Did Congress Steal Trillions From Social Security's Trust Funds? The Data Tells the Irrefutable Truth.

Key Points

Social Security's financial footing is deteriorating, with the program facing a $29.3 trillion long-term funding shortfall and the possibility of sweeping benefit cuts by the fourth quarter of 2032.

A popular online belief suggests that Congress pilfered trillions from America's leading retirement program, and that returning this cash, with interest, will resolve Social Security's financial woes.

However, every cent of Social Security's "investment portfolio" is fully accounted for and currently earning interest.

- The $23,760 Social Security bonus most retirees completely overlook ›

For most retirees, Social Security income is indispensable. A quarter-century of annual Gallup surveys shows that 80% to 90% of retirees need this payout, in some capacity, to cover their expenses.

But America's leading retirement program isn't on the best financial footing. The newly released 2026 Trustees Report highlights a $29.3 trillion long-term (75-year) funding shortfall, as well as the projected depletion of the Old-Age and Survivors Insurance trust fund's (OASI) asset reserves by the fourth quarter of 2032. While Social Security won't go bankrupt or halt payouts, benefits for retired workers and survivors of deceased workers are at risk of being cut by an estimated 22%.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

If you peruse online message boards, you're virtually assured to find comments placing the blame for Social Security's financial shortcomings on Congress. Specifically, there's the belief that elected officials stole from Social Security's trust funds (the OASI and Disability Insurance trust fund (DI)), and that returning this cash, with interest paid, would fix the program.

There's just one problem: this long-lived and popular belief of Congress pilfering trillions from Social Security's proverbial cookie jar doesn't have a shred of evidence to back it up.

Social Security's most pronounced myth is firmly busted

When the Social Security Act was signed into law in August 1935, one of its provisions stated that the program's asset reserves (i.e., excess income collected that wasn't outlaid for benefits or administrative expenses) would be invested in special-issue, interest-bearing government bonds.

These bonds are backed by the full faith of the U.S. government, which, aside from computer issues, has never missed an interest payment or a bond maturity date. This requirement that the trust fund's asset reserves be invested in special-issue government bonds also ensures that Social Security generates interest income on this excess cash. In other words, Social Security is already receiving interest income on cash held in its asset reserves.

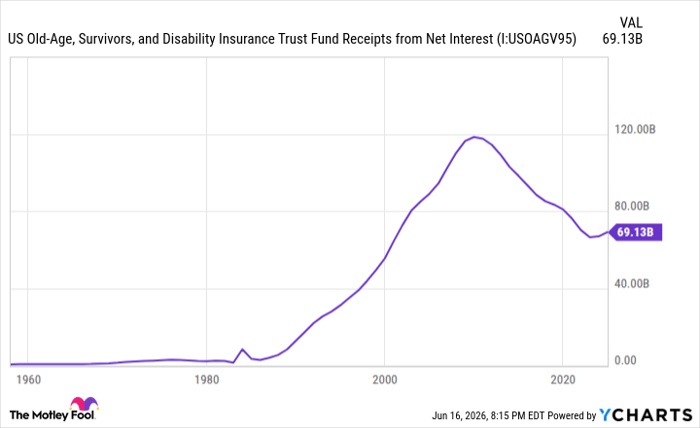

US Old-Age, Survivors, and Disability Insurance Trust Fund Receipts from Net Interest data by YCharts.

Furthermore, the holdings of Social Security's "investment portfolio" are updated monthly and publicly available to anyone who wishes to view them. As of the end of April 2026, the combined OASI and DI held $2.541 trillion in asset reserves, which is generating an average interest rate of 2.633%.

Imagine going to your local bank to purchase a certificate of deposit (CD) yielding 4% over the next year. Your bank isn't going to take your cash, stick it in a vault, and allow it to collect dust over 12 months. Instead, it's going to lend out your capital to generate an even higher rate of return than the 4% it's agreed to pay you via CD. Just because your cash is in a CD rather than your checking account doesn't mean it's been stolen or pilfered. Everything is accounted for, just as every cent of Social Security's asset reserves is documented in its investment portfolio.

If these special-issue bonds were fully redeemed and the OASI's and DI's cash placed into a vault to collect dust, Social Security would no longer generate interest income and would be significantly worse off financially. This year, Social Security is forecast to collect $67 billion in interest income from its asset reserves.

The data couldn't be clearer: Congress hasn't stolen from Social Security, every cent is accounted for, and these funds are currently generating interest income.

The $23,760 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income.

One easy trick could pay you as much as $23,760 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Join Stock Advisor to learn more about these strategies.

View the "Social Security secrets" »

The Motley Fool has a disclosure policy.

Recommended Articles