Palantir Stock Slipped 35% From Its Peak. Is the Artificial Intelligence (AI) Software Leader a Safe Buy for the Second Half of 2026?

Key Points

Palantir continues to deliver strong growth.

The stock trades at too high a valuation to warrant an investment.

- 10 stocks we like better than Palantir Technologies ›

Palantir (NASDAQ: PLTR) shareholders have had a rough past year. Since setting a new all-time high last October, the stock has marched straight down and is off around 35% from that high. This weakness comes despite reporting incredible results, including an 85% growth rate last quarter.

Palantir is blowing past all expectations and looks unstoppable from a business standpoint. But is it a safe stock to buy in the second half of 2026?

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

I don't think so, and it's not because of anything the business is doing, either; it's a rock-star business. It has to do with one factor: the difference between a great stock and a terrible one.

Image source: The Motley Fool.

Palantir's valuation is still out of control despite its sell-off

Even the best companies bought at the wrong price can turn out to be terrible investments. I think that perfectly sums up a Palantir investment right now, as it's just too highly priced to make any money from it.

As a business, Palantir is crushing it, and the company has signed several major clients to use its artificial intelligence (AI)-powered data analytics software to drive efficiencies in businesses and automate workflows. This has led to strong growth, and with 80% growth expected next quarter (Wall Street analysts have historically underprojected Palantir's actual growth rate), it's still doing just fine.

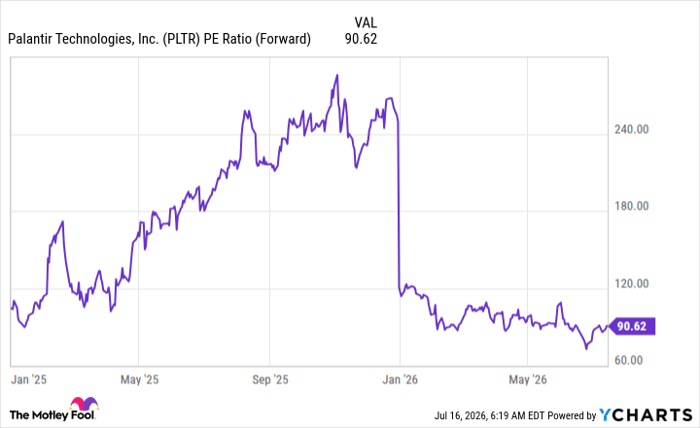

The issue here isn't the business; it's the stock. Over the past few years, Palantir's stock has run up to unreasonable valuations, and it now trades at around 90 times forward earnings.

PLTR PE Ratio (Forward) data by YCharts. PE Ratio = price-to-earnings ratio.

While some may point out that it's cheaper than it was, it's still nowhere near other AI firms growing at similar rates and valued at 20 to 30 times forward earnings. The problem is what this valuation conveys.

Let's say Palantir deserves to trade at a long-term forward earnings multiple of 30. That means Palantir must triple its revenue after 2026's growth has already occurred. Next year, Wall Street analysts project 45% revenue growth. If that growth rate translates directly to an earnings growth rate, it will take three years for Palantir's earnings to triple.

So, it's safe to say that Palantir has all the growth through 2029 priced into the stock already. There's a lot that can happen between now and then, and other stocks could deliver incredibly strong returns during the same time frame, making the opportunity cost of investment in Palantir far too high. As a result, I think investors should look elsewhere for AI stocks, as Palantir may be a solid business, but its stock is just too expensive right now.

Should you buy stock in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $400,964!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,272,955!*

Now, it’s worth noting Stock Advisor’s total average return is 930% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 18, 2026.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has a disclosure policy.

Recommended Articles