrastructure, CoreWeave signed long-term memory procurement agreements with chip giants such as Micron Technology and SanDisk, which typically include price floor clauses.

Against the backdrop of surging AI demand, memory prices once soared, but market concerns over a reversal in supply-demand dynamics have persisted—if prices decline in the future, CoreWeave would be locked into higher contract prices, facing risks of elevated costs and inventory write-downs.

Recent media reports indicate that CoreWeave is exploring the use of financial derivatives, including put options, to hedge against potential sharp declines in future memory prices, aiming to mitigate operational risks brought by price volatility.

Although the company did not directly respond to the reports, stating only that it does not comment on market rumors, the news has still sparked concerns among some investors.

Analysts believe that against the backdrop of intensifying competition in AI cloud computing, if companies begin to rely on financial instruments to manage cost volatility, the market may worry whether the profitability of their core business is facing new challenges.

High Customer Concentration, Long-Term Order Stability Remains to Be Seen

Currently, Meta ( META) remains one of CoreWeave's most important customers. The $21 billion long-term computing power procurement contract signed by both parties is a key pillar supporting the company's order backlog and cash flow.

However, Wall Street is concerned that as tech giants like Meta aggressively build their own data centers and accelerate the development of proprietary AI chips, future demand for leasing third-party AI cloud computing power may gradually slow down. This structure of heavy reliance on a single customer will face massive uncertainty.

Meanwhile, competition in the AI cloud market is intensifying, and Amazon ( AMZN) AWS, Microsoft ( MSFT) Azure, and other traditional cloud giants are stepping up their AI computing layouts, while new players continue to emerge, putting CoreWeave's market share at risk of being squeezed. Under the multiple pressures of order expectations, industry competition, and profit margins, the company's valuation is facing a significant hit.

For a long time, Wall Street has maintained a cautious stance toward CoreWeave's investment-grade credit quality and financing strategies. The convergence of multiple current risks—such as rising interest rates, memory price volatility, customer concentration, and intensifying competition—is now translating these concerns into tangible pressure on its stock price.

CoreWeave's situation also serves as a wake-up call for the market: amidst the AI infrastructure boom, the vulnerability of a highly leveraged expansion model during a tightening financing environment may far exceed prior market expectations.

Recommended Articles