The Japanese Yen is boxed between a floor it hates and a ceiling nobody trusts

- USD/JPY churns just below 162.50, unable to claim 163.00 yet relentlessly bid at 162.00, the weakest Yen regime since 1986.

- A record 11.7 trillion Yen intervention in the spring bought less than six weeks of relief, and Tokyo is back to near-daily verbal warnings.

- National inflation data on July 23 and the July 28-29 Federal Reserve meeting frame the eventual break from the box.

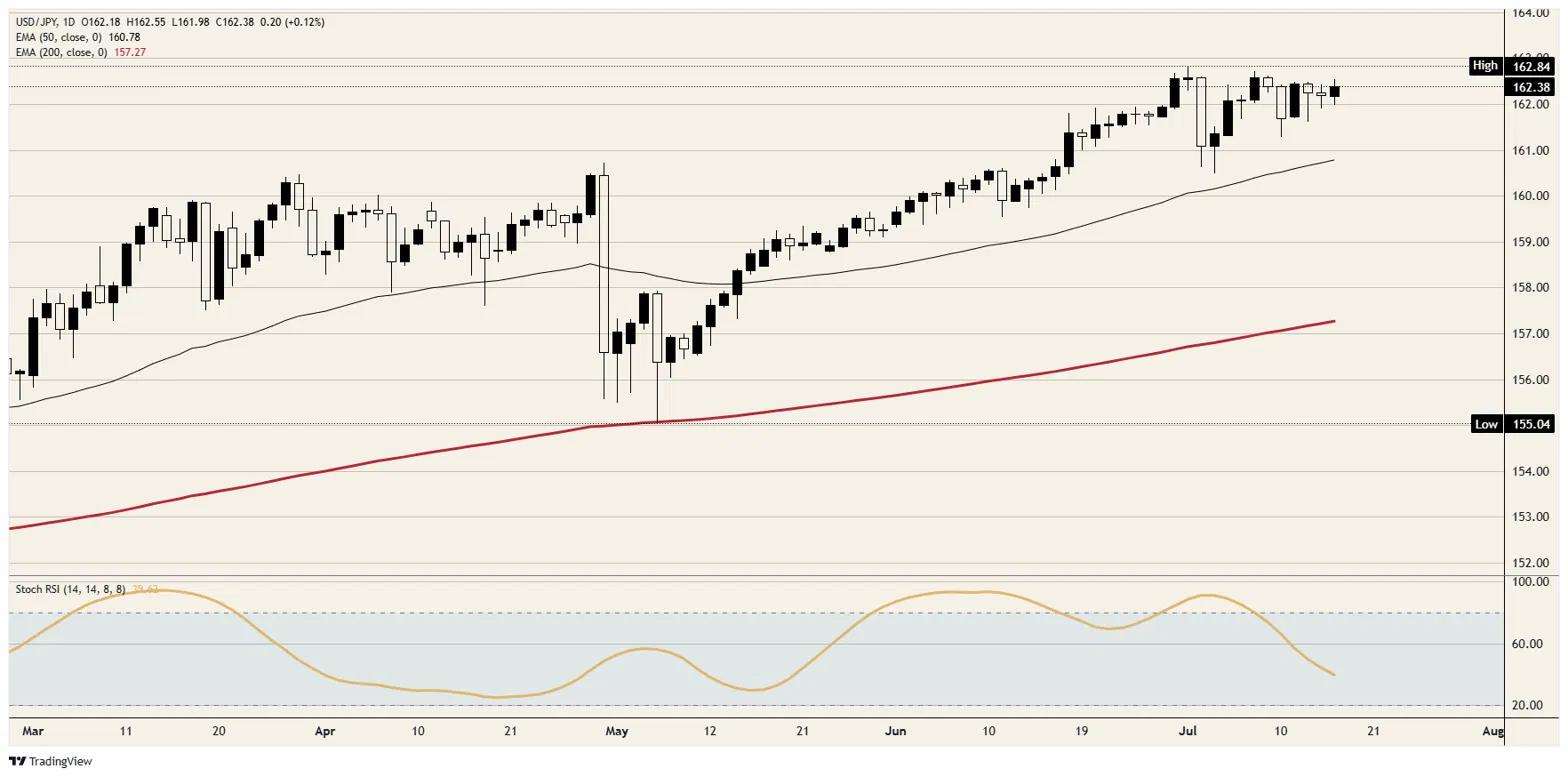

Dollar-Yen has spent the week doing almost nothing at the most dramatic level in four decades. USD/JPY adds a tenth of one percent to hold just below 162.50, short of the cycle top printed just under 163.00, inside the zone traders have taken to calling Tentervention no man's land: close enough to the presumed trigger to fear an ambush, far enough away that the carry still pays out every single day. Two weeks of trade have compressed into little more than a single Yen of range, a coiled spring by this pair's 2026 standards.

