Bitcoin’s potential recovery in the second half hinges on these 4 catalysts

Bitcoin (BTC) has fallen over 34% in the first half of this year as the King Crypto failed to capitalize on a good semester for risk assets despite the woes from the Iran war. With risk-loving investors increasingly looking at AI-related stocks and with no visible catalysts ahead, Bitcoin enters the second half of the year facing a crucial question: can it rebuild demand or will the correction deepen?

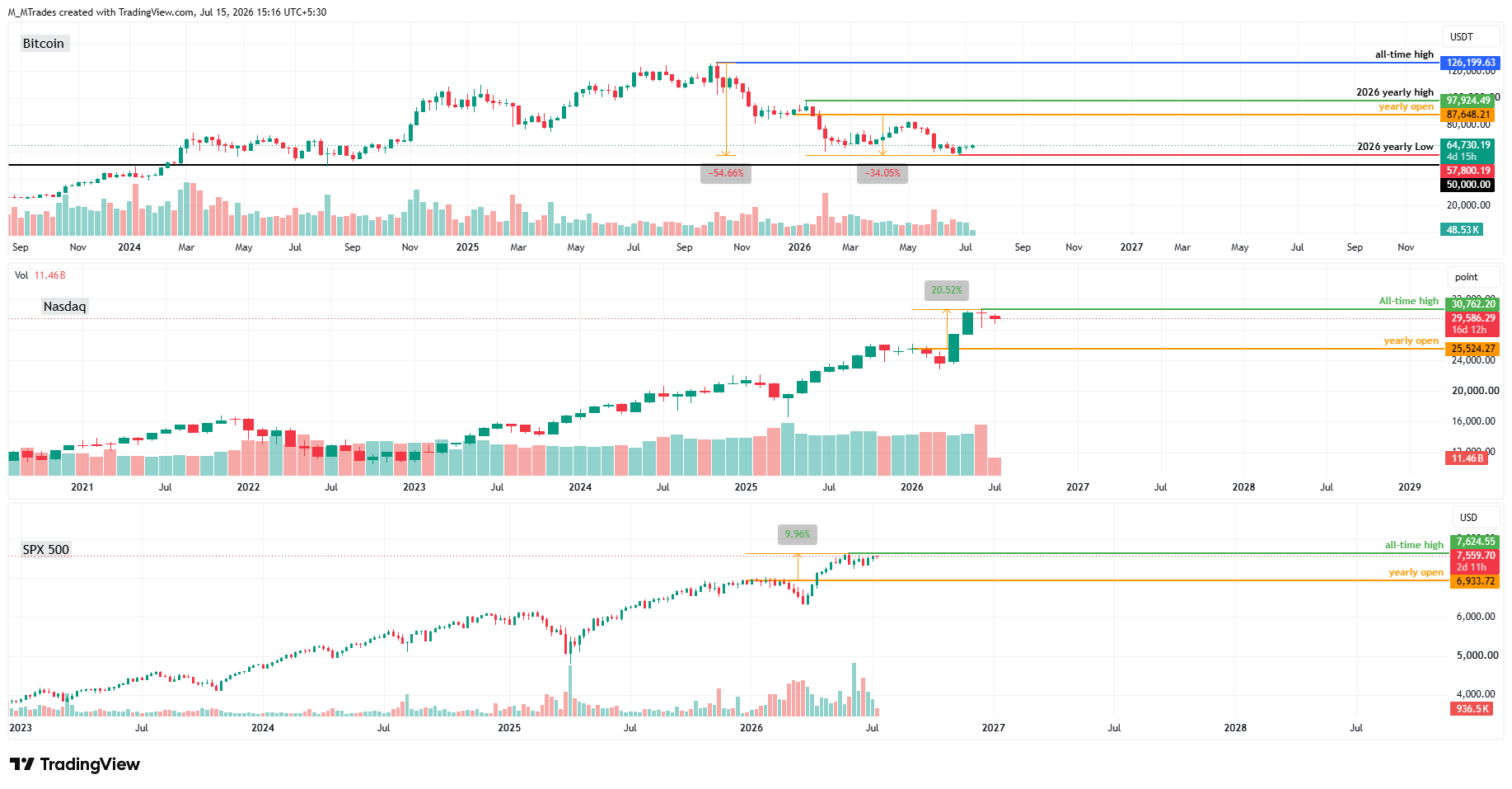

Bitcoin price touched a 2026 low on July 1 at $57,800, down from the yearly open of $87,648.

The largest cryptocurrency has extended its correction by over 54% from its all-time high of $126,199 seen on October 6, 2025.

