- Gold tumbles as traders book profits ahead of key US inflation data

- Australian Dollar remains stronger following PBoC interest rate decision

- Gold declines as traders brace for trade talks, US CPI inflation data

- Gold tumbles as traders book profits ahead of key US inflation data

- BNB Price Rebounds as Traders React to CZ’s Pardon — But One Roadblock Remains

- US CPI headline inflation set to rise 3.1% YoY in September

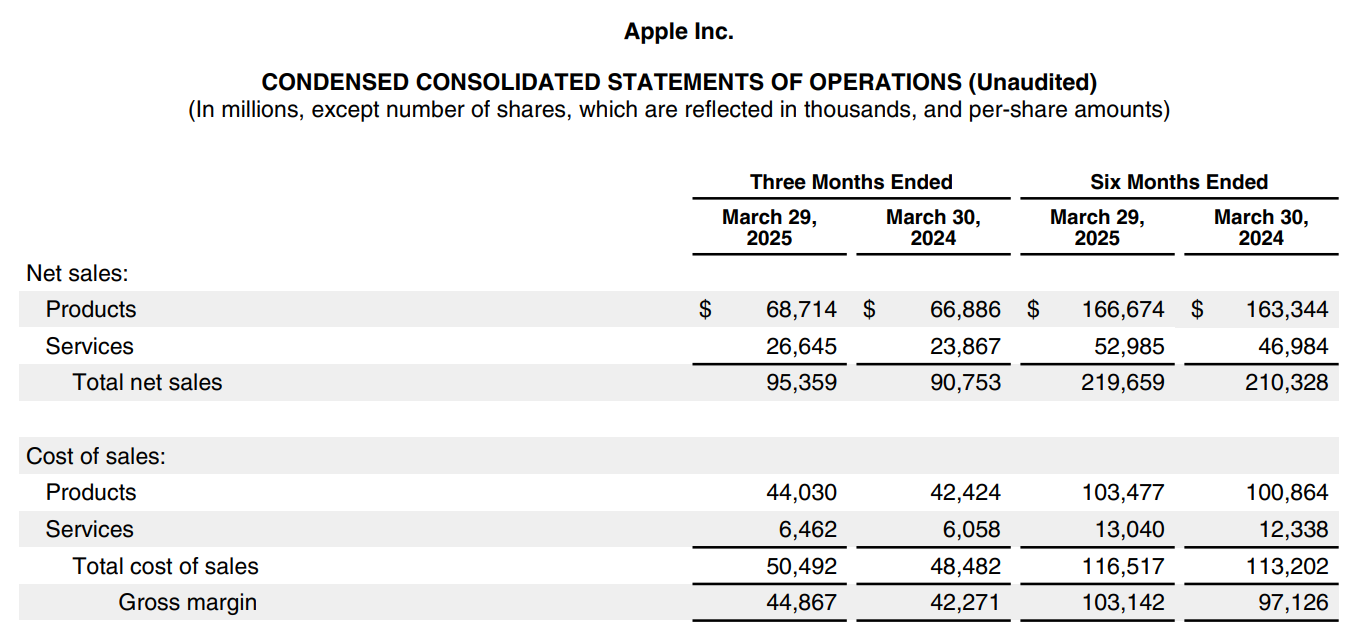

Apple reported Q2 FY25 revenue of $95.4 billion and net income of $24.8 billion, with Services contributing 28% of total sales and 45% of gross profit—showcasing its margin supremacy.

Gross margin reached 47.1%, up 50bps YoY, driven by Services' 75.7% margin; hardware margins trailed at 35.9%, highlighting Apple’s strategic pivot toward digital monetization.

