CVS Health 2.0: Leaner, Smarter, Stronger

- Q1 2025 adjusted EPS rose 72% YoY to $2.25, with $94.6B in revenue (+7%) and $4.6B in operating cash flow, supporting revised full-year guidance of $6.00–$6.20 in adjusted EPS.

- Health Care Benefits operating income surged 170% to $1.99B, while Health Services and Pharmacy grew 18% and 11.6% respectively, highlighting strategic execution across CVS’s pillars.

- CVS trades at 11.03x forward EPS and just 0.39x EV/sales—over a 90% discount to sector peers—despite $7B in annual cash generation and strong segment leadership.

- Legal liabilities (e.g., $387M Omnicare judgment), front-store softness, and competitive headwinds could delay revaluation—but current price implies minimal terminal growth expectations.

TradingKey - In the midst of a chaotic healthcare environment of price scrutiny, margin pressure, and shifting consumer behavior, CVS Health (CVS) has undertaken a conscious shift: less bulk, more acuity. At first glance, Q1 2025 headline figures look good: $94.6 billion in sales (+7% year-over-year), $4.6 billion in operating cash flow, and $2.25 in adjusted EPS, up a robust 72% from $1.31 last year. It is a more complicated story, however, underneath these figures of portfolio trimming, pending litigations, and reset expectations.

CVS's recent announcement to leave the ACA individual exchanges in 2026, discontinue its ACO REACH participation, and divest its MSSP operation is not a retreat into fee-for-service. It's a strategic realignment. This restructuring looks defensive on the surface, but coupled with its increased 2025 adjusted EPS guidance ($6.00-$6.20) and maintained adjusted operating income guidance by segments, it is a sign that CVS is intentionally moving away from low-margin and high-regulatory exposure to platform-based care delivery and integrated pharmacy solutions. Although GAAP EPS was lowered to ($4.23-$4.43), the delta is due to discrete charges and not weakening operations.

At a market price barely above 10.7x on forward adjusted earnings, such a blend of clean execution, aggressive streamlining, and resilient cash generation has the potential to represent an asymmetric upside. In the event this thesis plays out, investors are not simply viewing a defensive value opportunity. They might be seeing the re-rating of a more agile and capital-efficient CVS 2.0 amid healthcare service market expansion.

Source: The Business Research Company

Under the Umbrella: A Streamlined Engine with Segmental Momentum

CVS has an operating model with three vertically synergistic pillars: Health Care Benefits (HCB), Health Services (Caremark, Oak Street, Signify), and Pharmacy & Consumer Wellness. The combined structure allows for operational leverage and cost management and amplifies engagement with its close to 185 million customers. Although conglomerate complexity has been derided in the past, recent quarters reveal how CVS is leaning into its pillars and trimming non-scaled outliers.

