Is This Robotics Stock a Potential 10-Bagger?

Key Points

Serve Robotics develops last-mile logistics solutions to lower the cost of making small commercial deliveries.

It has deployed over 2,000 of its robots into food and retail delivery networks like Uber Eats and DoorDash.

Revenue is soaring thanks to a mix of organic growth and a key acquisition, so its stock looks attractive.

- 10 stocks we like better than Serve Robotics ›

Serve Robotics (NASDAQ: SERV) develops last-mile logistics solutions. It believes robots and drones are perfect for delivering food, retail goods, and other small commercial loads, because they are far more efficient and less expensive than current human-driven solutions.

Thousands of Serve's latest Gen 3 robots are already making deliveries through platforms like Uber Eats and DoorDash, and the company's revenue is soaring. Management's guidance suggests the company's best financial results are still ahead, which could be great news for shareholders.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Serve stock is down 51% this year, and it's still trading at a sky-high valuation based on the company's trailing revenue. However, with rapid sales growth potentially ahead and a market capitalization of just $450 million, could Serve be a 10-bagger over the long term?

Image source: Getty Images.

Robotic delivery could be a $450 billion opportunity

It costs somewhere between $8 and $10 to deliver food from a restaurant to a consumer via a human courier and their car. Since the median distance traveled per order in the U.S. is just 2.5 miles, Serve thinks shifting to small autonomous robots could reduce the cost per delivery to just $1.

Serve has deployed over 2,000 of its Gen 3 robots across 20 U.S. cities so far, with a domestic and international expansion in the works. They are powered by Nvidia's Jetson Orin platform, which provides all of the hardware and software required to achieve Level 4 autonomy, enabling robots to safely drive along the sidewalks in designated areas without human intervention.

By 2030, Serve believes robotic and drone delivery will be so widespread that it could be a staggering $450 billion market. If the company wants to capture as much of this opportunity as possible, it can't limit itself to the food and retail segments alone. That's why it entered the healthcare space in January by acquiring Diligent, a company that developed its own Nvidia-powered autonomous robot called Moxi.

Moxi is specifically designed for hospitals, where it transports lab samples, equipment, and medication across departments so nurses and doctors can spend less time managing internal logistics and more time supporting their patients. This expansion into healthcare immediately doubled Serve's geographic footprint to 44 U.S. cities across 14 states.

Serve is producing explosive revenue growth

Serve's revenue rocketed up 578% to come in at $3 million in the first quarter of 2026. The company benefited from the inclusion of Diligent's revenue for the first time, which shows the effectiveness of bolt-on acquisitions for financial performance.

Management now expects Serve to deliver $26 million in total revenue for 2026, marking a near-tenfold increase from the previous year. Looking even further ahead, Wall Street thinks Serve could grow its revenue to over $77 million in 2027 (according to Yahoo Finance), which shows how fast its business is scaling.

But that growth is coming at a cost. During the first quarter, Serve's operating expenses more than tripled year over year to $42.8 million, resulting in a net loss of $49 million for the three-month period. That followed a $101.3 million loss in 2025, so the company is burning through cash at a rapid clip.

Serve had $197.4 million in cash and equivalents on hand as of March 31, so it simply can't afford to lose money at this pace for much longer. In a year or so, management might be forced to raise more money by selling new shares, which would dilute existing investors and hurt their future potential returns.

Could Serve stock rise tenfold from here?

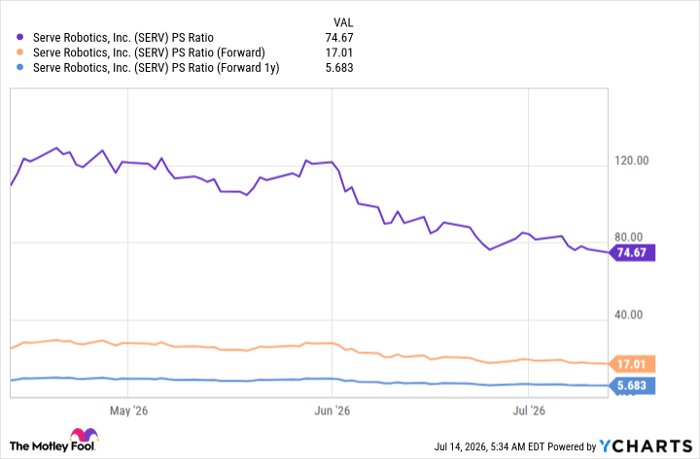

Based on Serve's trailing 12-month revenue, its stock is trading at a price-to-sales (P/S) ratio of 74.7. That means it's almost 12 times as expensive as the Nasdaq-100 technology index, which has a P/S ratio of just 6.3.

However, Serve appears significantly cheaper when valued against its future potential revenue. Based on Serve's 2026 sales guidance, its stock has a forward P/S ratio of 17, and that falls to 5.7 when we use Wall Street's 2027 revenue forecast.

SERV PS Ratio data by YCharts

If Serve stock were to rise tenfold from here, the company's market capitalization would be $4.5 billion. Hypothetically, if it were to trade at a P/S ratio of 6.3 to match the Nasdaq-100, the company would need $714 million in annual revenue to justify its valuation. If its P/S ratio were to hover around 15 instead, which I would consider the higher end of what is reasonable for a company at this early stage, it would need just $300 million in annual revenue.

Serve could achieve $300 million in annualized revenue by mid-2029 if it continues to grow at nearly 200% per year after 2027. However, even if the company's annual growth slowed to just 20% after 2027, it could still achieve $300 million in annual revenue by the year 2035.

As a result, it's certainly possible for Serve stock to deliver a tenfold return from here, but investors need to maintain a long-term time horizon of between five and 10 years to give the business time to scale. Even then, it's no guarantee, but if robotic and drone delivery does become a $450 billion opportunity, Serve only needs to capture a tiny fraction of the market.

Should you buy stock in Serve Robotics right now?

Before you buy stock in Serve Robotics, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Serve Robotics wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $396,542!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,299,961!*

Now, it’s worth noting Stock Advisor’s total average return is 931% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 15, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends DoorDash, Nvidia, Serve Robotics, and Uber Technologies. The Motley Fool has a disclosure policy.

Recommended Articles