PepsiCo’s Q2 Earnings Mixed as Strong International Business Fails to Mask Weak North American Market

TradingKey - Against the backdrop of persistently high global inflationary pressures and weak consumer spending willingness, the food and beverage industry is experiencing unprecedented challenges.

Before the U.S. market opened on Thursday, global consumer giant PepsiCo (PEP) released its second-quarter earnings report for fiscal year 2026. This report presented a sharp contrast, with strong growth in international business driving overall revenue to exceed market expectations, while weak demand in the North American domestic market led to a decline in core margins, and adjusted earnings per share fell slightly short of analysts' expectations.

Following the release of the earnings report, the company's pre-market share price rose slightly by 1%, before subsequently falling over 3%.

Source: TradingView

Overall revenue beat expectations, while earnings performance fell slightly short.

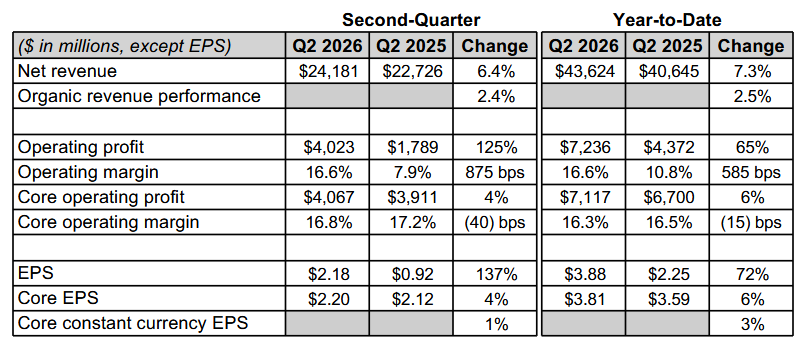

Financial results show that PepsiCo's second-quarter net revenue reached $24.181 billion, up 6.4% year-over-year, far exceeding the market expectation of $23.95 billion. Organic revenue grew by 2.4%, with foreign exchange fluctuations contributing 2.2 percentage points, and acquisitions and divestitures contributing a net of 1.8 percentage points.

Net income attributable to the company was $2.98 billion, representing a significant year-over-year increase of 137%, or $2.18 per share. This growth was primarily driven by lower impairment charges for the Rockstar and Be&Cheery brands, as well as reduced restructuring costs, compared to the same period last year.

However, core earnings metrics were slightly softer. Adjusted EPS came in at $2.20, missing the analyst consensus estimate of $2.21 by $0.01. Core operating profit grew by 4% to $4.067 billion, but the core operating margin contracted by 40 basis points to 16.8%.

Source: PepsiCo

Ramon Laguarta, Chairman and CEO of PepsiCo, stated that the highlight of the second quarter was the strong organic volume and net revenue growth in both the global convenient foods and beverage businesses. Year-to-date global organic volume growth reached its highest level since 2022, though performance in the North American market fell short of expectations, acting as a drag on overall results.

Outstanding performance in international business yields significant results in market expansion.

PepsiCo's international business performed exceptionally well across all regions, with net revenue achieving robust growth, making it the biggest highlight of this earnings report. Organic volume growth was recorded in the Asia-Pacific food business, international beverage franchising, as well as the Europe, Middle East, and Africa regions, demonstrating the success of the company's expansion in global markets.

Particularly in emerging markets, PepsiCo successfully captured opportunities from growing consumer demand through localized product strategies and brand promotion.

This stands in sharp contrast to the sluggish performance in the North American domestic market. The North American convenient foods business saw an increase in volume market share, yet net revenue declined. Although the North American beverage business benefited from acquisition activities in 2025 to achieve net revenue growth, organic volume fell by 4%.

Chief Financial Officer Steve Schmitt admitted that the second-quarter performance of the North American business fell short of expectations, primarily impacted by rising inflationary pressures, which led to a slowdown in the U.S. food and beverage categories as consumer budgets tightened.

Influenced by tensions between the U.S. and Iran, global oil prices fluctuated sharply, with the U.S. national average gasoline price hitting a four-year high of $4.56 per gallon in late May, further dampening consumers' willingness to spend.

Faced with the challenge of weak demand in the North American market, PepsiCo has taken a series of countermeasures.

As price hikes weakened demand over the past two years, PepsiCo cut prices on products such as Lay's, Tostitos, Doritos, and Cheetos by up to 15% in February this year, in an attempt to win back consumers.

At the same time, the company has also revitalized iconic brands like Gatorade and Lay's through a brand-new image overhaul, and is continuously meeting consumer needs by offering diverse options such as portion-control packages, varied ingredients, functional products (e.g., hydration, protein, dietary fiber), energy drinks, and zero-sugar beverages.

Full-Year Guidance Maintained as Market Divergence Persists

Despite facing challenges in the North American market, PepsiCo maintained its full-year 2026 financial guidance, projecting organic revenue growth of 2% to 4% and core constant-currency EPS growth of 4% to 6%.

If foreign exchange gains are included, the midpoint of the guidance implies a core EPS growth rate of 5% to 7%, which is largely in line with analyst expectations. This guidance demonstrates the company's continued confidence in its long-term growth prospects, particularly regarding the growth potential of international markets.

Market opinions remain divided on PepsiCo's future performance.

Evercore analysts noted that weak consumer demand could weigh on upcoming results, advising investors to remain cautious.

Vital Knowledge analysts characterized the earnings report as "generally in line and uneventful, but slightly negative under the hood," primarily reflected in the year-over-year decline in profit margins and weak organic revenue performance in North America.

However, some experts believe the company can overcome these challenges through innovation and brand promotion to sustain its growth. As market competition intensifies, whether PepsiCo can effectively boost local demand in North America while continuing to expand in international markets will be the key factor determining its future performance.

Recommended Articles