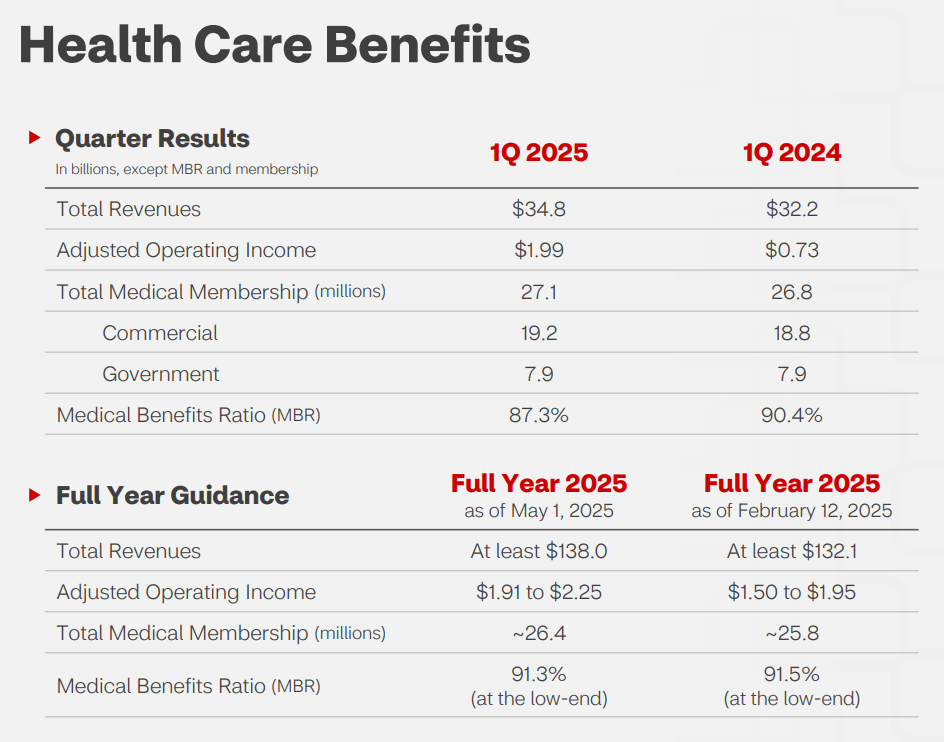

HCB recorded a Q1 2025 operating income of $1.99 billion, more than 170% higher than the prior year, driven by better prior-year reserve developments and better-performing Medicare Advantage. Although Medicaid volume was flat and commercial premiums were down, better Star Ratings and prudent management of costs reduced the Medical Benefit Ratio (MBR) to 87.3% from 90.4%. Of particular note is a $431 million deficiency reserve added in 2025, indicating CVS is managing the downside proactively.

The health services business contributed $1.60 billion in adjusted operating income (+18% year-over-year), fueled by specialty pharmacy expansion, enhanced purchasing economics, and improving brand drug mix. The coming Caremark July 2025 formulary shift towards favoring Wegovy (Novo Nordisk’s GLP-1 product) represents more than an operating adjustment—it represents a larger commitment to therapeutic cost-effectiveness. In the meantime, Oak Street and Signify Health fueled care delivery engagement increases, providing scale at local levels and supporting CVS’s long-term value-based care thesis.

Pharmacy & Consumer Wellness generated $1.31 billion of adjusted operating income (+11.6% year-over-year), as prescription volume accelerated (+4.3%) and same-store sales rose (+14.2%). The front store is a continued drag with traffic declining and softer discretionary spending. Nonetheless, rollouts of CVS CostVantage, its transparent price model for pharmacies, are on track and may eventually become a game-changer in helping to combat reimbursement pressure.

Together, these outcomes reinforce a focused triad approach: limit exposure to capital-intensive programs, double down on scalable wellness and care platforms, and deploy omnichannel pharmacy distribution to preserve margins. The structural realignment seems less defensive and more about positioning to leverage embedded operating leverage and long-term efficiency.

Source: Q1 Deck

A Defensive Moat or Simply Better Timing?

CVS's operating segments are resilient, but how do they compare to competitors? Relative to UnitedHealth Group (UNH), which has a larger scale in managed care and tech-enabled services through Optum, CVS still lags in margin breadth and innovation pace. CVS is not seeking to outspend UNH but to out-focus it.

In managed care, CVS is doubling down on its Medicare Advantage strength. While UNH’s MBR has ranged in the low low-80s, CVS’s fall to 87.3% (despite ACA challenges) indicates an upside. CVS's tactical retreat from ACA market participation mitigates both politics and price risk, a notable contrast to Centene and Elevance, which are more heavily ensnared by exchange-driven turnover.

