A Once-in-a-Decade Investment Opportunity: The Best Artificial Intelligence (AI) Stock to Buy in March

Key Points

Nvidia's data center business continues to boom amid accelerating infrastructure investments from AI hyperscalers.

Nvidia has a number of new catalysts that are yet to move the needle for the company.

Nvidia is hovering near its cheapest valuation over the entire AI revolution.

- 10 stocks we like better than Nvidia ›

Since OpenAI commercially launched ChatGPT on Nov. 30, 2022, shares of semiconductor stock Nvidia (NASDAQ: NVDA) have risen 977%. This spectacular rise propelled Nvidia's market cap well north of $4 trillion -- making it the most valuable company in the world.

While Nvidia's gains throughout the artificial intelligence (AI) revolution have been historic, smart investors understand that the company's rally is just getting started.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Let's dig into the tailwinds fueling Nvidia's current trajectory and explore some of the company's major catalysts going forward. From there, I'll assess the company's valuation profile and make the case for why Nvidia looks like a no-brainer stock to buy hand over fist right now.

Image source: Nvidia.

How is Nvidia growing so fast?

During fiscal 2026 (which ended in late January), Nvidia generated $216 billion in revenue -- up 65% year over year. The company's largest source of sales stemmed from its data center business.

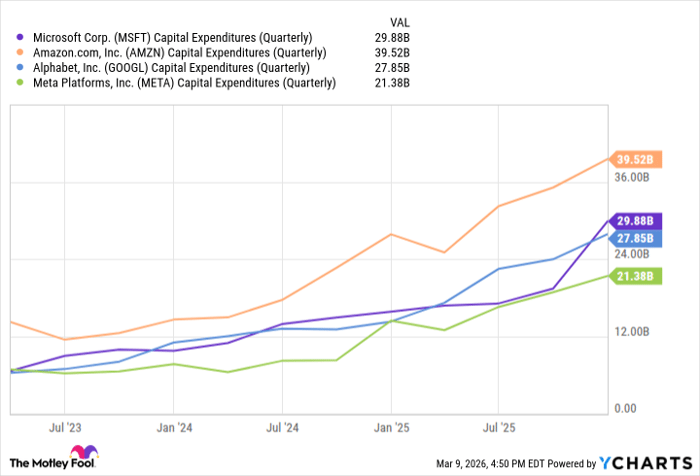

AI hyperscalers, including Microsoft, Alphabet, Amazon, and Meta Platforms, have spent unprecedented sums on infrastructure over the last few years. What's more is that these investments are accelerating -- with big tech projected to spend over $600 billion on capital expenditures (capex) in 2026.

MSFT Capital Expenditures (Quarterly) data by YCharts.

Nvidia's Blackwell graphics processing units (GPUs) and CUDA software ecosystem have become staples in data centers -- cementing the company as a core architect in the training and inferencing of next-generation AI models.

With that said, many of these big tech developers are also exploring designing their own custom silicon architectures. While that may initially appear to be a headwind for Nvidia's chip empire, the company is positioned strategically to grow well beyond the world of data centers.

What opportunities does Nvidia have for the future?

Nvidia's booming data center chip operation has commanded enormous pricing power over the competition. As a result, the company has built a durable profitability profile. In turn, Nvidia has been strategically investing its cash flow into several new growth opportunities.

- In late 2025, Nvidia invested $5 billion in Intel. Through this partnership, Nvidia gains access to the AI PC market -- deepening its ties to the consumer electronics market.

- In October, Nvidia partnered with data analytics specialist Palantir Technologies. Palantir will be integrating Nvidia's AI models into its Artificial Intelligence Platform (AIP) to help operationalize enterprise AI workflows.

- Also in October, Nvidia introduced its Arc Aerial RAN Computer in combination with a $1 billion investment in Nokia.

- Back in January, Nvidia invested $2 billion in neocloud company CoreWeave. Nvidia has long been a supporter of CoreWeave, and this most recent transaction underscores the company's commitment to ongoing AI infrastructure buildouts.

- Most recently, Nvidia invested $2 billion in Lumentum, a specialist in advanced optics and laser components manufacturing.

Above all, the collaborations detailed here share a common theme: Nvidia is working to integrate its tech stack beyond data centers and into new end markets. From consumer electronics to real-time data analytics and telecommunications, Nvidia is diversifying its business into more edge applications across various industry sectors.

Taking this one step further, these partnerships should help Nvidia play a central role in next-generation services such as agentic AI, physical AI, robotics, and autonomous systems as they come to market over the coming decade.

Is Nvidia stock a good buy right now?

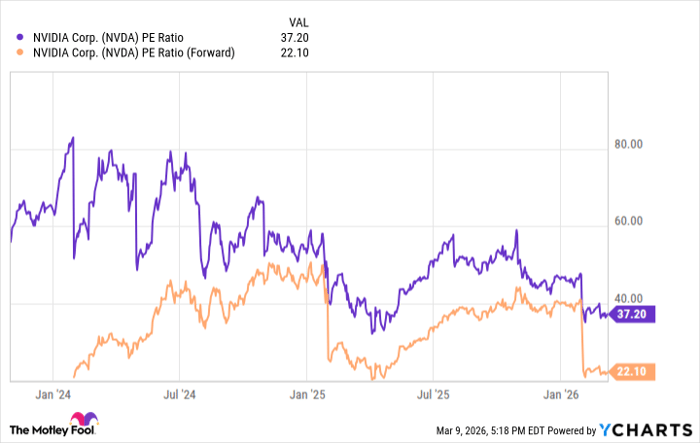

Per the trends below, Nvidia is trading near its cheapest levels in the AI revolution based on price-to-earnings (P/E) and forward P/E multiples.

NVDA PE Ratio data by YCharts.

To me, these dynamics could suggest that the market is starting to price Nvidia more like a maturing business as opposed to one positioned for explosive growth.

Moreover, the discount in its forward P/E relative to prior periods could be a signal that some investors have doubts around big tech's ability to sustain record infrastructure spend and Nvidia's ability to capture it.

If you zoom out and look at the bigger picture, Nvidia's latest earnings report yet again featured monster growth across revenue and profits. Even better, management supplemented this with robust forward guidance.

For these reasons, Nvidia appears to be a great opportunity to buy and hold as numerous AI-driven tailwinds are yet to impact the company's growth profile. While short-term volatility is possible as investors digest the broader macro factors that impact Nvidia, the company remains on a solid footing to continue growing throughout the AI infrastructure era.

In my eyes, Nvidia stock has gotten too cheap to ignore, and smart investors should be taking advantage of the company's attractive price point right now.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $514,000!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,105,029!*

Now, it’s worth noting Stock Advisor’s total average return is 930% — a market-crushing outperformance compared to 187% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 16, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Intel, Lumentum, Meta Platforms, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has a disclosure policy.

Recommended Articles