Key Information You Need to Know About the Trillion-Won Investment Blueprints of South Korean Memory Giants Samsung and SK Hynix

TradingKey - On June 29, 2026, Seoul time, South Korean President Lee Jae-myung stood at the podium of the Blue House press conference, seated next to Samsung Electronics Chairman Jay Y. Lee and SK Group Chairman Chey Tae-won. This press conference, titled "National Report Meeting on the Three Super Projects for the Great Leap Forward of the Republic of Korea," ultimately turned into an "arms race exhibition" between the two semiconductor giants.

Samsung announced a local investment plan of 2,655 trillion Korean won, while SK Group followed with approximately 2,100 trillion won. Together, the two conglomerates committed to a combined investment scale of about 4,800 trillion won.

It far exceeded the previous market expectation of 2,000 trillion won, prompting Wall Street chip analysts to adjust their models overnight. Some upgraded their ratings on equipment stocks such as Applied Materials and Lam Research, while others began to worry about whether such massive capital expenditure would lead to overcapacity in the future.

Affected by the news, the South Korean stock market experienced volatile trading on Monday. The KOSPI index fell by more than 3% at one point during early trading, Samsung Electronics saw its intraday decline approach 5%, and SK Hynix fell in tandem. Analysts pointed out that the investment plan had been widely anticipated by the market before its announcement, prompting some funds to lock in profits once the news officially broke.

As more details of the press conference were gradually released—including plans by the South Korean government to build four chip factories in the southwest and double DRAM capacity within five years—market sentiment quickly recovered, and the KOSPI briefly turned positive. As of the close that day, the KOSPI fell 0.2% to close at 8,394.65 points, while Samsung Electronics closed down 4.86% and SK Hynix closed down 1.68%.

Samsung Electronics to Invest 265 Trillion Won Across Four Major Regions

According to the plan announced by Samsung, the investment will be distributed by region as follows:

The Seoul Capital Area semiconductor cluster will receive 203 trillion KRW, serving as the absolute core, which will be allocated to the Pyeongtaek Campus and the Yongin National Industrial Park, with a strategic focus on AI semiconductors, HBM4 and HBM5, robotics, batteries, and materials for IT components.

The Honam region will receive 425 trillion KRW, with Gwangju alone accounting for 400 trillion KRW. Samsung plans to convert the former air force base in Gwangju into a semiconductor wafer fabrication plant. In addition, Samsung SDS will build an AI data center in Jeollanam-do, while Samsung C&T will simultaneously construct photovoltaic power plants and hydrogen production facilities.

The Chungcheong region will receive 140 trillion KRW. Samsung Electronics will invest 56 trillion KRW in Cheonan and Onyang to build new HBM fabs; Samsung Display will spend 67 trillion KRW in Asan to construct a next-generation display production base; and Samsung Electro-Mechanics will build an AI server packaging substrate production line in Sejong.

The Yeongnam region will receive 60 trillion KRW. Samsung Electronics will build a humanoid robot mass-production line and a smartphone final assembly plant in Gumi; Samsung Electro-Mechanics will expand its AI chip packaging substrate facility in Busan; and Samsung SDI will increase its investment in all-solid-state batteries in Ulsan.

Samsung's strategic layout is actually straightforward: keeping the most critical wafer fabs in the Seoul Capital Area while dispersing supporting industries like packaging, materials, and batteries to other regions, ultimately forming a nationwide semiconductor industry network. This "core-and-spoke" approach not only meets the demand for capacity expansion but also aligns with the South Korean government's political objective of balanced regional development.

