Berkshire’s Pause: Strategy, Not Stagnation

- Berkshire’s $347B cash position isn’t idle; it’s a strategic reserve ready to deploy during market turmoil, over 66% of current market cap is liquid, yielding powerful downside convexity.

- Insurance float hit $165B in Q1 2025, with $2.6B in underwriting profit, GEICO’s AI-led turnaround and Jain’s actuarial upgrades mark a durable shift in operational strength.

- Berkshire’s forward P/E is 128% above sector median, but EV/EBITDA at 7.64x is 32% below peers, market undervalues its capital optionality and counter-cyclicality.

- Japanese trading house holdings exceed $20B, with Buffett aiming for 50+ year duration; Berkshire seeks to lift the 10% cap, signaling sovereign-scale, global capital strategy.

TradingKey - The market tends to read inertia as stagnation. Berkshire Hathaway's (BRK.A) (BRK.B) own $347 billion cash hoard has caused renewed suspicion of capital deployment, as skeptics cite lagging returns and soaring cash ratios. Q1 2025 results, when viewed together with strategic commentary by the AGM and underlying valuation scatterplots, show a firm far from stasis but strategic pause, poised to deploy capital when the wider market falters. Berkshire, in such a case, shouldn’t be viewed as a firm holding out to seize the next opening; it needs to be re-priced as a platform with embedded convexity, optionality, and policy-insulated defensive strengths.

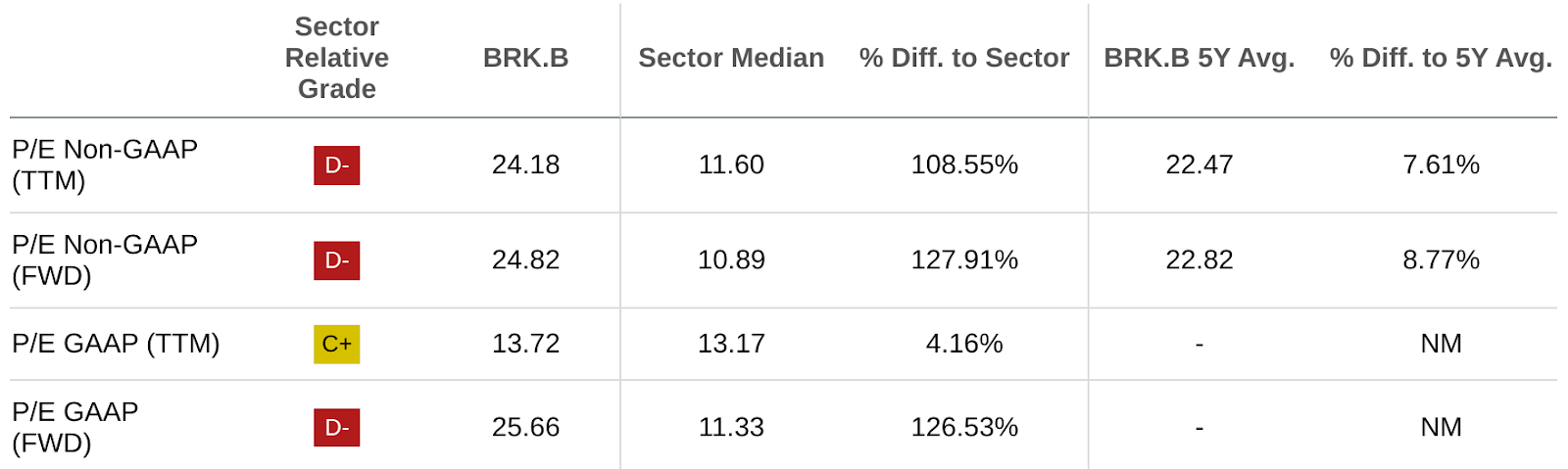

The prevailing assumption that Berkshire exchanges at a premium to peers in the sector on a trailing P/E basis overlooks the broader structural inflection: Berkshire is not merely managing earnings; it's managing markets to manage volatility and duration and the ability to underwrite markets themselves. A superficial glance at its 24.18x non-GAAP TTM P/E (against a sector median of 11.6) might imply it's overvalued, but when the counter-cyclicality of its insurance float and latent purchasing power are considered, as are its tested acquisition DNA, the story turns. The better lens is to look at Berkshire as a capital efficiency and reinvestment optionality story, one in which the market is only just beginning to price.

