IONQ: The Quantum Inflection Point: From Experimental Promise to Market-Making Potential

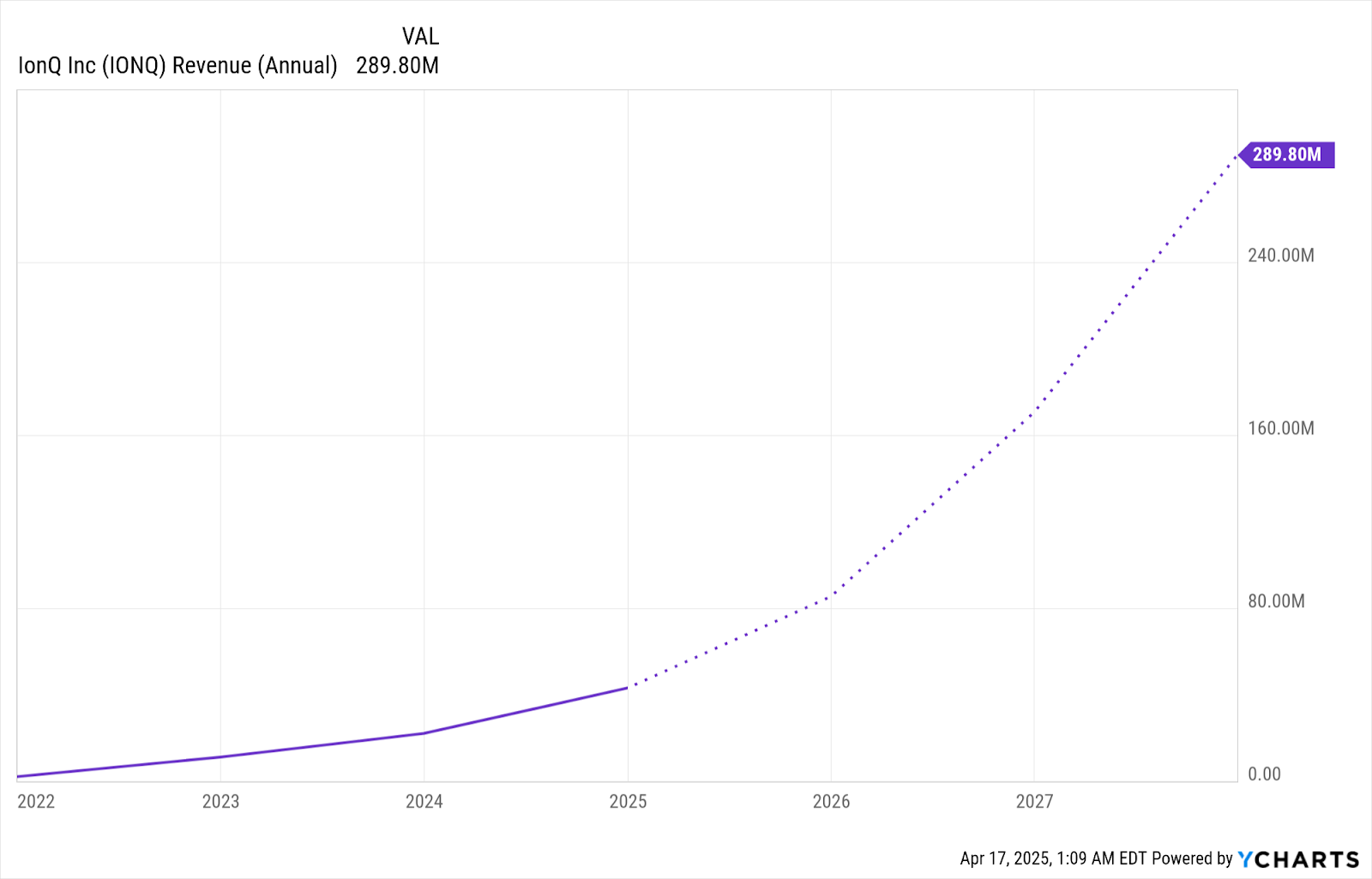

- IonQ forecasts up to $95 million in FY25 revenue, reflecting a 97% YoY growth rate and nearly doubling revenue annually since IPO, signaling a commercial inflection point.