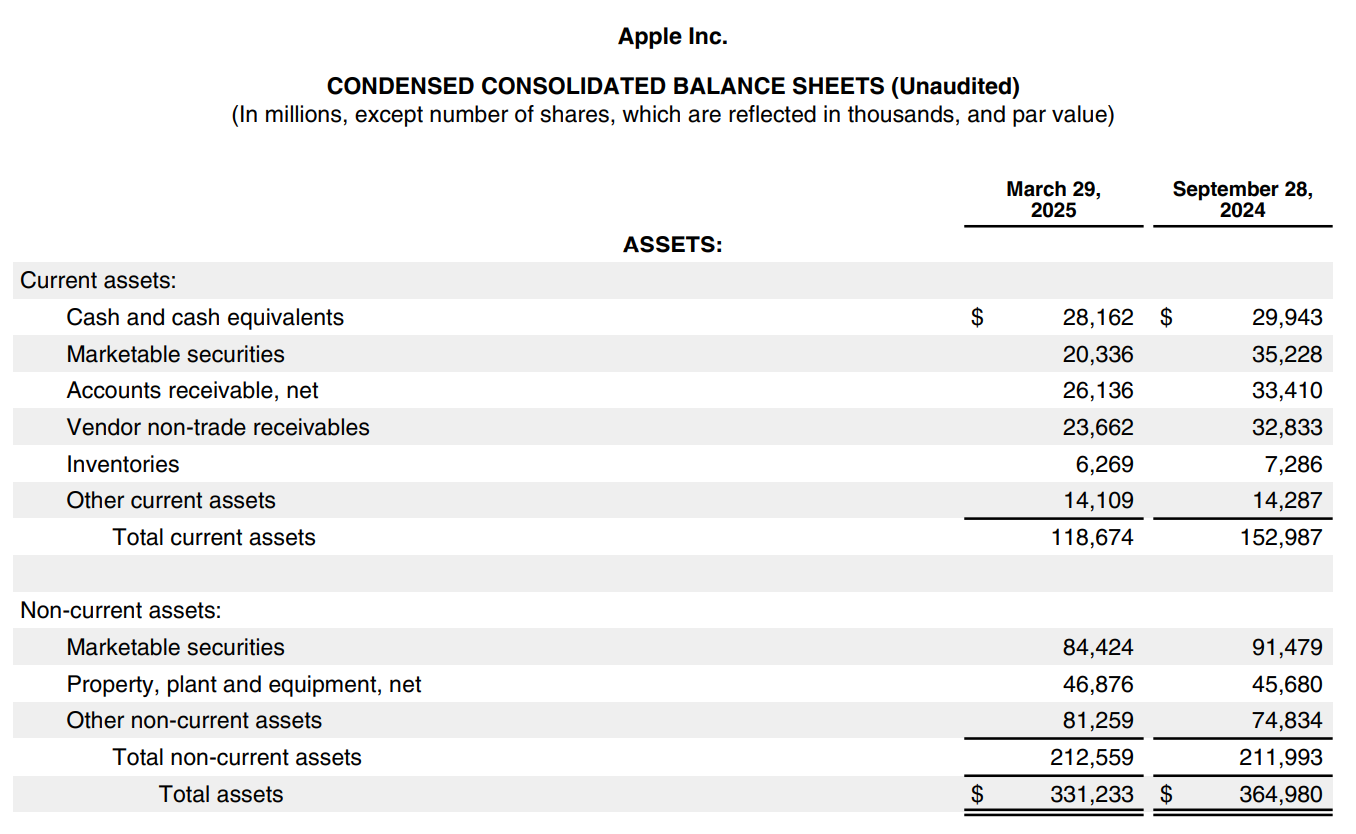

Apple spent $49.5 billion on buybacks and $7.6 billion on dividends YTD, while maintaining a cash position of $28.2 billion and $84.4 billion in long-term securities.

R&D spending hit a record $8.6 billion (9% of sales), signaling Apple’s quiet but focused AI push, while its valuation stands at 27.25x forward P/E with a PEG of 2.48.

TradingKey - Apple (AAPL) has long excelled at the nexus of hardware greatness, software integration, and brand affection. But Q2 FY25 presents a picture of a grownup goliath honing its operating playbook while building the foundation for future expansion outside of devices. Apple is still an earnings machine with revenue of $95.4 billion and net income of $24.8 billion. But beneath the surface, strategic nudges quietly suggest a broader story taking shape, one of Apple evolving from a product icon to an ecosystem giant with widening digital moats.

Fundamental to its success is a quarter that highlights Apple’s long-term strength amid a world of fickle consumer behavior and international regulatory pressures. Services, which comprise more than 28% of revenue, are stabilizing margins and scale of recurring revenue at their back. But that is also a defensive strategy amid cyclic device saturation and geopolitical risks, particularly in Greater China. As Apple contends with macro headwinds and trade dynamics, its success at compounding value from AI integration, expense management, and customer retention will shape its next chapter.