.png)

Source: Voronoi

Insurance, Infrastructure, and Infinite Time Horizon: Unpacking the Berkshire Moat

Berkshire Hathaway is not a conventional conglomerate. It’s an industrial fortress combined with a built-in hedge fund and a reinsurance engine. This design is not just a Warren Buffett legacy. It’s now an institutional asset class on its own. Berkshire’s decentralized form has more than 90 operating businesses and is deceptively adaptable. Greg Abel’s expanding leadership visibility seen during the AGM attests to a smooth succession process in the course, with Berkshire’s holdings such as BNSF, Berkshire Hathaway Energy, and GEICO more and more connected to self-driving compound expansion.

At the center of Berkshire’s model is its insurance flywheel, which keeps generating float, now over $165 billion, that Buffett and Jain are able to redeploy without dilution. The capital is completely free and never has to be repaid. Underwriting profit from insurance operations in Q1 2025 was more than $2.6 billion, highlighting how GEICO’s turnaround is more than skin-deep. Berkshire’s insurance operations have moved on from simple premium collection to AI-enhanced actuarial modeling, a shift Jain recognized at the AGM. Although Berkshire is coming late to heavy AI investment, the conservative wait-and-pounce stance has traditionally returned better marginal returns.

Complementing it is Berkshire Hathaway Energy, a utility giant regulated by government agencies and now with ~$30 billion in annual revenue. Abel's long-time steward expands its renewable and transmission presence, a differentiator in the midst of US energy grid decentralization. Long-duration assets are delivering stable, regulated returns as a result. Traditional models and their sum-of-parts estimates fail to capture the value of BHE. But as the US electrifies and data center infrastructure accelerates with AI, BHE's moat will grow, and it will gain from capital markets turmoil instead of losing out to it.

In contrast, BNSF, while subject to secular rail headwinds, is a cash-generating asset at scale. BNSF has geographic insulation relative to peers such as Union Pacific or CSX, which are subject to more pronounced operational leverage. While it experienced some margin contraction in 2024, BNSF is structurally better positioned to move energy, agricultural, and bulk commodities through the Midwest and West Coast.

.png)

Source: Berkshire Hathaway Energy Deck

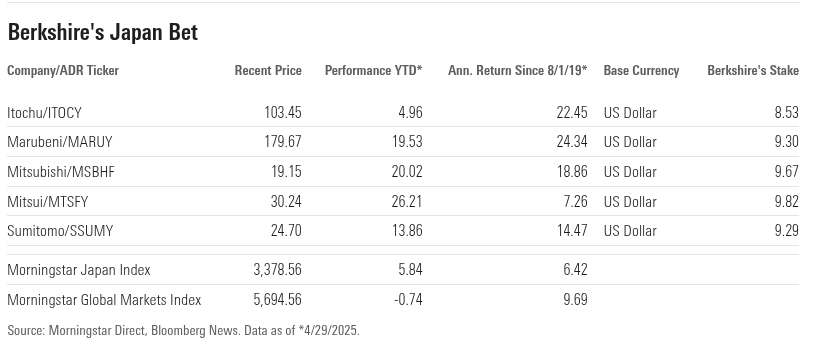

Japan and the Unassuming Emergence of Worldwide Deep Conviction

Investments in Berkshire’s Japanese trading houses, Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo, were initially written off as opportunistic value plays. But with Buffett and Abel announcing plans to retain these holdings “for 50 years or more,” it’s now certain they are a long-term cross-border reallocation of capital. What was initially a "turn every page" test has turned into a pillar $20B bet on global commodities, energy, and infrastructure. Significantly, Berkshire is in talks to increase the 10% ownership cap, a sign of deeper strategic alignment. These are compounding positions, infused in sovereign economies with good demographic and fiscal policies.

