Nvidia: What to Expect from Q1 Earnings? Will Investors be Disappointed Again?

.jpg)

Source: TradingView

TradingKey - The highly-expected Nvidia earnings for the first quarter of the new fiscal year will be announced on Wednesday (28th of May) after the bell. In the past several quarters, the company managed to beat the estimates on both the top and bottom lines, however the subsequent reaction of the investors were either lukewarm or even negative, implying the enormous amount of expectations the market is putting on the GPU giant.

Revenue and EPS

The revenue is expected to be $43.38 billion (+66% year-over-year), while earnings per share to be 74 cents (+21% year-over-year). The EPS growth will be significantly lower compared with previous periods due to the China H20 ban. It was announced that there will be a one-off charge of around $5.5 billion related to inventories and purchase commits.

In fact, the ban will be a $10-15 billion headwind to the revenue throughout the whole fiscal year. We do expect the management to disclose more details on this topic and provide up-to-date guidance for revenue and earnings.

Margins

In the last four quarters we saw a sequential decline in gross margins, from 78.35% in 2025Q1 to 73.03% in 2025Q4, raising concerns about eroding competitive moat. Gross margin pressure will continue through the first half of the fiscal year but we do expect a mean reversion in the later half to mid-70%s once the new Blackwell products are fully rolled out and all supply chain delays and manufacturing issues are sorted out.

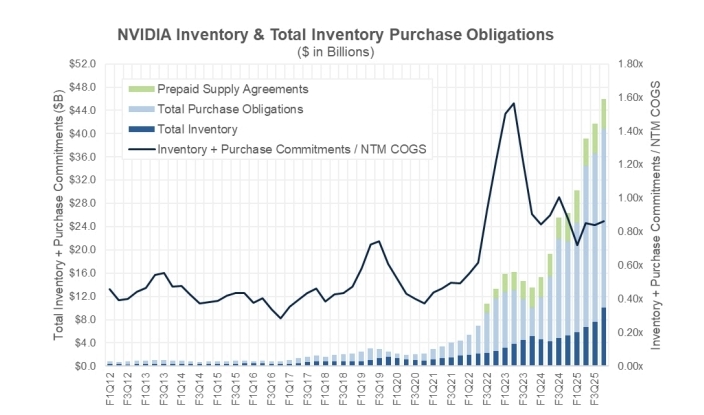

Source: Wells Fargo Securities

Another important aspect for the margins is the state of the inventory. Currently, the inventory along with the purchase obligations and the supply agreements as a proportion of COGS are not at a very high level, far below what it was during the supply chain crisis in 2022. This decreases the chance of product markdown and therefore pressuring the margins.

Spending on AI Infrastructure

One of the biggest concerns of investors with regards to Nvidia is about AI spending by hyperscalers, and whether we will see slowdown due to economic downturn or unsatisfactory ROI.

The top four cloud service providers have combined capital-spending plans this year that exceed $318 billion, up about 19% year to date. From recent earnings calls from Amazon, Microsoft, Google and Meta, we saw slight upwards revisions in capex estimates for the current year, which should provide a temporary relief for NVDA bulls. AI remains central to growth strategies, with spending tied to commercial models like Copilot, Llama and Gemini.

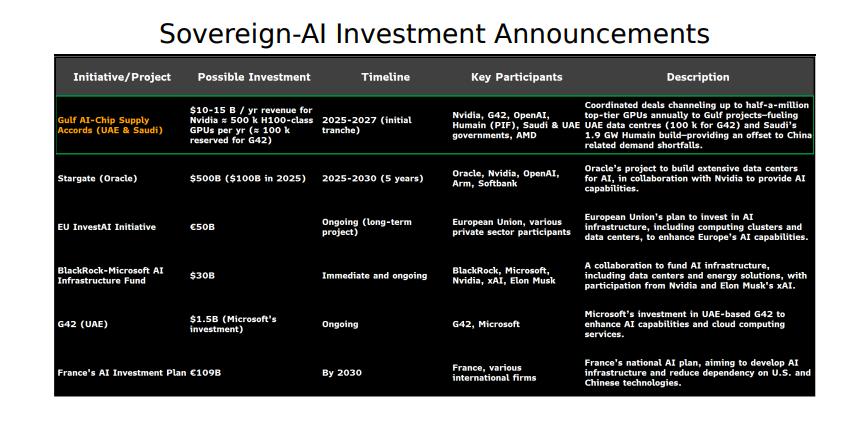

A trend that may soon emerge is AI spending on a government level. Many countries, from America, to Europe and the Middle East, are shifting their priority towards developing strong AI capabilities, which might happen to be a big tailwind for Nvidia revenue, considering its dominant market position. UAE and Saudi Arabia are committing tens of billions of dollars toward national AI infrastructure. This coincides with the US-led Stargate project, as well as the recent efforts of Europe to catch up technologically with the US and China.

Source: Bloomberg Intelligence

Finally, TSMC High Performance Computing (HPC), as well as SK Hynix and Micron High Bandwidth Memory (HBM) businesses are still growing rapidly. TSMC HPC grew 70% in 2025Q1 and we expect solid growth for HBM once they report it. Usually these products are also closely tied with data centers and AI infrastructure, making them strongly correlated with Nvidia performance and a good predictor of the company’s Data Center segment growth.

Valuation

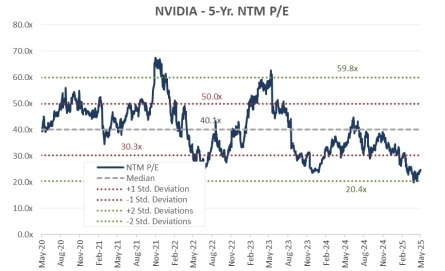

Nvidia's valuation can be seen from two perspectives - one is from historical average P/E and the other is compared to the Philadelphia Semiconductor Index (SOX) covering the whole industry.

Currently, NVDA is traded at 24x the estimated forward earnings, which is on the lower side versus the historical average. The five-year average is around 32x.

Source: FactSet

Also, as a market leader, Nvidia is usually traded at a large premium versus the SOX. However the current premium is just 20% which is much lower than the five year average of 76%. Considering that Nvidia produce the best performing product, and possesses a software-led economic moat (CUDA), they deserve a much larger premium against the rest of the semiconductor players.

Source: Bloomberg Intelligence

Recommended Articles