As the Crypto King faced this steep fall, both the Nasdaq and the SPX 500 indices reached all-time highs, up 20.52% and 9.96%, respectively, reinforcing the view that the drawdown is Bitcoin-specific rather than a broad risk-off event.

Key factors that weighed on BTC

1. Regulatory momentum isn’t good enough

Bitcoin began the year on a negative note. The bullish narrative about crypto regulation that had been fueling the market since Donald Trump’s return to the White House took a step back as the CLARITY Act failed to advance out of markup, weighing on broader industry sentiment.

The setback highlighted ongoing friction between the crypto and banking sectors, particularly around the treatment of stablecoin rewards, which remains a key point of contention.

While legislation had some progress in the second quarter, the ultimate passage of the CLARITY Act is still very much up in the air. While the committee vote marked a measurable change versus the prior Q1 legislative setbacks, the bill remains highly uncertain because ethics-related objections emerged as a clear unresolved sticking point.

In addition, bank lobbying groups continue to oppose the bill because language regarding stablecoins paying yield is not sufficiently restrictive to prevent platform workarounds, which, in their view, could result in deposit flight from banks to digital dollars.

2. Institutional demand fades

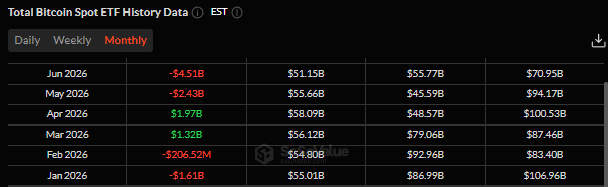

Institutional demand for Bitcoin, one of the main drivers of the 2025 rally toward all-time highs, weakened significantly during H1. SoSoValue data shows that US spot Bitcoin Exchange Traded Funds (ETFs) recorded $5.46 billion in net outflows during the first half of the year.

Inflows briefly returned in March and April, but heavy withdrawals resumed in May and June. These sustained ETF outflows highlight weakening institutional demand and were a key driver behind Bitcoin’s price correction.

3. Narrative headwinds: AI concerns and quantum computing risks

Concerns around Artificial Intelligence (AI) and Quantum Computing (QC) narratives have weighed on BTC traders’ sentiment.

Capital from the crypto market has started rotating into more AI-narrative stocks, as traders find greater appeal and opportunity in investing in such stocks rather than crypto. This could be seen in the KOSPI index, which surged to a new all-time high in June, with returns exceeding 100%.

Capital rotation further intensified ahead of blockbuster Initial Public Offerings (IPOs) such as SpaceX, Anthropic and OpenAI. This shift in investor capital has weighed on the broader downtrend in BTC.

On Quantum Computing, the recent progress shown by the Google research paper has highlighted the accelerating pace of development in quantum capabilities.

This quantum risk became more visible after US President Donald Trump signed two executive orders in June to advance US quantum research and development, raising institutional attention on a long-dated threat to public-key cryptography.

However, the near-term risk to BTC remains limited; traders and investors remain more cautious, as this is a protocol-level concern that may affect long-dated protocol threats, social and governance challenges for upgrades.

4. Shift in Digital Asset Treasuries behavior

The Digital Asset Treasury (DAT) companies, which were the key drivers for Bitcoin demand through aggressive accumulation in 2025, have changed their role this year.

Several treasury companies became sellers or potential sellers in H1, which added pressure on BTC prices. Miners also added to market supply by selling BTC to fund operations and increasingly finance investments in AI and high-performance computing.

This structural shift was further amplified when Strategy (MSTR), the largest corporate Bitcoin holder, announced the sale of 3,588 BTC from its BTC holdings to fund dividends on its Digital Credit. Since DATs had been a key source of marginal demand in previous years, their transition from consistent buyers to potential suppliers introduced a new structural source of sell-side pressure for Bitcoin.

5. Inflationary pressure kept BTC under pressure

The US-Iran war, which began in February and intensified further in July, has kept investor sentiment capped. Due to this ongoing war, Oil shipping routes have been disrupted, leading to constrained global supply.

A steady, prolonged rally in Oil prices during the first half of this year has added pressure on global inflation, as higher energy costs ripple through transportation and production, raising the costs of goods and services for consumers. This occurs at a time when many central banks around the world are still grappling with inflation that is above target.

This scenario has not only ruled out further interest rate cuts by, let’s say, the Fed or the ECB, but has even put on the table the possibility of tightening policy.