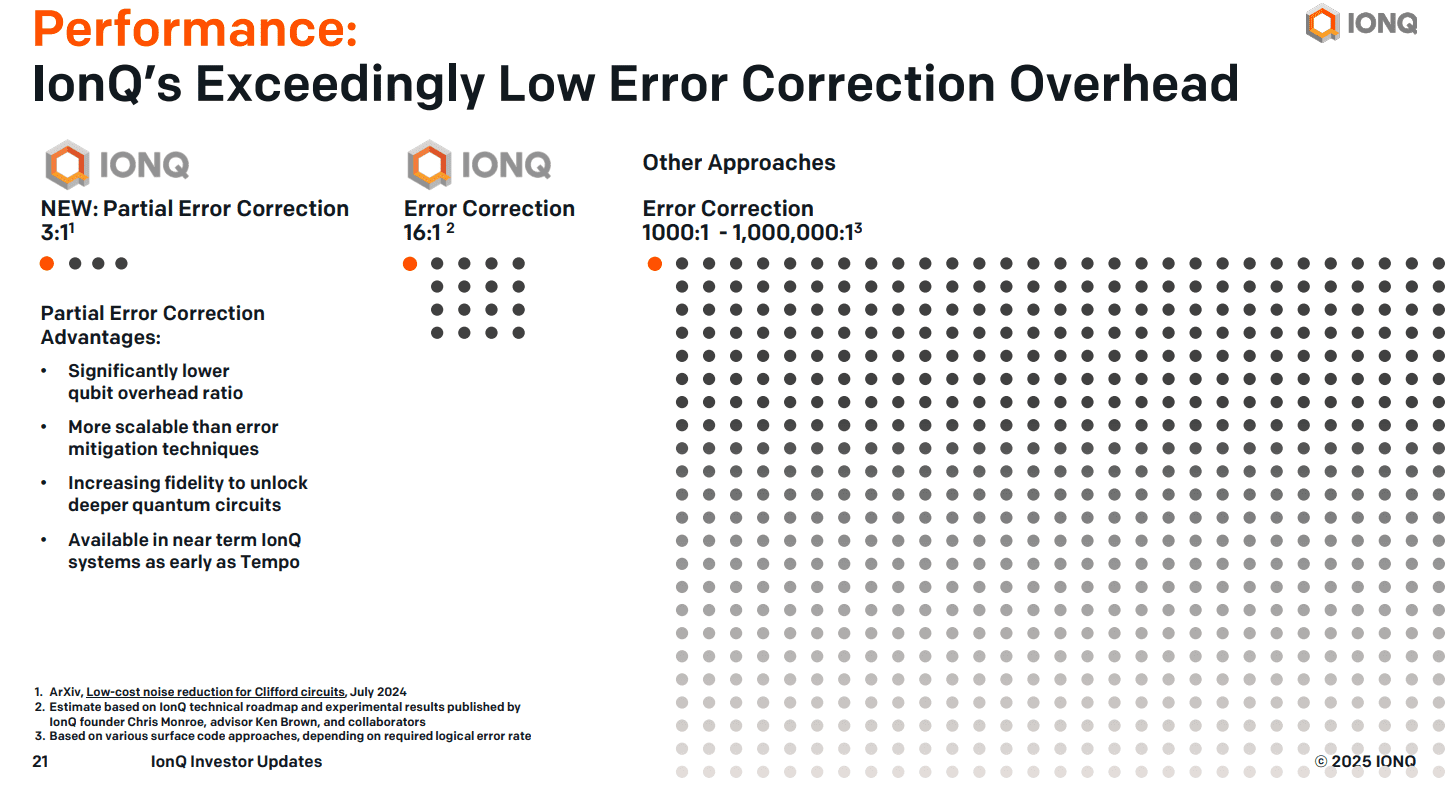

- Its Forte system achieved 99.9% two-qubit gate fidelity with only 16:1 correction overhead, enabling more scalable quantum solutions versus competitors requiring 1,000:1 correction.

- With 900+ quantum-related patents and cloud integrations across AWS, Azure, and Google Cloud, IonQ owns both the intellectual moat and distribution to scale Quantum-as-a-Service.

