Prediction: Microsoft Stock Is Going to Soar After July 29

Key Points

Microsoft stock is down 29% from its record high last year, as investors worry that AI could disrupt the software industry.

But Microsoft has a distinct advantage in the AI race precisely because of its enormous base of software customers.

Microsoft will report Q4 results on July 29, and its stock trades at a very attractive price ahead of the report.

- 10 stocks we like better than Microsoft ›

Microsoft (NASDAQ: MSFT) is scheduled to release its fiscal 2026 fourth-quarter results (ended June 30) on July 29, and I think it could spark a recovery in the company's languishing stock, which is currently down 29% from its record high.

Microsoft has been a casualty of the broader sell-off in the software sector, as investors fear that the growing adoption of artificial intelligence (AI) could render legacy software products obsolete. But the company is proving it can use this revolutionary technology to its advantage, not just in its software business but also in its booming cloud computing segment.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Microsoft stock is heading into July 29 at a very attractive price, so here's why it could be a good long-term buy before the earnings release.

Image source: Getty Images.

All eyes on Copilot adoption

Microsoft developed its own AI virtual assistant called Copilot, which it embedded in the Windows operating system, Edge internet browser, and Bing search engine for free. But it's also available as a paid add-on to the 365 productivity suite, helping users rapidly create content in Word, Excel, PowerPoint, Outlook, and more.

Companies around the world pay for more than 400 million 365 licenses for their employees, and all of them are candidates for the Copilot add-on, so this move represents a huge financial opportunity for Microsoft. By the end of the fiscal 2026 third quarter, ended March 31, enterprises had added Copilot to 20 million licenses, up by an eye-popping 250% year over year.

While pure-play AI companies OpenAI and Anthropic have to acquire customers from scratch, Microsoft can sell Copilot and other AI products into its enormous existing customer base. Therefore, while some investors believe legacy enterprise software is in trouble, Microsoft is turning its product portfolio into a huge advantage in the AI race.

Copilot adoption will be closely watched by investors when the company reports its fourth-quarter results on July 29. I think further triple-digit growth could flip the opinion of some of the more bearish investors.

Azure likely grew at a rapid pace, again

Developing AI models from scratch requires substantial computing capacity, which is typically delivered by large data centers equipped with thousands of specialized chips. Most enterprises can't afford to build this infrastructure themselves, so they rent it from cloud computing platforms such as Microsoft Azure.

Microsoft already operates data centers worldwide, but it's working to double its footprint over the next two years to meet demand for computing power from the AI industry. In fact, as of March 31, the company had a staggering $627 billion order backlog from customers who were waiting for more infrastructure to come online, and that figure doubled from the same time last year.

Azure's total revenue increased by 40% year over year during the third quarter, an acceleration from the 39% growth it delivered three months earlier in the second quarter. But considering Microsoft thinks it can convert its entire $627 billion backlog into revenue over the next two and a half years, I think even faster growth could be ahead.

If Microsoft shows even further growth in its order backlog on July 29, that will only increase my conviction that Azure is on track for more blockbuster quarterly revenue results.

Should you buy Microsoft stock before July 29?

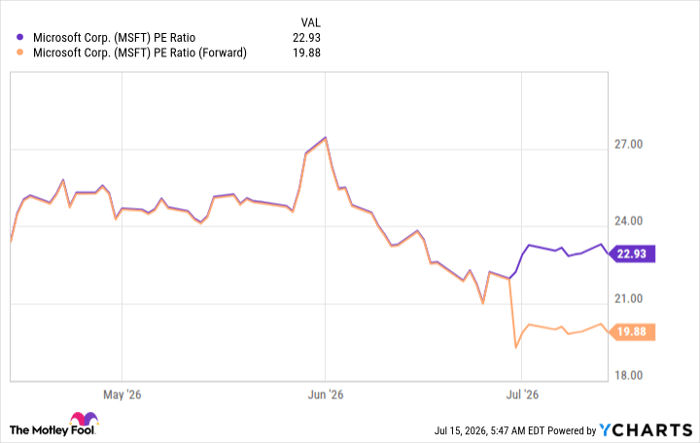

The 29% decline in Microsoft stock from its record high has pushed its price-to-earnings (P/E) ratio down to just 22.9, making it substantially cheaper than the Nasdaq-100 index, which has a P/E of 34.5. In other words, Microsoft appears to be heavily undervalued compared with a basket of its big-tech peers.

Its stock looks even more attractive when looking ahead. Based on Wall Street's earnings estimate for fiscal 2027 (which started on July 1), its forward P/E is 19.9.

Data by YCharts.

If we assume Wall Street's earnings estimate proves to be accurate, Microsoft stock would have to soar by 73% over the next 12 months just to trade in line with the 34.5 P/E ratio of the Nasdaq-100. That isn't unrealistic considering Microsoft averaged a P/E of 32.7 over the last 10 years.

Simply put, investors are getting a fantastic price for Microsoft heading into its latest quarterly report on July 29. It will probably take a series of positive results over the next year or so to rebuild investors' confidence in its software business, but the rewards might be worth the wait.

Should you buy stock in Microsoft right now?

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $396,542!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,299,961!*

Now, it’s worth noting Stock Advisor’s total average return is 931% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 16, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles