C3.ai Stock Is Down 21% in 2026. Should You Buy the Dip, or Run for the Hills?

Key Points

C3.ai offers a suite of 40 ready-made applications to accelerate the adoption of artificial intelligence (AI) for enterprises.

A major disruption to the company's management team last year continues to impact sales.

C3.ai stock looks cheap at face value, but the company's shrinking revenue could lead to more downside for investors.

- 10 stocks we like better than C3.ai ›

Artificial intelligence (AI) has already created trillions of dollars worth of value for investors, but not every stock in this space has been a winner. C3.ai (NYSE: AI), for instance, is down 21% so far in 2026, as investors digest the company's declining revenues and ballooning losses.

Last September, C3.ai founder Thomas Siebel stepped down from his role as chief executive officer (CEO) to deal with health issues. He played a pivotal role in attracting new customers and maintaining relationships with existing ones, so his departure led to a sharp decline in the company's sales.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

However, Siebel returned to the CEO role on May 8 and is laser-focused on getting C3.ai back on track, so should investors buy the stock while it's still trading in the red for 2026, or is more downside ahead?

Image source: Getty Images.

Helping enterprises unlock the power of AI

Developing AI software from scratch requires billions of dollars' worth of data center infrastructure, and a significant amount of technical expertise. The average business simply doesn't have those resources, so many of them choose to work with third-parties like C3.ai instead.

C3.ai offers a portfolio of 40 ready-made AI applications that can be customized to suit the needs of enterprises in a variety of industries, accelerating their adoption of this revolutionary technology. As an example, oil and gas giant Shell uses C3.ai's apps to monitor thousands of items of equipment so it can conduct preventative maintenance and even predict failures, which minimizes downtime.

Retailers can also use apps like C3.ai Inventory Optimization, which analyzes variations in customer demand to ensure they are ordering precisely enough products, which limits waste. Banks and financial institutions can use the C3.ai Anti-Money Laundering app to identify suspicious transactions with greater accuracy than human-led processes.

Enterprises can access C3.ai's suite of apps through all major cloud providers, including Amazon Web Services, Microsoft Azure, and Alphabet's Google Cloud. This allows them to seamlessly integrate AI into their existing digital environments, and it means they can tap into the data center computing capacity on offer from their cloud provider to scale their usage as necessary.

C3.ai expects sales to continue declining

C3.ai generated $250.3 million in revenue during fiscal 2026 (ended April 30), which was a whopping 35% decline from the prior year. Stephen Ehikian, who served as CEO in Siebel's absence, initiated a complete restructure of the company to limit the damage from the sharp decline in sales.

Unfortunately, his efforts couldn't prevent a $470.4 million loss at the bottom line in fiscal 2026, which was 63% higher than the company's loss in fiscal 2025. With just $575.4 million in cash, equivalents, and marketable securities on hand at the end of the fiscal year, C3.ai simply can't afford another blowout loss in fiscal 2027, so it slashed roughly 35% of its workforce.

While this will reduce costs and stop some of the bleeding, it will also have negative implications for the company's ability to grow. As a result, management is forecasting revenue of between $210 million and $240 million in fiscal 2027, which would be a year-over-year decline even at the high end of the range.

C3.ai stock looks cheap, but that doesn't mean it's a buy

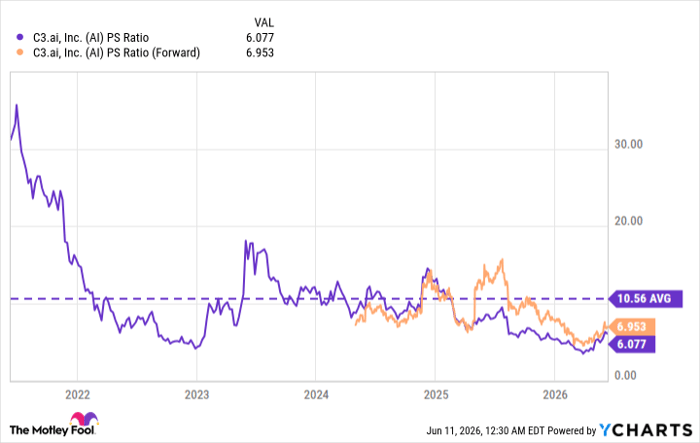

C3.ai stock currently trades at a price-to-sales (P/S) ratio of 6.1, which is below its five-year average of 10.5, so it looks like a good value from that perspective. But because the company's revenue is forecast to shrink in fiscal 2027, its forward P/S ratio is 6.9, so the stock actually looks more expensive when looking into the future.

AI PS Ratio data by YCharts

This is precisely why most investors won't buy into a shrinking business -- it can actually get more expensive over time even if its stock price is falling. It's too early to say whether Siebel can turn C3.ai around over the long term, but all we know for sure is that investors will have to endure at least one more year of declining sales, which makes this a very tough investment.

In summary, a beaten-down stock isn't always a cheap stock. C3.ai will have to prove it can return to growth in a sustainable way before I would consider buying its stock.

Should you buy stock in C3.ai right now?

Before you buy stock in C3.ai, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $438,283!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,257,427!*

Now, it’s worth noting Stock Advisor’s total average return is 938% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 13, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, and Microsoft. The Motley Fool recommends C3.ai. The Motley Fool has a disclosure policy.

Recommended Articles