- IonQ targets a $880 billion quantum market by 2040, with its acquisition of Qubitekk and ID Quantique unlocking $36 billion in secure quantum networking upside.

TradingKey - Within only four years since going public, IonQ (IONQ) has gone from being an experimental quantum startup to a leader on one of the most revolutionary technology frontiers of the 21st century. As the wider market fixates on the race to raw qubit counts, IonQ’s differentiated approach to execution, based on its trapped ion architecture, modular scalability, and commercial-grade hardware, ports an asymmetric opportunity for long-term investors. It is IonQ’s move away from solely academic advances toward a reproducible business model centered on practical deployment, revenue expansion, and strategic IP building that differentiates it. While most quantum hardware firms are years away from deploying functional systems, IonQ’s Forte Enterprise systems are being shipped to customers, including QuantumBasel, an innovation hub for Europe.

In addition, IonQ's $364 million cash position and estimated 97% year-over-year revenue growth to FY25, reaching potentially as high as $95 million, represent an inflection point not only in story but in fundamentals. The company's revenue has almost doubled annually since its IPO and recently sits atop a patent moat of more than 900 filings across quantum computing, networking, and related technologies. Combined with an estimated $880 billion addressable quantum market through 2040, IonQ compares to only a handful of publicly traded companies with legitimate long-term commercial upside within quantum computing.

Source: Investor Deck

Architecture Over Arms Race: How Trapped Ions Are The Winning Modality

In contrast to competitors like IBM, Rigetti, and PsiQuantum, which depend upon superconducting or photonic modalities with harsh scaling and error correction requirements, IonQ's foundational advantage is its trapped ion architecture, a modality that provides natural atomic homogeneity, room-temperature operation, and higher gate fidelity. Its most recent platform, Forte, achieved 99.9% two-qubit gate fidelity with remarkably low error correction overheads (16:1 for full correction and 3:1 for partial correction), as opposed to 1,000:1 or worse for comparable platforms. The result is expressed for real-world performance: IonQ's systems exhibit greater time-to-solution speed and reduced energy consumption per computation, a key consideration for commercialization.

Most compelling is IonQ's multi-core, modular roadmap, which accommodates photonic interconnects and a future path to 1,000+ qubits across quantum networks. In contrast to other architectures that demand cryogenic operation and closest-neighbor qubit communication, IonQ's systems leverage all-to-all connectivity, ultra-high vacuum trap package miniaturization, and room-temperature operation, and are thus deployable in existing data center environments. These features minimize infrastructure cost and enable faster time-to-solution for actual commercial applications such as chemical modeling, supply chain optimization, and detecting fraud.

What sets IonQ apart still, however, is its focus on system integration and hybrid compute environments. IonQ is the sole hardware provider to be available on all three major cloud platforms, AWS, Microsoft Azure, and Google Cloud, offering developers and business users both flexibility and convenience and minimizing onboarding hurdles. It not only positions IonQ as a hardware leader but as a platform-ready company as well, at the vanguard of the quantum-as-a-service economy.

Source: Investor Deck

Disruptive Edge: Strategic Placement within an Expanding Quantum Environment

IonQ is positioning itself at the intersection of quantum computing and quantum networking. With recent buys, Qubitekk and its commercial Bohr IV quantum network, and a binding agreement to acquire ID Quantique, IonQ now owns two of the most commercially viable quantum networking stacks, expanding its revenue base. With this integration, IonQ can be at the forefront of developing secure quantum communication platforms and distributed quantum computing architectures, a market that is projected to generate as much as $36 billion of economic value for 2040.

Additionally, IonQ's singular collaborations with hyperscaler clouds and hybrid classical-quantum programs with NVIDIA's CUDA-Q show robust traction with both hyperscalers and business customers. It boosts distribution while lowering the cost of acquiring customers, an accomplishment few competitors can match. Government demand for IonQ’s roadmap is further supported: a $21.1 million order with the U.S. Air Force Research Lab to implement secure quantum networking infrastructure, as well as its position as anchor of Maryland's $1 billion “Capital of Quantum” program, reflects robust institutional confidence.