Source: 10-Q

Apple's Core Flywheel: How Services Alleviate Hardware Cyclicality

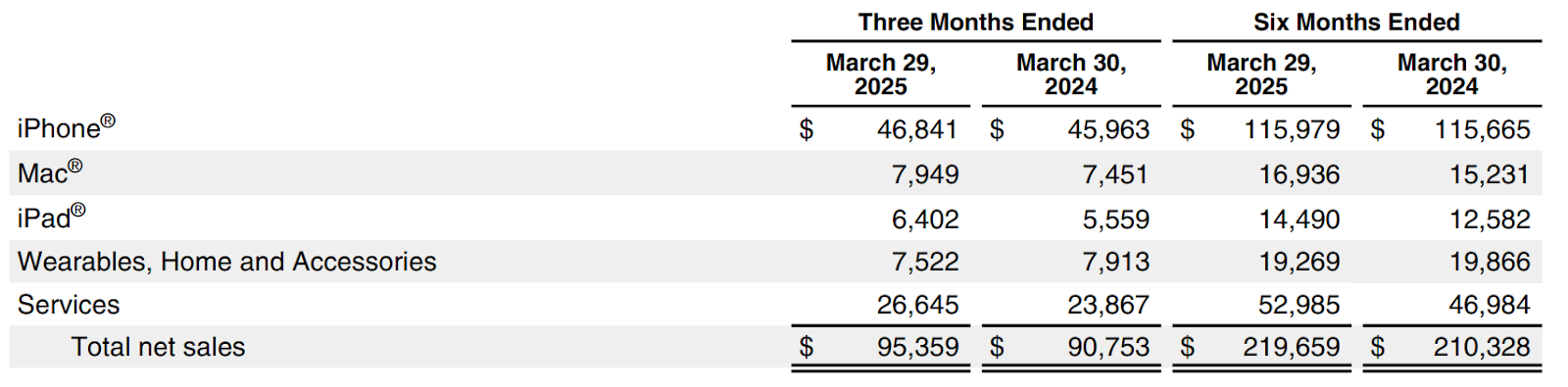

Its Apple ecosystem is its biggest strength, where each piece of hardware adds greater lock-in for the customer, and each service tier doubles monetization opportunities. Product revenue rose 2.7% year on year to $68.7 billion in Q2 FY25, with strong demand for iPhone Pro and a resumption of iPad sales (+15% year over year). Of particular note, Mac sales rose 7%, with the upgraded M-series silicon and revived institutional adoption. Wearables fell 5% year on year, however, that weakness was muted by explosive growth for Wearable revenue, which rose 12% year on year to $26.6 billion.

Not just breadth that makes Apple’s business model so resilient, but vertical alignment. From Apple Silicon design to services delivery (App Store, iCloud, Music, TV+), Apple controls and orchestrates nearly its entire value chain. That control insulates margins even with input costs' volatility and FX headwinds. Gross margin reached 47.1%, a 50bps increase from the prior year, driven by Services' 75.7% margin profile, a dramatic contrast with hardware at 35.9%. That shift toward digital monetization is deliberate and ever more necessary in a flatlining world smartphone market.

In the background, Apple is also accelerating its investments in AI. R&D reached a record-high $8.6 billion in Q2, just shy of 9% of sales, as Apple prepares its GenAI suite, possibly launching across iOS and macOS by FY26. Unlike cloud-centric competitors, Apple's competitive differentiator is on-device intelligence. With its own privacy-driven AI, it may quietly recast user experience without the regulator overhang that has weighed against other cloud-centric models.