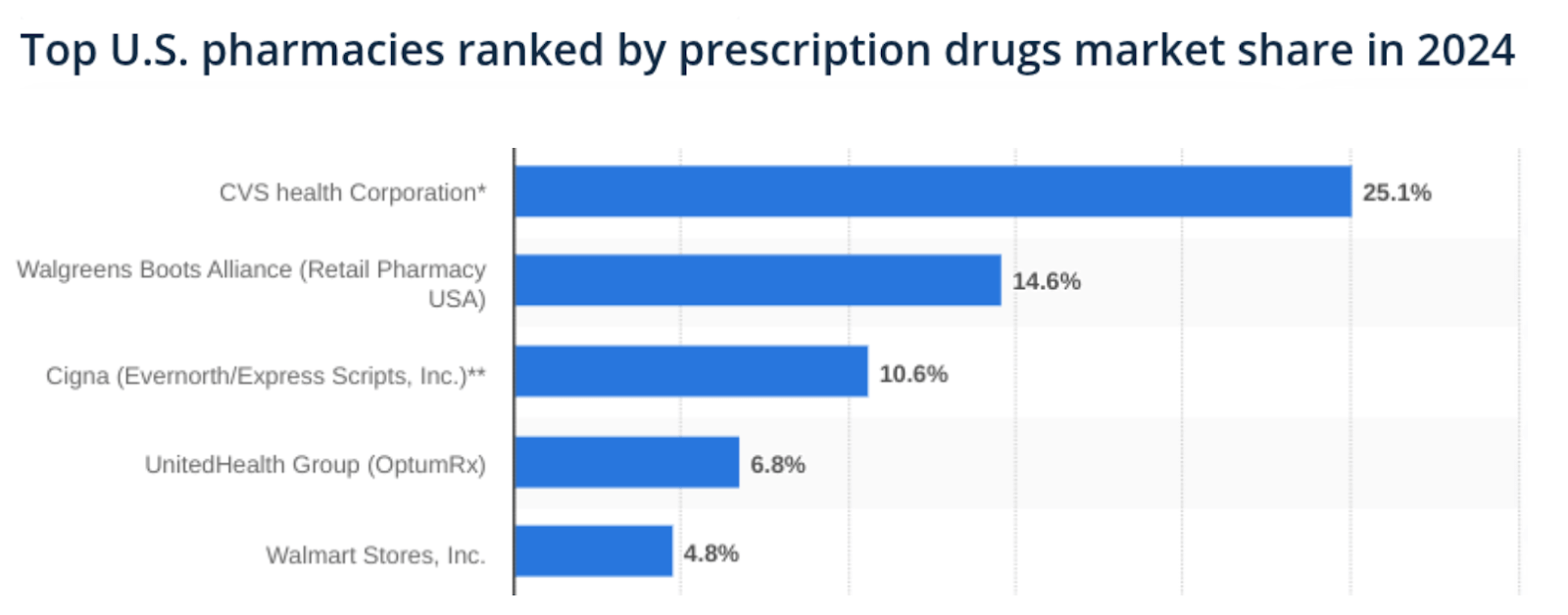

In pharmacy benefits management, CVS Caremark is still #2 by size and has ~27.6% of the US retail pharmacy script share as of Q1 2025. With close to 465 million pharmacy claims processed this quarter and strategic alliances such as the deal with Novo Nordisk on Wegovy access, CVS is taking back price narrative leadership from Cigna’s Express Scripts.

On the back of Walgreens’ (WBA) operational struggle and Rite Aid’s bankruptcy, the door is open for CVS to extend its 9,000+ unit moat. The long-run headwind persists, however: slowing foot traffic and front-store profitability. CVS’s strengths are its clinical integration, vaccines, testing, and consultations on health, not soda and makeup. The firm is already aware of it and positioning itself accordingly.

Although CVS cannot dominate on all fronts, its diversified strategy presents a counter-cyclical blend: stable insurance economics in healthcare, high-volume prescription demand, and scalable digital and home care growth. In a rate-volatile environment, such a configuration increasingly looks like a risk-mitigated asset allocator more than a retail-biased conglomerate.

.png)

Source: Q1 Deck

Deep Value in Plain Sight: A Valuation Gap Worth Taking Advantage Of

CVS's present multiple reflects a market story detached from its normalized power of earnings. The stock, at $66.97 a share, sells at merely 10.7x forward non-GAAP EPS, a discount of 35.7% to the industry median of 17.7x. Trailing the multiple compresses even more to 10.53x, validating consistent pessimism in terms of valuation regardless of operations execution. This disparity becomes even greater when referenced against CVS's own 5-year average P/E of 9.92 (forward) and 9.69 (TTM), supporting a reversion mindset and not overvaluation.

