Lam Research Corp Stock (LRCX) Moved Up by 4.98% on Jun 30: What Signal Does It Send?

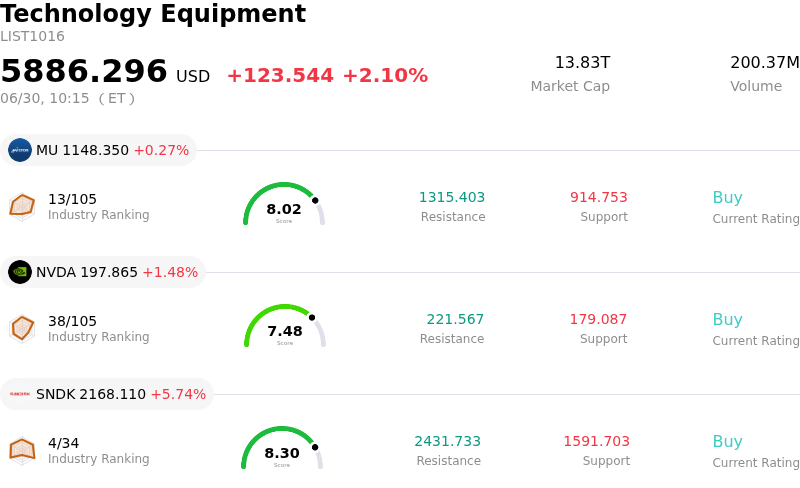

Lam Research Corp (LRCX) moved up by 4.98%. The Technology Equipment sector is up by 2.10%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.27%; NVIDIA Corp (NVDA) up 1.48%; SanDisk Corporation (SNDK) up 5.51%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research Corporation has experienced robust upward momentum, fueled by a combination of high-profile Wall Street analyst upgrades, structural tailwinds in the semiconductor equipment industry, and a key index inclusion. This strong performance has offset broader market volatility and previous concerns regarding cyclical cooling, highlighting the company’s crucial role in the ongoing global build-out of artificial intelligence infrastructure.

A primary catalyst for the positive movement is a wave of optimistic revisions from institutional analysts. Cantor Fitzgerald raised its price target for Lam Research to five hundred dollars, maintaining an Overweight rating and emphasizing the company's market share gains among semiconductor capital equipment manufacturers. Simultaneously, Susquehanna upgraded its target to four hundred seventy-five dollars from three hundred eighty-five dollars, pointing to extensive channel checks that reveal an upward revision to semiconductor equipment backlogs extending beyond one year. Industry-wide wafer fabrication equipment spending forecasts have also been elevated, with projections now targeting up to three hundred billion dollars by 2028 as key customers pay premium rates to secure tool allocations.

Beyond direct analyst sentiment, the company's growth trajectory is heavily supported by the structural demands of the AI hardware revolution. Advanced memory technologies like High Bandwidth Memory and next-generation 3D NAND rely heavily on Lam’s specialized atomic layer deposition and high-aspect-ratio etching equipment. Management has projected that advanced packaging revenue alone will grow by more than fifty percent in 2026, driven by these complex chip architectures. This outlook is reinforced by the broader industry data from SEMI, which recently reported that worldwide memory equipment spending is projected to surpass fifty billion dollars for the first time in 2026 due to robust demand for AI accelerators and GPU infrastructure.

Further driving institutional demand, Lam Research was added to the prestigious Russell Top 50 Index in late June. This inclusion has triggered automatic portfolio adjustments and forced buying by passive index funds and exchange-traded funds. While concerns about premium valuation and general semiconductor cyclicality remain, the confluence of index-driven buying, substantial upgrades to industry spending forecasts, and Lam's dominant market position in critical fabrication technologies have collectively propelled the stock's recent gains.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 3.036, indicating a buy signal. The RSI at 63.679 suggests neutral condition and the Williams %R at 3.735 suggests overbought condition. Please monitor closely.

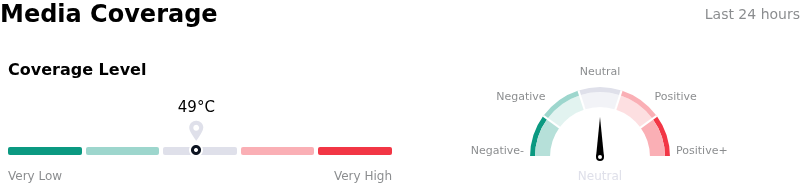

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

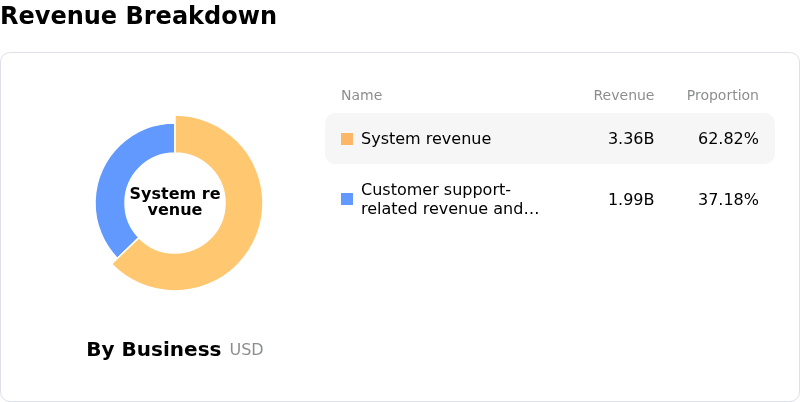

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $343.42, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Downstream Capital Allocation Shifts (SK Hynix): Following SK Hynix's structural pivot to slow advanced High-Bandwidth Memory (HBM4) and advanced NAND production in favor of commodity DRAM, Lam Research faces near-term order compression. Commodity semiconductor manufacturing requires significantly fewer processing steps, which directly reduces the etching and deposition tool intensity per wafer and weakens the revenue potential of Lam’s advanced systems.

- Severe System Shipment Growth Deceleration: Driven by cyclical cooling in 3D NAND and mature-logic nodes, institutional analysts project Lam's system shipment growth to sharply decelerate to just 3% in 2026, down from 82% in 2025. This structural slowdown is actively compounded by falling customer down payments, indicating a near-term cooling of capital commitments.

- Geopolitical Exposure and High China Revenue Concentration: Lam Research remains highly vulnerable to expanding US export control regulations due to its substantial 34% to 35% revenue concentration in China. This heavy geographical exposure elevates the risk of sudden revenue disruptions as trade restrictions limit advanced wafer-fabrication equipment sales to Chinese fabs.

- Extreme Valuation Premium and Material Insider Liquidations: Trading at an elevated trailing P/E ratio exceeding 69x (well above its historical 5-year median), the stock has shown extreme vulnerability to multiple compression during sector pullbacks. This valuation risk is heightened by SEC Form 4 filings showing zero insider buying alongside significant executive liquidations, including a $19.1 million divestment by Director Eric Brandt and a position reduction by SVP Neil J. Fernandes.

Recommended Articles