Source: 10-Q

Getting a Measure of the Opposition: Margin Defense Meets Strategic Discipline

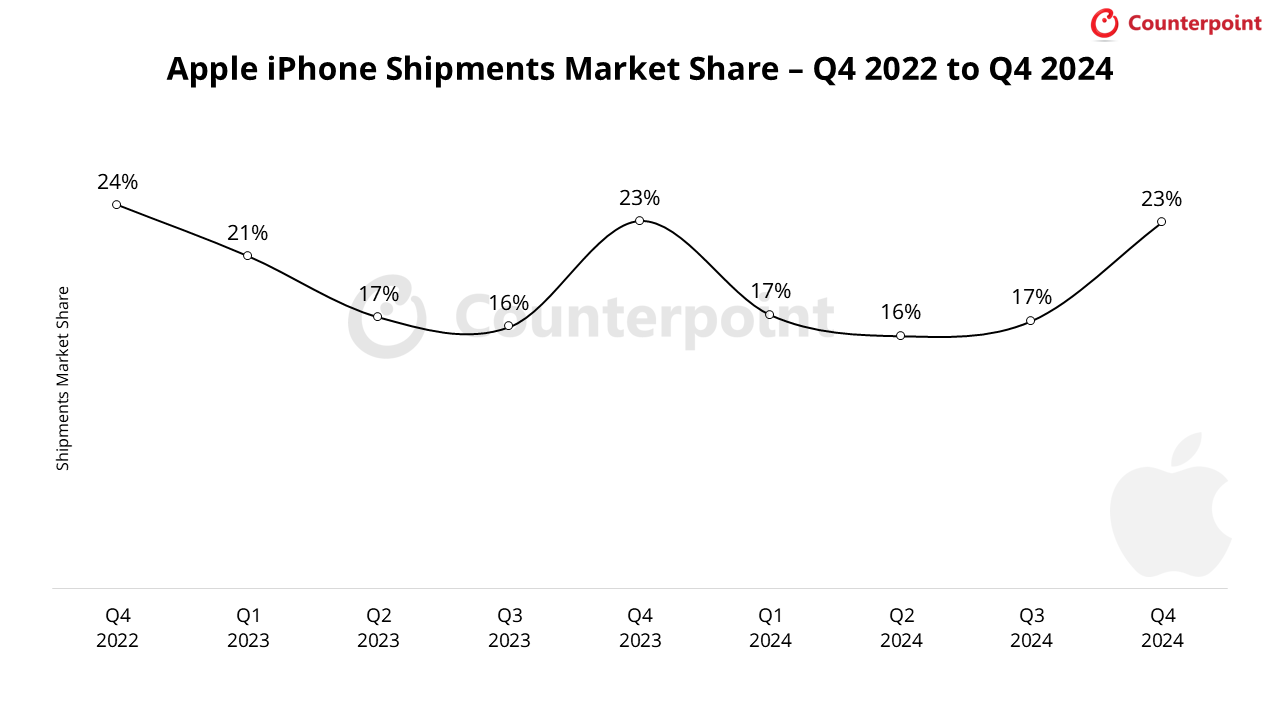

In spite of growing pressure from rival ecosystems such as Samsung, Google, and Microsoft, Apple’s differentiation holds firm. When competitors resort to price or scale in the cloud, Apple continues to triumph based on integration, design, and affinity with the user base. The premium benchmark is the iPhone, with Pro versions propelling ASP growth and carrier promotions propelling demand. More strategically speaking, Apple is not committing to price wars of a race to the bottom. Price inelasticity, particularly within developed markets, shields margins as well as brand equity.

In services, the moat is less impenetrable, though. Apple is facing mounting pressure on App Store economics and DMA compliance across Europe. Regulatory investigations into steering controls and pricing schemes pose the threat of jeopardizing 30% commission revenue streams, particularly for games and subscription apps. Apple’s Q2 move, stealthily opening doors for third-party app stores on a limited basis and allowing EU markets’ in-app link permissions, is a defensive adjustment. But the verdict remains out as to whether measures will sustain monetization leverage or stimulate platform challengers.

In AI adoption, Apple trails Microsoft or Alphabet in terms of narrative exposure. Yet its comparative quiet may be intentional. Rather than rushing to market with chatbot capabilities, Apple seems to be infusing AI incrementally, building out Siri, automating workflows, and natively personalizing services. This under-the-radar deployment is a function of both brand conservatism and technical differentiation: Apple’s AI is optimized for on-device, privacy-first inference rather than dependency on hyperscalers.

Source: Counterpoint Research

Delving into the Numbers: Growth, Efficiency, and Capital Allocation

Apple’s Q2 FY25 numbers are a story of unassuming strength. Revenue increased 5.1% year-over-year to $95.4 billion, led by the growth of Services and iPad. Net income came to $24.8 billion, equivalent to $1.65 EPS (level with last quarter, up 7.8% year-over-year). Operating margin stayed at a respectable 31%, backed by control on opex, R&D expanded only 8.2% year-over-year while SG&A expanded a modest 4%. Services now account for 28% of aggregate sales but an unbelievable 45% of gross profit, which underscores the importance of software margins to long-term value.