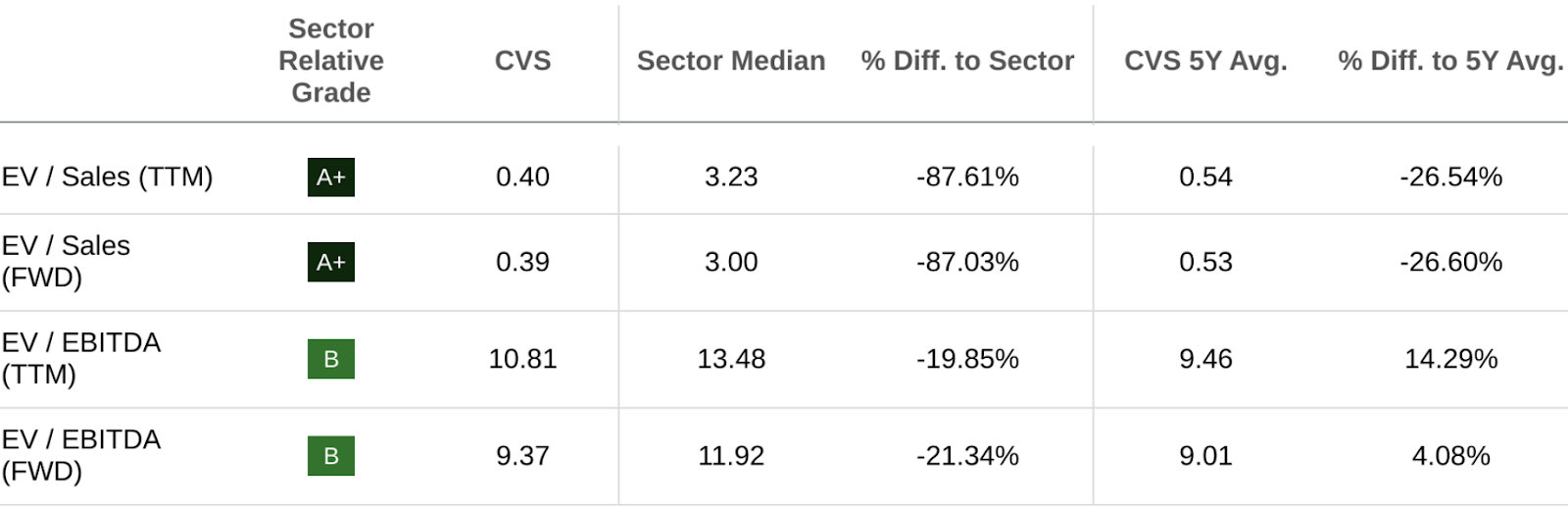

The undervaluation becomes even more compelling when examined through an enterprise value lens. CVS is quoted at 0.39x EV/sales (FWD) and 0.22x price/sales (TTM), putting it at a stunning ~87% discount to industry peers. Deep compressions like this are a rare occurrence in a company with $7B of annual cash generation and leadership positions in retail pharmacy, managed care, and pharmacy benefit management. The firm's EV/EBITDA multiples of 10.81x (TTM) and 9.37x (FWD) are slightly lagging peers but in no way materially depressed, indicating EBITDA is being reasonably rewarded but the equity component is underweighted in the capital structure story.

Notably, the PEG multiple (forward non-GAAP) is 0.74, putting CVS in a select group of large-cap stocks with a <1x PEG multiple. This indicates the market is discounting any earnings growth, even as it has been guided by management towards higher adjusted EPS and wider operating margins. Even its price/book multiple of 1.05 is ~55% below the sector median, even as it has $10B+ in cash and a good asset base.

Although litigious noise and exit-restructure pressure might have momentarily tainted sentiment, such multiples now imply little in the way of terminal value appreciation. Simply reverting to its own historical range of multiples, never mind the levels of peers, has upside written all over it. A rerating to a simple 13x on forward EPS would imply a $79–$81 share price versus around $67 currently, representing ~18–21% upside without any multiple expansion to levels seen in the group. Add to this a growing dividend stream, solid balance sheet, and enhanced cash flow dynamics, and the story is difficult to dismiss.

Source: seekingalpha.com

Risk Factors: Litigation, Traffic at the Soft Store, and Competitive Squeeze

Even with its positive momentum, CVS has real risks that will dampen several expansions. Foremost among them is the threat of legal action. The $387 million Omnicare judgment, pertaining to pre-purchase dispensing procedures, introduces reputational and financial uncertainty. While CVS has announced appeal plans, additional legal provisions cannot be discounted. The spread between its GAAP/adjusted earnings is already large and could increase further if additional cases are filed.

Second, soft consumer demand in front-store retail persists as a detractor. Although peripheral to the firm's story, front-store margins are still a material component and are lagging. Unless traffic does recover or deteriorates further, CVS might have to restructure or monetize segments of its retail platform, particularly in poorer-performing markets. Finally, the competitive pressure on managed care and pharmacy benefit management is still on the up. Cigna’s Express Scripts is also deploying AI-adherence tools, and Humana is competitively pricing up Medicare Advantage plans aggressively.

CVS's capacity to retain and increase high-value members without sacrificing margins will be challenged in the bid cycle of 2026. If any of these vectors decline at the same time, CVS's discount on valuation may endure even as it experiences growing adjusted earnings. Mitigation will rely on effective execution in platform bundling, digital member retention, and cost containment in clinical and logistic operations.

Source: statista

Conclusion

CVS trades at a deep discount despite strong fundamentals, rising adjusted EPS, and robust cash flow. With litigation risks isolated and strategic realignment underway, the valuation suggests an outsized upside. If CVS reverts to even modest historical multiples, investors could unlock meaningful gains from a stable, cash-generative healthcare platform.

Recommended Articles