Tesla’s Next Act: Betting on AI, Energy, and Operating Leverage Amid Demand Uncertainty

- Energy and Services gross profit grew 39% year-over-year, offsetting a sharp decline in automotive revenue, as Tesla’s software and infrastructure segments increasingly contribute to margin expansion and financial stability.

- Tesla trades at a 170.82x forward P/E, nearly 940% above the sector median, signaling extreme valuation tied to future AI, autonomy, and energy monetization rather than current automotive fundamentals.

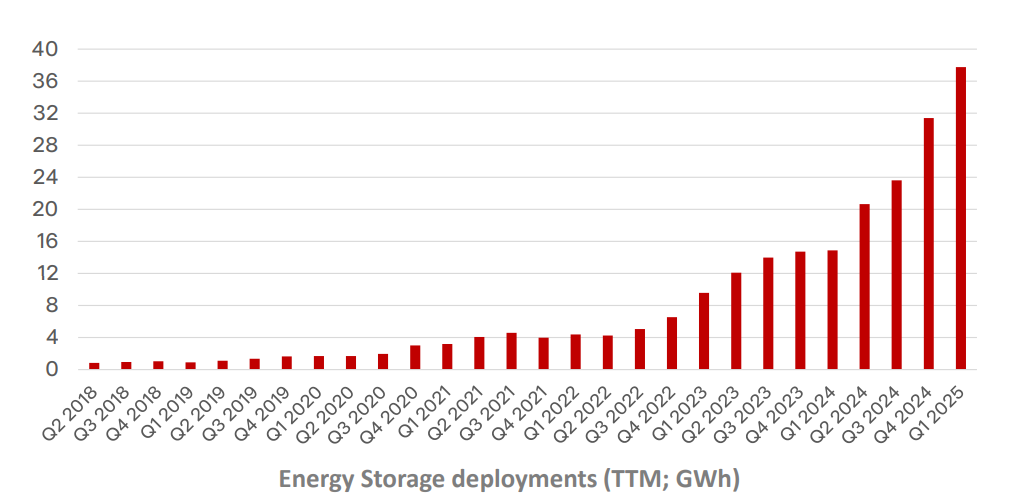

- Megafactory Shanghai produced over 100 Megapacks in Q1, fueling a 35% year-over-year increase in Energy and Storage revenue, with scalability that may soon outpace automotive growth globally.

- Autonomy and software monetization could add $40–$60/share in equity value, but delays in regulatory approval or execution could leave Tesla’s valuation vulnerable, with a rationalized fair value closer to $150–$170/share.

TradingKey - In spite of the market's preoccupation with Tesla's (TSLA) deceleration of delivery volumes and margins contraction, the far more important transformation is happening quietly beneath the surface. Tesla is transforming from a simple EV maker to a vertically integrated autonomy and energy platform. This transition has both been a necessity and an opportunity for the company. As conventional automakers catch up on EV production, Tesla is competing fiercely on full-stack AI, autonomous logistics, and grid-scale energy deployments. The Q1 2025 earnings support this thesis: automotive revenues fell precipitously, yet energy and services gross profit grew, and software-driven plays like Full Self-Driving (FSD) and Optimus robotics transitioned from promise to execution.

However, the market is divided. Tesla’s 145x forward P/E (non-GAAP) is either a sign of irrational exuberance or a pre-emption of AI-driven operating leverage that has not yet occurred. The company is strategically placed to unlock asymmetric potential across three axes: a highly localized cost base, an AI-born software stack with fleet-wide economies, and a capex-light growth trajectory through energy storage and autonomy. But that potential is still exposed to geopolitical trade disruptions, delayed autonomy revenue, and investor tolerance for a mythical monetization horizon.

Source: Q1 Deck

From Cars to Code: Breaking Down Tesla’s Business DNA

Tesla's business no longer fits the definition of "car manufacturing." The latest numbers from the company reveal a consistent shift toward services, software, and grid energy, which are light on operations and heavy on margins. Tesla brings in billions of revenue from energy and services, both of which became substantial contributors to gross profit. Services and Other were especially noteworthy for their year-over-year profit expansion due to enhanced collision and service efficiency.

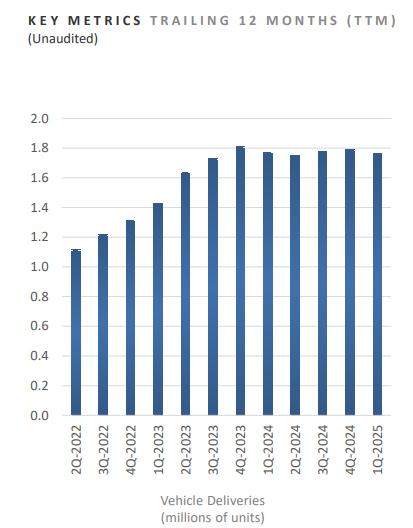

In the meantime, auto deliveries slipped as Tesla halted lines to upgrade for the Model Y. The transition coincided with the introduction of lower-priced variants and forthcoming offerings such as the Cybercab, a Robotaxi platform based on Tesla’s next-generation unboxed manufacturing strategy. Tesla’s plant capacity is over three million vehicles a year, but production utilization is still throttled by macro headwinds and planned factory retrofits.

