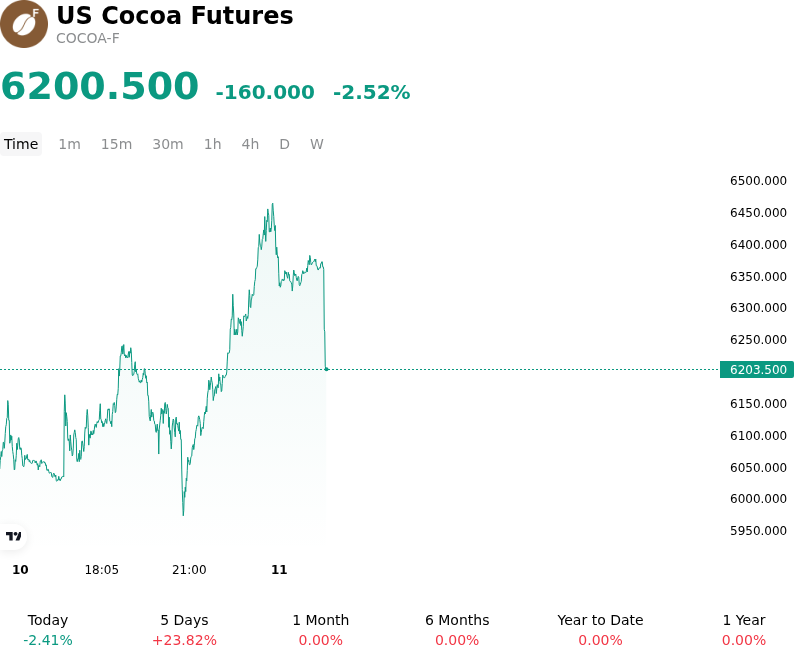

US Cocoa Futures (COCOA-F) Volatility Intensified on Jul 10: What to Watch

US Cocoa Futures (COCOA-F) is down 2.52% at Jul 10 04:55(ET), now at $6200.5, with a 7-day up of 23.68%.

What is driving US Cocoa Futures (COCOA-F)’s stock price down today?

The downward pressure on cocoa futures is primarily driven by an improving supply outlook for the upcoming 2026/27 main crop in West Africa. Favorable meteorological reports from Côte d’Ivoire and Ghana indicate that recent rainfall patterns have been optimal for pod development, easing long-standing concerns over the structural supply deficits that have characterized the market over the previous two years. As the region enters a critical developmental phase for the next harvest, the transition toward more conducive growing conditions is prompting institutional desks to recalibrate production estimates upward, effectively reducing the risk premium associated with tight global stocks.

On the demand side, evidence of sustained price rationing is becoming increasingly visible. Preliminary industrial data for the second quarter suggests that global cocoa grinds are continuing to contract as chocolate manufacturers face the limits of their ability to pass through record-high input costs to consumers. This trend toward demand destruction, particularly in mature markets like Europe and North America, is signaling to investors that the peak in consumption growth may have passed for the current cycle. The resulting accumulation of mid-crop inventories at origin ports has further mitigated immediate tightness in the physical market, encouraging commercial participants to reduce long-side hedges.

Market technicals and institutional capital flows have exacerbated the intraday move. After failing to clear key resistance levels earlier in the week, the market triggered a series of stop-loss orders from trend-following funds. In an environment where open interest remains relatively thin compared to historical norms, these liquidations have had a disproportionate impact on price action. The lack of fresh bullish catalysts ahead of the weekend has left the market susceptible to profit-taking and technical de-risking by macro funds.

Furthermore, investors are monitoring the broader impact of the US dollar's performance and its influence on soft commodity pricing. While supply-demand fundamentals remain the primary driver, the absence of significant geopolitical disruptions or transport bottlenecks has allowed the market to focus squarely on the improving fundamental balance. As the implementation of the EU Deforestation Regulation continues to influence trade flows, the market appears to be shifting its focus from immediate scarcity to a more balanced medium-term outlook, characterized by recovering West African yields and stabilizing global inventories.

More details about US Cocoa Futures (COCOA-F)

Recent Events and Risks:

- Improved Precipitation in West Africa: Recent meteorological reports from Ivory Coast and Ghana indicate an increase in seasonal rainfall over key cocoa-growing belts, potentially alleviating multi-month soil moisture deficits and improving the outlook for the 2024/25 main crop, which pressures the scarcity-driven price premium.

- Contraction in Global Grinding Data: Recent quarterly figures from major processing hubs in Europe and North America reveal a year-on-year decline in cocoa grindings, signaling that record-high terminal prices are causing significant demand destruction and prompting chocolate manufacturers to reformulate products with cheaper substitutes.

- Margin-Induced Liquidation Risk: Heightened intraday volatility has sustained elevated margin requirements on ICE futures, creating a liquidity-thin environment where technical breaks below psychological support levels can trigger forced liquidation of crowded speculative long positions.

- Regulatory Compliance Delays: Emerging discussions regarding a potential one-year delay or phased implementation of the EU Deforestation Regulation (EUDR) threaten to remove the immediate "scramble for certified supply" premium, which has been a primary driver of recent spot market tightness.

Recommended Articles