2025 Mid-Year Review: The Reversal of the “End of U.S. Exceptionalism” — Strongest Bond Rally in 5 Years, New Equity Highs

TradingKey - In the first half of 2025, concerns over the end of U.S. exceptionalism dominated global investor sentiment, as Trump’s tariff policies triggered frequent sell-offs across stocks, bonds, and the dollar. However, by June, a shift was underway — with U.S. equities hitting record highs, and Treasuries staging their strongest rebound in years, reversing earlier pessimism.

Driven by improved expectations for Fed rate cuts and progress in trade negotiations, the U.S. capital markets have seen a significant turnaround since May — offering a fresh look at American assets after months of volatility.

Trump’s Tariff Policies Triggered “Sell America” Trend

In early 2025, Trump’s aggressive tariff hikes, the “Beautiful Big Bill”, and the controversial Section 899 asset tax prompted a wave of capital outflows toward non-dollar assets. At several points this year, the U.S. experienced rare episodes of stocks, bonds, and the dollar all falling together.

However, as H1 came to a close, the narrative began to change. While the U.S. Dollar Index (DXY) remains weak, both U.S. equities and Treasuries have made surprising recoveries.

On April 9, when Trump announced a temporary pause on reciprocal tariffs, the S&P 500 stood near its lows for the year. It has since rallied approximately 24%, reaching a new high of 6,173.07 on Friday, June 27.

U.S. Treasury Secretary Scott Bessent noted that the S&P 500 has staged its fastest recovery on record, quickly bouncing back from a 15% drawdown — and he expressed optimism that Trump’s tariff policy would not lead to economic recession.

Analysts suggest that the strong performance of U.S. equities reflects renewed confidence in the Fed’s accommodative stance and resilient corporate earnings — despite lingering risks such as trade tensions, fiscal deficits, and geopolitical uncertainty.

“Sell America, Buy Europe” Trade Loses Momentum

The earlier trend of shifting capital from U.S. to European assets also appears to be fading.

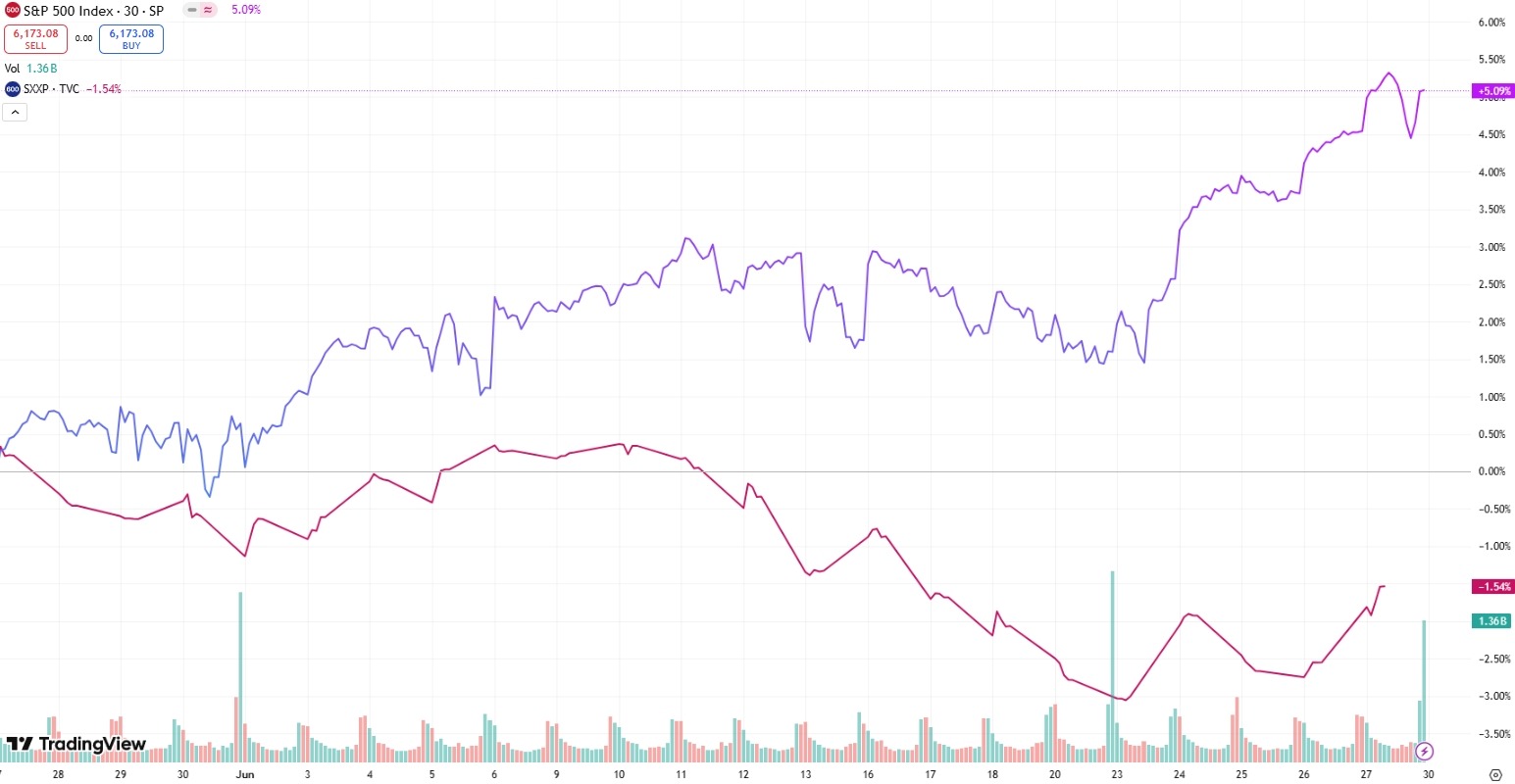

The S&P 500 rose nearly 10% in Q2, outperforming the Stoxx 600’s sub-2% gain — and beating most major global indices.

One-Month Performance of S&P 500 vs. Stoxx 600, Source: TradingView

While the S&P 500 still trails the Stoxx 600 on a year-to-date basis — up 5% vs. 7% — analysts believe the gap may narrow further. They argue that U.S. market strength is underpinned by solid balance sheets and earnings growth, while European gains appear more speculative — hinging largely on defense spending plans yet to materialize.

U.S. Treasuries Stage a Historic Comeback

Meanwhile, investor attention has shifted to the potential for two interest rate cuts by the Federal Reserve later this year.

The yield on the 10-year Treasury has declined by more than 30 basis points year-to-date, with a 15-basis point drop alone in June.

If this momentum continues, U.S. Treasuries are on track to deliver their strongest six-month performance since 2020, marking a dramatic reversal from earlier fears of bond market instability.

Recommended Articles