What Makes a Bank Stock Worth Owning for Decades

Key Points

Banks offer consumers and businesses vital financial products and services.

The Great Recession highlighted the risks that can accompany owning a bank stock.

For long-term investors, focusing on banks with strong dividend histories is likely to be a winning strategy.

- 10 stocks we like better than Goldman Sachs Group ›

A small portion of society lacks a banking relationship, which makes it very difficult to operate in the modern world. Most people have at least one banking relationship, if not more. The economy simply wouldn't function without a place for consumers to put cash or a way for them to get loans. And that doesn't even get into the business-related services banks provide.

Most investors should have some exposure to the banking sector. However, not all banks are created equally. You need to tread with care, focusing on financially strong banks that have proven they know how to reward investors with reliable dividends in good times and bad. Here are some banks to consider today.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

The Great Recession was an important lesson

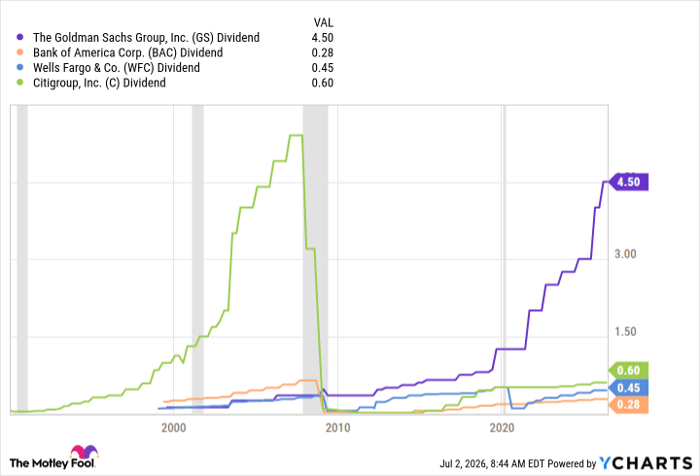

Some of the most iconic U.S. banks got caught up in the housing crisis that precipitated the Great Recession. The list includes Bank of America (NYSE: BAC), Citigroup (NYSE: C), and Wells Fargo (NYSE: WFC). (Some once notable U.S. banks didn't survive the crisis, having taken on too many risky mortgages.) All three cut their dividends. Wells Fargo also found itself caught up in a business scandal that exposed internal operating weaknesses (accounts being created without customer consent). It cut its dividend again in the early 2000s.

These aren't bad banks. And it wouldn't be a mistake to buy any of them. But you can probably do better. For example, Goldman Sachs (NYSE: GS) had a dividend blip in the Great Recession, but for the most part, it survived that difficult period in relative stride. It has many of the attributes an investor should look for in a bank, offering investment and asset management services, among others. However, it appears expensive right now with a 2.9x price-to-book ratio. That's well above the 1.4x five-year average. The dividend yield is a fairly modest 1.8%.

GS Dividend data by YCharts

More compelling choices, north of the border

Toronto-Dominion Bank (NYSE: TD) and Bank of Nova Scotia (NYSE: BNS), more commonly known as Scotiabank, are likely to be more attractive choices. TD Bank's yield is currently 2.6%, while Scotiabank's yield is 3.7%. So you are getting paid more to own them. And, notably, neither was forced to cut their dividends during the Great Recession. That said, like Wells Fargo, TD Bank ran afoul of banking regulators. Only it didn't end up in a position where it had to cut its dividend because of the issue (weak money-laundering controls).

Meanwhile, TD Bank and Scotiabank aren't as cheap as they once were, but neither is as expensive as Goldman Sachs. TD Bank's P/B ratio is 2.5x compared to a five-year average of 1.5x. Scotiabank's P/B ratio is 2x versus a five-year average of 1.3x. One notable difference here is that both TD Bank and Scotiabank are Canadian, where banking regulations are more strict. They tend to operate in a fairly conservative manner throughout their businesses, which span beyond Canada's borders.

That said, there's an added benefit here. Canadian banking regulations have basically resulted in a small number of large banks having protected market positions. TD Bank and Scotiabank are two such banks. So each of them has a very strong foundation. TD Bank's growth is largely in the U.S. market, where it mostly operates on the East Coast. So it has long-term growth potential. It is also focused on expanding in the investment banking space, where Goldman Sachs is an industry leader.

Scotiabank is a bit of a turnaround story. It had skipped over the U.S. market, focusing instead on Central and South America for growth. That plan didn't work out as well as hoped, so it is now refocused on the Mexico-to-Canada trade corridor, with renewed interest in the U.S. market. Given its historically minimal U.S. exposure, it has a sizable growth opportunity in the U.S., too.

Good banks, attractive and reliable dividends

All of the banks highlighted above are well capitalized today. However, the U.S. banking system did not exemplify itself during the Great Recession. Among the domestic banks noted here, Goldman Sachs comes out on top when you examine that deep industry downturn. It is expensive today, however, and you can find banks rewarding you with more generous dividend yields.

Two attractive alternatives are TD Bank and Scotiabank. Neither is exactly cheap, but they are cheaper than Goldman Sachs. And both have diversified businesses, strong operating histories, and attractive growth opportunities in the U.S. market. Take some time to dig into the finer details, and you'll likely consider adding one of these two banks to your portfolio in July.

Should you buy stock in Goldman Sachs Group right now?

Before you buy stock in Goldman Sachs Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Goldman Sachs Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $400,101!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,212,683!*

Now, it’s worth noting Stock Advisor’s total average return is 911% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 2, 2026.

Wells Fargo is an advertising partner of Motley Fool Money. Bank of America is an advertising partner of Motley Fool Money. Citigroup is an advertising partner of Motley Fool Money. Reuben Gregg Brewer has positions in Bank Of Nova Scotia and Toronto-Dominion Bank. The Motley Fool has positions in and recommends Goldman Sachs Group. The Motley Fool recommends Bank Of Nova Scotia. The Motley Fool has a disclosure policy.

Recommended Articles