Apple’s cash war chest on the balance sheet is still strong, with $28.2 billion of cash and $84.4 billion of long-term marketable securities. Inventories and receivables did drop substantially, likely due to better control of the supply chain and working capital management. Accounts payable also decreased emphatically (-$14.8 billion YTD), possibly indicative of either better terms or seasonable normalization from post-holiday demand.

Shareholder returns are still aggressive. Apple spent $49.5 billion on share repurchases YTD and issued $7.6 billion of dividends, further decreasing diluted share count. Financial engineering, combined with growth in Services EBIT, drove EPS higher while topline growth trailed technology comps. Apple remains committed to capital returns as a pillar of shareholder value with an additional $100 billion of buyback authorization and a 7% increase in quarterly dividend to $0.26.

Source: 10-Q

Valuation: Justifiably Deep Premium Pricing, or Extended Stability?

Apple sits at a forward P/E of 27.25x (Non-GAAP) and 27.31x (GAAP) and is roughly 34% higher than its sector average on a non-GAAP basis and only a touch higher than its own recent five-year average of 28.69x. Even with what seems like a premium, Apple’s pricing is multi-faceted, less a hype bubble and rather a portrayal of structural quality, margins durability, and master capital allocation.

The actual rub is the market’s challenge to harmonize Apple’s modest topline expansion with its rich multiples. The PEG on a non-GAAP basis is 2.48, considerably higher than the sector average of 1.54, suggesting growth-normalized valuation is extended unless growth within Services or AI monetization makes a dramatic jump. But even that metric is at risk of oversimplification. Apple’s 20.90 EV/EBITDA forward multiple, while 59% higher than the sector average, is within its normalized five-year range (21.19). EV/EBIT at 22.60 also indicates that operating earnings are being valued with a substantial, but not exorbitant, quality premium.

One place where the valuation is extreme is on capital structure measures. Apple's Price/Book multiples, 43.89x trailing and 48.57x forward, are more than 1,200% higher than industry standards. This is not an outlier, but a characteristic of Apple’s capital-light, asset-leveraged business model. When there is intense share buyback and minimal tangible equity, book value is no longer a reliable surrogate for economic value. Investors are not purchasing Apple’s net assets, but rather its durability of sustaining cash generation and monetization of a billion-user platform.

Even EV/Sales measures (7.23x trailing, 7.12x forward) look lofty on initial inspection, some 3x the industry median. Once again, context is key: Services, with >75% margins, represent a material portion of revenue and are priced accordingly. Relative to enterprise software comps, Apple’s EV/Sales picture remains conservative considering optionality across wearables, health, and AI integration.

In the end, Apple’s value is less a matter of line-of-sight growth projections and rather one of platform depth of monetization. Its intrinsic value probably resides within a range of $185 to $210 a share, based on steady services margin growth, modest AI coattails, and sustained capital return momentum.

Source: SeekingAlpha

Risks: Regulation, China, and the AI Arms Race

Apple's risks are no small matter. Regulatory overhang within the EU and U.S. may reshape its monetization playbook for Services. The Digital Markets Act is a specific threat, aiming at Apple’s gatekeeper position, imposing compliance burdens and prospective revenue leak from competing app distribution. Another is China with Q2 sales falling by 2.3% YoY due to continued soft demand for iPhones and local competitive pressure from Huawei. Given China's 16% revenue contribution, sustained weakness may crimp near-term growth.

Also at risk is both supply chain continuity and geopolitical atmosphere toward Apple’s brand due to U.S.-China tech decoupling. Ultimately, Apple risks being left behind AI platform wars. Although its on-device, privacy-focused AI strategy matches its brand heritage, being without a marquee LLM or developers' ecosystem might bring strategic vulnerabilities. If consumer demand turns toward real-time generation capabilities, Apple might be forced to move faster on partnerships or acquisitions to remain competitive.

Source: Reuters

Conclusion:

Apple Isn’t Only a Tech Giant, But an Operations Masterclass Apple's Q2 FY25 performance cements its position as technology’s most disciplined operator. Headline growth may be modest, but the consistency of the company’s margins, capital efficiency, and services growth tells a compelling long-term story. As Apple sets out on its AI chapter, quietly but intentionally, the question is not so much whether it can grow, but how profitably it can expand its ecosystem.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.