BTC and the broader crypto market generally struggle in high-interest-rate environments because high borrowing costs reduce market liquidity and steer markets towards safer, yield-bearing assets.

What’s there for BTC in the second half?

Several key catalysts are likely to shape Bitcoin’s next directional move in the second half of the year, with regulation, institutional demand, Digital Asset Treasury (DAT) activity, and macroeconomic developments remaining at the forefront.

1. The Clarity Act

The CLARITY Act stands as the most important industry catalyst for the digital asset sector. The bill would establish a federal market-structure framework covering exchanges, stablecoins, tokenization, custody, Decentralized Finance (DeFi), and potential future non-Bitcoin ETFs.

After advancing out of the Senate Banking Committee, it now faces a critical but narrow window on the Senate floor from July 13 to August 7, before recess and amid intensifying midterm politics.

The direct effect of the CLARITY Act on Bitcoin would be modest compared with that on altcoins and crypto equities. However, its successful passage would boost institutional confidence and expand adoption, supporting the broader crypto market. Conversely, failure to advance the legislation would leave the industry reliant on temporary agency guidance and vulnerable to shifting administrations.

2. Demand via ETFs

The second thing that traders should keep a watch on is that demand confirmation through flows will be essential for any sustainable recovery after the weak first half. US spot Bitcoin ETFs experienced significant net outflows, while stablecoin market capitalization contracted, signaling that marginal capital has been exiting rather than entering the ecosystem.

For Bitcoin to stage a sustainable recovery, ETF inflows must return alongside renewed stablecoin supply growth. Any price rebound lacking these underlying flow improvements would likely be a short-term bounce within a broader downward trend, indicating repositioning rather than fresh capital addition.

3. The DATs

Another major development to monitor is the evolving role of Digital Asset Treasury companies, namely Strategy. Once viewed as a reliable source of Bitcoin demand through continuous accumulation, Strategy has introduced the possibility of monetizing part of its Bitcoin holdings to meet financing and balance-sheet obligations.

Actual BTC sales remain limited for now, but the shift has altered market perceptions, raising concerns that DAT companies could gradually transition from consistent buyers to periodic sellers.

If financial constraints worsen due to wider discounts to net asset value (NAV) or elevated financing costs, these companies could become persistent sellers and increase market supply, thereby weighing on BTC prices. As of now, Strategy continues to trade at a slight premium to the value of its Bitcoin holdings, suggesting investors have not yet lost confidence in the DAT model.

4. Central banks

The macroeconomic side remains an important driver of Bitcoin, as it affects its liquidity and could bring high volatility to risk assets.

With the renewed escalation in geopolitical tensions between the US and Iran, energy prices could push higher, reinforce inflationary pressures, and keep interest rates elevated for longer. Such an environment dampens demand for risk assets.

Overall, while downside risks remain elevated, the second half of the year could mark a turning point if regulatory clarity improves through the CLARITY Act, institutional capital returns via ETF inflows and stablecoin growth, and macroeconomic conditions become more supportive. These factors will likely determine whether Bitcoin establishes a durable recovery or remains under pressure through the end of the year.

Bitcoin, altcoins, stablecoins FAQs

Bitcoin is the largest cryptocurrency by market capitalization, a virtual currency designed to serve as money. This form of payment cannot be controlled by any one person, group, or entity, which eliminates the need for third-party participation during financial transactions.

Altcoins are any cryptocurrency apart from Bitcoin, but some also regard Ethereum as a non-altcoin because it is from these two cryptocurrencies that forking happens. If this is true, then Litecoin is the first altcoin, forked from the Bitcoin protocol and, therefore, an “improved” version of it.

Stablecoins are cryptocurrencies designed to have a stable price, with their value backed by a reserve of the asset it represents. To achieve this, the value of any one stablecoin is pegged to a commodity or financial instrument, such as the US Dollar (USD), with its supply regulated by an algorithm or demand. The main goal of stablecoins is to provide an on/off-ramp for investors willing to trade and invest in cryptocurrencies. Stablecoins also allow investors to store value since cryptocurrencies, in general, are subject to volatility.

Bitcoin dominance is the ratio of Bitcoin's market capitalization to the total market capitalization of all cryptocurrencies combined. It provides a clear picture of Bitcoin’s interest among investors. A high BTC dominance typically happens before and during a bull run, in which investors resort to investing in relatively stable and high market capitalization cryptocurrency like Bitcoin. A drop in BTC dominance usually means that investors are moving their capital and/or profits to altcoins in a quest for higher returns, which usually triggers an explosion of altcoin rallies.

Recommended Articles