Tesla Q2 Deliveries of 480,000 Units Far Exceed Expectations, Why Did the Stock Price Plummet 7.49% to Record the Biggest Drop of the Year?

TradingKey - On July 2, local time, Tesla ( TSLA) announced its production and delivery data for the second quarter of 2026, delivering a report card that far exceeded market expectations.

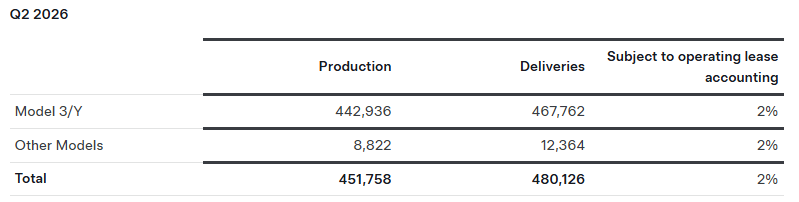

During the quarter, a total of 451,758 vehicles were produced and 480,126 vehicles were delivered, representing a year-on-year increase of 25% and a quarter-on-quarter increase of 34%. This not only significantly exceeded Bloomberg's consensus forecast of 406,000 vehicles but also surpassed Goldman Sachs' most optimistic expectation of 420,000 vehicles.

Source: Tesla

Munster, managing partner of Deepwater Asset Management, believed: "Tesla's delivery data is the first sign that we are emerging from the 'EV winter' that began in March 2024."

However, the stellar data failed to boost the stock price. Tesla plunged 7.49% to close at $393.45 on that day, marking its largest single-day drop in nearly a year.

Source: TradingView

Tesla’s Q2 Deliveries Significantly Beat Expectations

Tesla's deliveries this time significantly exceeded expectations, primarily driven by strong performance in the Chinese and European markets. Garrett Nelson, an analyst at CFRA Research, pointed out that following the elimination of the $7,500 EV tax credit in the U.S., demand recovered faster than expected, while the European market saw a notable boost in consumer enthusiasm for electric vehicles due to rising oil prices fueled by the war in Iran.

Furthermore, Tesla's second-quarter deliveries exceeded production by approximately 28,000 vehicles, indicating that the company successfully digested about 50,000 vehicles of inventory carried over from the first quarter, reversing the previous trend where capacity growth outpaced demand absorption.

In terms of vehicle models, Model 3 and Model Y remain the absolute mainstay, with deliveries reaching 467,762 vehicles, accounting for approximately 97.4% of total deliveries. Meanwhile, demand for the Cybertruck remained weak; were it not for bulk purchases by SpaceX, the overall delivery figures would have been even less impressive.

It is worth noting that this quarter may be the last one in which the Model S and Model X benefit from the "last chance sale" effect, as Tesla ceased production of these two luxury models in May to shift capacity toward its Optimus humanoid robot.

Why did the stock price fall instead of rising?

The main reason for the slump in Tesla's stock price is that the rally over the previous four consecutive trading sessions had already fully priced in the positive news of deliveries exceeding expectations.

Munster believes that investors had already bet on positive delivery data, leaving the market with little reason to remain excited when the news was officially announced.

Furthermore, Tesla's current forward price-to-earnings ratio of 204 times has long detached from the valuation logic of traditional automakers; investors are more focused on the grand narrative of integrating Musk's aerospace, electric vehicle, and artificial intelligence businesses, rather than simple vehicle sales growth.

Although Tesla's energy storage product deployments reached 13.5 GWh in the second quarter, representing a 53% increase from the first quarter, it fell slightly short of the market expectation of 13.8 GWh, failing to deliver an extra surprise to investors.

Truist analyst William Stein emphasized that compared to vehicle deliveries, the development of AI projects, especially FSD (Full Self-Driving), is far more important to Tesla's long-term cash flow and stock price performance.

Intensifying Industry Competition: Tesla Faces Multiple Challenges

Ford ( F) saw its total sales fall 10% in the second quarter, with electric vehicle sales plunging 40.7%. General Motors ( GM) reported a 4.2% decline in quarterly sales and noted the smaller size of the EV market. Lucid ( LCID) posted lower-than-expected deliveries and announced a series of organizational restructurings. Meanwhile, Rivian ( RIVN) delivered a stellar performance, with last-quarter deliveries beating expectations and its full-year delivery target revised upward.

Notably, BYD delivered 557,090 battery-electric vehicles in the second quarter, outperforming Tesla by 77,000 units to reclaim its global leadership position.

To remain competitive, Tesla must not only continue to boost sales but also secure solid profit margins. To achieve its delivery targets, Tesla has relied on price cuts and promotional incentives, which compress profit margins.

In addition, factors such as U.S. inflation, shifting trade policies, and rising chip costs could pose challenges for Tesla in the future.

Recommended Articles