The arithmetic refuses to move

The box exists because the carry math remains undefeated. The Bank of Japan (BoJ) hiked to 1.00% in June, its highest policy rate since 1995, and the Yen barely blinked because the Federal Reserve holds its target range at 3.50% to 3.75% with June's projections pencilling in at least one further hike this year. A gap near 275 basis points pays traders to stay short the Yen through every scare, and one Wall Street desk now carries a twelve-month target at 165.00.

Tokyo's counterpunch is structurally capped, and the market knows it. Debt-servicing costs consume roughly a quarter of the national budget this fiscal year, which places a hard ceiling on how far the BoJ can chase the Federal Reserve, while the Takaichi government's fiscal expansion works directly against whatever tightening the central bank manages. Investors can read a budget document, and they have concluded the rate gap narrows slowly or not at all.

Domestic politics keeps leaning on the same side of the boat. Import costs are squeezing households at the weakest exchange rate in two generations, and the political answer has been fiscal support that requires more of the very bond issuance keeping the BoJ cautious. The Yen has become the release valve for a policy mix that refuses to tighten anywhere else.

Pricing the ambush

The Ministry of Finance has already played its loudest card once. A record 11.7 trillion Yen of intervention between late April and late May dragged the pair back to the mid-150s, and the entire move round-tripped in under six weeks, with June 30 printing the weakest Yen level since December 1986 just above 162.50. The Finance Minister has since returned to near-daily assurances that Tokyo stands ready to act, most recently in parliament this week, language that moves the market a little less each time it is repeated.

The result is a market that respects the threat without believing the follow-through. Sell-side desks peg the zone from 162.00 to 163.00 as the live trigger area, rate-check rumours made the rounds in early July, and yet every dip toward 162.00 gets absorbed by carry buyers within hours. The floor exists because the interest gap pays, and the ceiling exists because nobody wants to be the last one long when the ambush finally lands. The war chest is real, but the spring lesson stands: reserves buy time, and the carry buys it right back.

The week that picks the exit

The domestic calendar takes its swing next Thursday. National Consumer Price Index (CPI) data for June lands on July 23 at 23:30 GMT, with the prior headline at 1.5% and the ex-fresh-food core at 1.4%, both below the BoJ's 2% target. Sub-target inflation exposes June's hike as currency defence rather than conviction tightening, and another soft print would drain what little normalization premium the Yen still carries, pressing the pair toward 163.00 from the Japanese side of the ledger.

The American side is doing the heavier lifting anyway. Thursday's 208K jobless claims and a 41.4 Philadelphia Federal Reserve survey keep a hike conversation live for the July 28-29 meeting, and Michigan sentiment follows Friday at 14:00 GMT. Japan's trade data on July 21 at 23:50 GMT rounds out the week, where a 16.8% YoY export surge mostly measures how enthusiastically a weak Yen inflates invoice values. A hawkish Federal Reserve outcome takes 163.00 almost mechanically and forces Tokyo to choose between the ambush and another lecture.

Levels and bias

Resistance: The 163.00 barrier is the tripwire, with the cycle high parked just short of it, and a break opens 164.00 with little but 1986 air beyond.

Support: The 162.00 floor has absorbed every test this month, ahead of 161.50 and the 50-day Exponential Moving Average near 161.00.

Bias: Higher. The carry pays longs to wait while the floor keeps proving itself, so the path of least resistance remains a grind into 163.00, sized for the air pocket below 162.00 if Tokyo finally swings.

USD/JPY daily chart

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The BoJ ultra-loose monetary policy between 2013 and 2024 caused the Yen to depreciate against its main currency peers due to an increasing policy divergence between the Bank of Japan and other main central banks. More recently, the gradually unwinding of this ultra-loose policy has given some support to the Yen.

Over the last decade, the BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supported a widening of the differential between the 10-year US and Japanese bonds, which favored the US Dollar against the Japanese Yen. The BoJ decision in 2024 to gradually abandon the ultra-loose policy, coupled with interest-rate cuts in other major central banks, is narrowing this differential.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

Recommended Articles