Tesla is refining its value creation engine on four interconnected flywheels: autonomy, AI hardware, energy storage, and vertically integrated logistics. Model 3, Model Y, and Cybertruck vehicles are autonomously driving out of production lines to outbound lots. FSD (Supervised) launched in China with no market-specific training data, showcasing Tesla’s superiority in end-to-end neural net generalization. On the hardware side, IRA-compliant 4680 cell puts Cybertruck in a position for a tax credit while onshoring Tesla’s battery supply chain. These are structural cost advantages that few OEMs are able to match.

Source: Q1 Deck

Red Ocean to Deep Tech: Navigating the Competitive Minefield

Tesla’s quarterly report refuses to sugarcoat increased competition within the EV and AI spaces. As the general EV market gets commoditized, especially within China, where local companies are bringing out competitively priced vehicles, Tesla is betting on defensibility based on real-time AI and energy software rather than mere unit economics. The goal is now selling autonomy as a fleet software solution and not just vehicles.

Tesla no longer only competes against mainstream OEMs: it is now competing with technology companies on AI infrastructure, data aggregation, and control of the OS. It has an advantage based on vertical integration: it controls the sensors, the training data, the compute stack, and the inference runtime. This lowers marginal cost per software update and allows for things like unsupervised outbound logistics and multi-region FSD deployment with minimal localization.

Tesla's energy business is likely even more disruptive. Although the automotive business had a material revenue drop, Energy and Storage revenue jumped on the back of Megapack and Powerwall installations.

Megafactory Shanghai manufactured over 100 Megapacks during the quarter, which primes it for scalable expansion globally without additional U.S. CapEx exposure. Energy could grow even faster than auto over the next five years, particularly as AI load growth creates unprecedented pressure on the world's power grids. Tesla’s grid-stabilizing storage products are already taking hold with utilities and enterprise customers, where there is no legacy OEM footprint.

Source: Q1 Deck

Recalibrating the Machine: Valuation Signals and Strategic Optionality

Tesla’s valuation profile is still one of the most highly contentious on public markets, and for a good reason. At $276.22 per share, the company trades at stratospheric levels across nearly every earnings and revenue-based multiple, particularly relative to sector medians. The company’s forward P/E is 170.82, some 939% higher than the sector median at 16.45, and even its trailing non-GAAP P/E of 123.31 is 777% higher compared to peers. These levels are not only rich on a visual basis, they are historically aberrant. And Tesla’s current P/E is 10.5% less than its five-year average, implying that while valuation is extreme on a relative-to-peer basis, the market has already factored in a depth of cyclical contraction.

Tesla’s EV/EBITDA forward multiple of 61.16, versus a sector median of only 9.41, represents a 550% premium, while EV/EBIT is at 146.82, 917% higher than the sector, although 3.6% below Tesla’s own five-year average. This discrepancy indicates a widening divergence from current profitability and long-term expectations based on AI and autonomy monetization.

Revenue multiples say the same thing. Tesla's forward EV/Sales is 8.81, 683% higher than average, with a Price/Sales of 9.25, way higher than the sector average of 0.83 by over 1,000%. Even its Price/Book is rich at 11.91, five times higher than the sector average of 1.94, although 44% lower than its five-year average of 21.46. These outliers suggest that Tesla is not being priced as a typical automaker but as a growth platform with hidden operating leverage from software, energy, and robotics.

Forward Non-GAAP PEG is 6.73 compared to the sector average of 1.46, which indicates the market is pricing a premium for anticipated growth but that growth needs to expand substantially to cover the difference. The fall in forward P/E compared to its five-year average (276.92 vs. 170.82 currently) indicates that the market is revising terminal growth estimates and infusing more doubt about near-term earnings realization.

Tesla's valuation at current levels has a lot of optionality built into it but not much margin for error. Unless revenue from autonomy is tapped or energy storage grows profitably, Tesla's premium is at risk of a meaningful return to industry-aligned multiples. Simply put, the company is still priced for perfection, but is facing a less sympathetic, more uncertain macro and regulatory environment.

Source: iea.org

Actionable Insights: Navigating Tesla’s Asymmetric Curve

Tesla's present price has built-in expectations, but not unrealistic ones assuming software and energy flywheels kick into action. Institutional players ought to position exposure as a call option on vertically monetizable AI, rather than a conventional auto investment. The following are the most actionable takeaways:

Its cash-rich balance sheet and capital expenditure-light shift guarantee financial resilience up to 2025 even with macro headwinds. The threat of a liquidity crisis is low. Energy Storage would surpass Services as a contributor to gross profit by the middle of 2026, forming a separate revenue source that compounds independently of the sale of vehicles.

Monetization of Robotaxi and FSD may push Tesla into a two-part profit arrangement (hardware + SaaS) but only when there is a clearing of pending regulations and technology by 2026 at the latest. Otherwise,deferred revenue is a mirage for margins. Using a 45x multiple on a $2.50 FY24 non-GAAP EPS equates to a fair value of about $112. Factoring-in future software optionality (FSD, Optimus, energy services) at a premium adds $40–$60 per share, for a rationalized bull-case target price of $150–$170. At current prices, Tesla has asymmetric potential for gain but no room for error.

Source: Voronoi

Conclusion

Tesla is no longer an EV story anymore. It is a convergence play, AI, autonomy, energy, and manufacturing innovation. This quarter is a sign of pain in the near term but a platform that is in incubation. The patience of the market shall be tried. But for long-term players who want exposure to a full-stack AI deployment thesis with real-world scale, Tesla provides something that not many do: leverage to electrons as well as to algorithms.

Recommended Articles