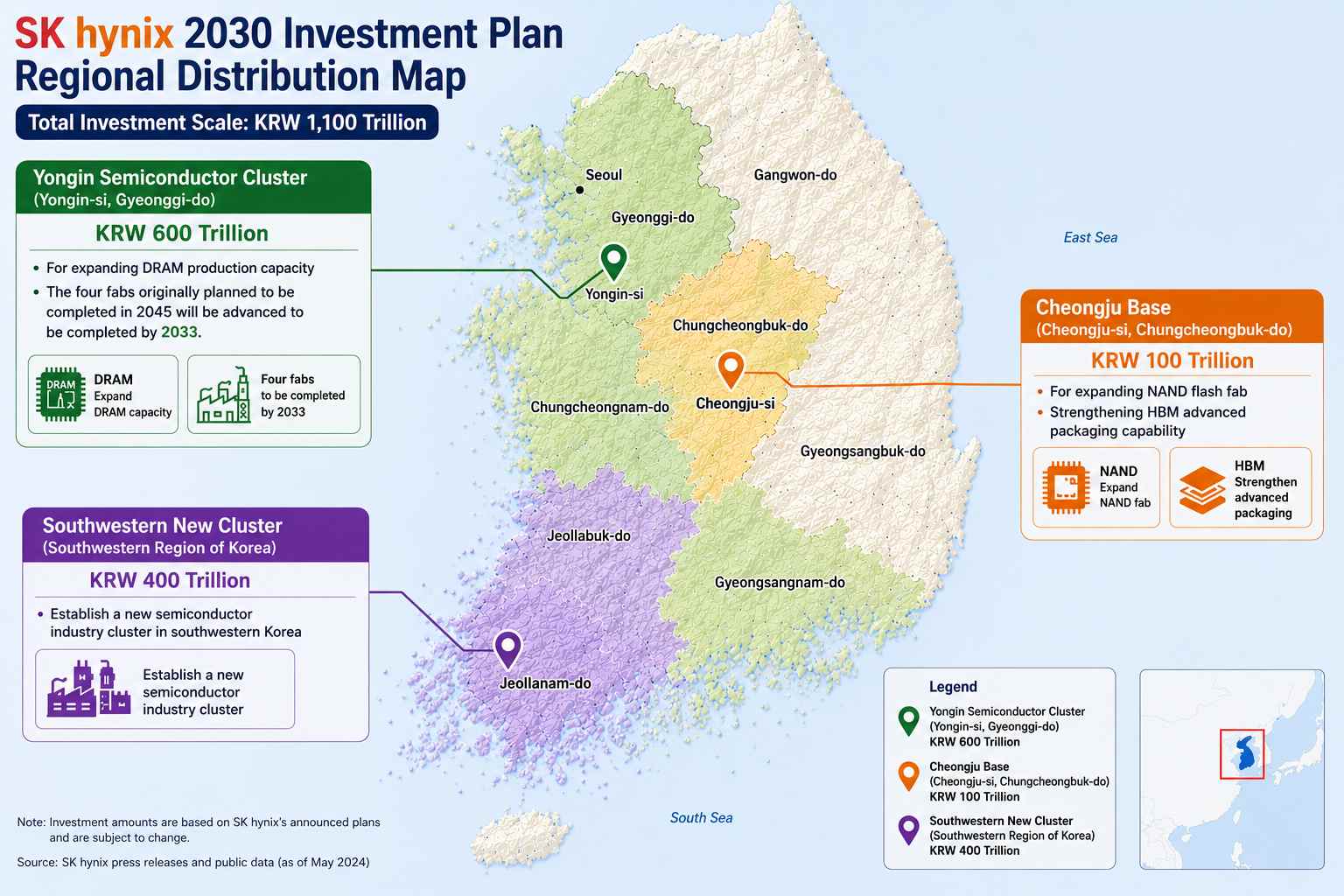

SK Hynix to Invest 103 Trillion Won with Focus on Memory Capacity Expansion

SK Group's investments are more concentrated in the semiconductor supply chain. Chey Tae-won stated at the press conference: "The memory semiconductor market is already facing a severe supply shortage, which is expected to intensify in the future."

This statement is backed by solid performance. In the first quarter of 2026, SK Hynix recorded revenue of 52.58 trillion won, representing a year-on-year increase of 198%; its operating profit reached 37.61 trillion won, up over 400% year-on-year, with an operating profit margin exceeding 72%. The company currently commands over a 55% share of the global HBM market. It can be said that HBM saved SK Hynix, and now SK Hynix intends to use this capital to replicate that success across more HBM-like growth stories.

The SK Hynix Yongin Semiconductor Cluster was allocated 600 trillion won to expand DRAM production capacity. The four wafer fabs, originally scheduled for completion in 2045, will now be fully built ahead of schedule by 2033. The Cheongju site received 100 trillion won to expand its NAND flash memory wafer fabs and strengthen its advanced HBM packaging capabilities. The new Southwestern Cluster secured 400 trillion won to establish a new semiconductor industry cluster in southwestern South Korea.