The Apple investment, $135 billion as of Q1 2025, also needs to be reframed. In the AGM, Buffett explained how “Tim Cook has made Berkshire more money than I ever have.” This is not flattery; it’s reality. Apple’s capital return program, sticky margins, and hardware-dominant ecosystem represent a synthetic dividend engine to Berkshire, which has sold very few shares over the long term. As Apple increasingly uses more AI at the edge, the long-term total return thesis remains intact. Unlike traditional tech plays, however, Apple provides capital preservation in addition to growth, a requirement of Buffett’s capital at scale.

What unites the portfolio positions is not merely their scale but their holding period. Berkshire does not trade. Berkshire accumulates, and it absorbs. From American Express to its energy plays, the firm keeps adding to a tax-efficient, globally dispersed portfolio that acts like a sovereign wealth fund, a fund whose risk stance is intentionally asymmetric.

Source: Morningstar

Valuation: Optionality Remains Undervalued, and the Market Continues to Misprice Duration

On first thought, Berkshire's valuation seems stretched on traditional multiples. Its forward P/E of 24.82x is a full 128% above the financial sector median (10.89x), and even its price-to-book of 1.70x is above the 1.22x peer median. The premium is anything but speculation. It's a tribute to intrinsic optionality and fortress-like protection on the downside. Shareholders aren’t paying for today’s profits. They're paying to utilize more than $180 billion in cash equivalents and short-term Treasuries at scale with impeccable timing, a structural characteristic most institutions don’t have.

Significantly, the optics of overvaluation evaporate when considered through an enterprise-value framework. Berkshire is valued at a mere 7.65x EV/EBITDA, a 32% discount to the sector median, and 8.60x EV/EBIT, 28% shy of its peers. Not only is this anomalous in a compounding FCF and low-leverage business, but it is also a 40% discount to Berkshire's own 5-year EV/EBITDA average of around 13x. In substance, the market still values Berkshire as a static insurance conglomerate instead of a dynamic capital allocation engine with built-in crisis convexity.

The oft-quoted "Berkshire owns 5% of the U.S. Treasury market" is exaggerated. Comparing ~$335 billion of Treasuries and short-dated securities against a $27 trillion-plus U.S. Treasury marketplace, Berkshire's share is more like 1.2%. Nevertheless, the message applies: the firm is a quasi-sovereign liquidity pool and a buyer of last resort when capital markets become dislocated.

Valuation scenarios anticipate a broader upside than consensus models do. Assuming a normalized power of earnings of ~$45B and using a conservative multiple of 15x results in a base case value in the neighborhood of $610/share. In the case where Berkshire returns to its 5-year average EV/EBITDA of ~13x on EBITDA of ~$53B now, the implied enterprise value accommodates a target price of $685/share. The stock is selling at a 16-25% discount of its intrinsic value at the prevailing price of ~$513, a discrepancy that diminishes only when volatility returns and Berkshire's capital allocation leadership resumes attention.

Source: seekingalpha.com

Conclusion: The Compounder of Last Resort

Berkshire Hathaway is still an asymmetric vehicle in an otherwise symmetric market. Its cash is not on the sidelines but is strategic ammunition. Its high multiples are not excess but an intrinsic price of long-duration optionality and resilience. As markets reprice duration, liquidity, and sovereign risk, Berkshire will re-emerge not simply as a defensive stalwart but as a rare compounder with acceleration in its DNA. At $513, investors aren’t buying a yield on earnings. They’re buying time, leverage-free flexibility, and the world’s most disciplined capital allocator. In a speed-addicted world, Berkshire’s slowness is its keenest edge.

Recommended Articles