IonQ is geographically expanding as well, with new deployments into North America, Europe, and Asia. Its recent strategic agreement with SK Telecom to bring IonQ systems into South Korea's AI stack is a recent example. Another partnership with Ansys is focused on accelerating engineering simulations, and collaborations with GDIT (General Dynamics IT) investigate AI-driven cybersecurity and finance anomaly detection. These disparate applications suggest a flywheel of demand for enterprises growing as algorithmic qubit numbers and system reliability increase.

Quantum Valuation: Framing Upside with Strategic Discipline

At an enterprise value under $2.5 billion, IonQ is trading at a forward EV/Revenue of around 67x, based on its top-end FY25 revenue guidance of $85 million. While this may look rich versus comparable hardware incumbents, it is not out of line with deep-tech disruptor valuation premia for those at commercial inflection. IonQ's close-to-100% revenue CAGR, commercial adoption of Forte Enterprise, and lengthy multiyear governmental procurements underpin this premium. Its growth path is not conjectural but based on delivery, revenue has doubled for three years running, and FY25 should be no different.

IonQ's impressive cash position of $360 million allows it to grow production capacity, make strategic buys (such as ID Quantique), and expand internationally without future dilution or debt. With a portfolio of more than 900 patents, sole-purpose architectures at stake, and hybrid-ready platforms supported across all major clouds, IonQ now enjoys several monetization levers, system purchases, cloud computation fees, algorithm development, and quantum infrastructure backed by governments.

By 2026, if IonQ achieves its multi-core scaling targets and Tempo platform adoption takes hold, IonQ could be generating annual revenue of more than $170 million. Using a 50x forward EV to that number suggests an enterprise worth of $8.5 billion, a return of well more than 40% above current levels. As pilot-phase use cases convert to production, IonQ’s valuation cap will be determined not by market stories but by reproducible economics.

Source: Ycharts

Risks: Highly complex, Long timelines, and Competitive pressure

Notwithstanding its powerful architecture and early-mover advantage, IonQ is subject to a series of structural and operational risks that cannot be discounted. Foremost is the risk of execution involved with scaling quantum systems from niche application to enterprise-level utility. The road to general quantum advantage remains unknown and potentially longer than currently expected, especially as error correction and software architectures continue to advance. While IonQ has made significant progress along its roadmap, any technical slowdown or postponement of achieving performance benchmarks, such as AQ50+ machines or meshed QPU scaling, could suppress commercial traction.

Customer adoption risk is similarly material. As a majority of companies currently exist at the quantum exploration stage, typically based on consulting engagements or pilot engagements, if the environment does not evolve quickly to enable repetitive workloads and enterprise-level applications, revenue growth at IonQ could flatten out. Moreover, as customer sophistication rises, IonQ will need to demonstrate cost-effectiveness versus high-performance classical equivalents, a dynamic that could benefit hybrid solutions at the expense of outright quantum providers during the intermediate term.

Competitively, well-funded incumbents IBM, Google, and Amazon keep investing heavily in quantum technologies. As beneficial as IonQ's trapped ion modality is, these competitors have superior distribution channels, base of customers, and pipelines of talent. If a major advancement is found for superconducting or photonic qubits, IonQ's uniqueness will be erased.

Other risks include geopolitical exposure to quantum export regulations, IP protection issues with cross-border development, and the long tail of talent shortage for quantum. While IonQ established a good leadership bench, retaining high-skilled engineers and building out its manufacturing base are still long-term challenges. Finally, while there is a good balance sheet, negative EPS and limited near-term profitability could put pressure on shares at a time when investors are focused on cash and operating leverage.

Source: Investor Deck

Conclusion: It's a Platform Play in the Making

IonQ is not only developing quantum computers, it is designing infrastructure for an economic future where quantum advantage is not only commercially accessible but widely available. With a defensible architecture, irreplaceable patent moat, revenue growth accelerating, and worldwide presence across both quantum computing and quantum networking, IonQ is moving from a speculative gamble to a category leader with institutional significance. As application cases move out of the lab and into the business world, IonQ is well-positioned to become one of the few public companies at the center of quantum's economic future.

Recommended Articles