In addition, SK Telecom plans to build AI data centers with a total capacity of 15GW in phases by 2035. SK Group as a whole plans to invest over 100 trillion won annually within South Korea over the next decade.

There is a subtle difference in the investment logic between Samsung and SK Hynix: Samsung is more inclined toward a diversified layout, covering everything from chips and robotics to batteries; meanwhile, SK is placing almost all of its bets on the semiconductor supply chain.

Government Objective: Double DRAM Capacity, Decentralize the Industry

South Korean President Lee Jae-myung has positioned semiconductors, physical AI, and AI data centers as the "three pillars" of South Korea's industrial upgrade, with the goal of making the country a "leading nation in the AI revolution."

Kim Jung-gwan, South Korea's Minister of Trade, Industry and Energy, stated that Samsung and SK Hynix will jointly build four chip factories in the southwestern region with an investment of approximately 800 trillion won. The Ministry of Industry estimates that the global memory market will quadruple within five years.

Lee Jae-myung indicated that the production bases centered on Yongin and Pyeongtaek are nearing their limits in terms of water resources and infrastructure, and the southwestern region will be developed as a second semiconductor production base.

South Korea plans to invest over 1,000 trillion won in the AI data center sector by 2035, with 81 trillion won to be invested in the Chungcheong region to build an advanced packaging industrial cluster.

There is a clear logical chain among these three goals: expanding production to cope with the surge in memory demand driven by AI; industrial decentralization to free up physical space for production expansion; and building AI infrastructure to extend South Korea's reach from chip manufacturing to the application side.

Who benefits most? Where do the potential investment opportunities lie?

The ripple effects of this colossal investment are beginning to surface, and the sequence and extent of benefits across different segments of the industry chain are gradually becoming clearer.

Semiconductor equipment is the first to benefit. Capacity expansion in memory chips will significantly drive up upstream equipment procurement demand, ushering in a seller's market for semiconductor equipment. On June 29, Applied Materials' stock price surged nearly 10% to hit a record high. With SK Hynix planning to double its wafer capacity within five years and triple it by 2034, the volume of equipment procurement is highly predictable. Equipment is the track with the highest certainty; as long as a fab breaks ground, the equipment must be moved in first.

Construction companies secure the first wave of orders. Some analysts point out that construction firms such as Samsung C&T, Samsung E&A, SK Ecoplant, Hyundai E&C, and GS E&C are directly benefiting from the construction of infrastructure and data centers. Some brokerages even argue that the true highlight lies not in the semiconductor investment itself, but in supporting infrastructure such as power and water supply. These "invisible infrastructures" are often the true bottlenecks to capacity release and are the first budget items to be consumed.

Advanced packaging has become the core track of the HBM era. Samsung and SK Hynix have jointly committed 81 trillion won to set up advanced packaging bases in the Chungcheong province. JCET, a leading domestic OSAT (outsourced semiconductor assembly and test) player, has announced a 7.8 billion yuan investment to build a high-end advanced packaging and testing facility in Lingang, Shanghai. As the mass production of HBM3E and HBM4 progresses, advanced packaging capacity will become the next segment where demand outstrips supply—a point that has been explicitly written into the expansion blueprint for SK Hynix's Cheongju base.

Robotics has been elevated to a strategic industry. Some analyses point out that robotics has been elevated to a strategic industry, and priority should be given to complete systems, core components, and physical AI R&D companies. Samsung's humanoid robotics industrial base in Gumi is precisely the realization of this direction.

The logic of domestic substitution for semiconductor materials continues. The expansion of chip production continues to drive up demand for photoresists, electronic specialty gases, sputtering targets, and polishing materials, while domestic materials manufacturers constantly break through technological bottlenecks in the process of domestic substitution.

With 4,800 trillion won, South Korea is betting its national destiny for the next decade on semiconductors. The scale of this investment plan is unprecedented, but the risks are equally impossible to ignore. SK Hynix's 72% operating profit margin proves the profitability of the HBM era, but whether such massive capital expenditures can yield returns amid the cyclical fluctuations of AI demand remains an open question. In addition, whether South Korea's domestic water and electricity infrastructure can support such a vast expansion of capacity has also become a realistic concern for the market.

What is certain is that the global capacity landscape for memory chips is being thoroughly rewritten. Competitors such as Micron (MU), Kioxia, and Western Digital (WDC) will have to re-evaluate their respective capacity plans.

Recommended Articles