TradingKey’s The Week on Wall Street: Oil Spikes, VIX Surges, and the Return of the Inflation Scare

Previous Week’s Market Review & Analysis

TradingKey - Macroeconomic Landscape: The week was significantly influenced by escalating geopolitical tensions in the Middle East, which redirected global market sentiment towards risk aversion. This led to a notable rise in crude oil prices due to fears of supply disruptions through the Strait of Hormuz. Treasury yields also increased, fueled by concerns over inflation. Key economic data included a 0.5% rise in the Producer Price Index (PPI) for January, surpassing expectations and contributing to inflation worries. In contrast, the annual U.S. inflation rate for January slowed to 2.4%, with core inflation remaining at 2.6%. Mortgage rates continued to decline, with the average 30-year fixed rate falling to 6.09%. Conflicting data on the U.S. manufacturing sector was released on Monday, March 2, showing business activity indices above forecasts. The Federal Reserve’s Beige Book was released mid-week, and crucial U.S. labor market data, including Nonfarm Payrolls, the unemployment rate, and average earnings, were anticipated on Friday, March 6.

Market Performance Overview: Major U.S. equity indices experienced considerable volatility throughout the week. The S&P 500 saw a slight gain on Monday (+0.1%), a decline on Tuesday (-0.9%), a rebound on Wednesday (+0.8%), and closed down 1.33% on Friday. The Dow Jones Industrial Average followed a similar pattern, falling 0.1% on Monday, 0.8% on Tuesday, climbing 0.5% on Wednesday, and ending down 0.95% on Friday. The Nasdaq Composite gained 0.4% on Monday, dropped 1% on Tuesday, rallied 1.3% on Wednesday, and closed down 1.51% on Friday. Sector performance showed a rotation towards defensive areas. Energy and defense stocks rallied early in the week due to geopolitical concerns. Technology and financial stocks experienced sharp declines on Friday, while software stocks faced pressure amid artificial intelligence (AI) disruption fears.

Key Events Analysis: The primary market driver was the military escalation in the Middle East, which prompted significant risk-off trading and drove up oil prices. Corporate earnings reports were released by several companies, including Broadcom, Veeva Systems, Okta, Brown-Forman, Dycom Industries, CrowdStrike, Ross Stores, and Best Buy. Ross Stores notably climbed 8% following better-than-expected results. The January Producer Price Index (PPI) indicated higher wholesale inflation, adding to market caution.

Flows & Sentiment: Market sentiment was characterized by heightened risk aversion. The Cboe Volatility Index (VIX) surged, rallying 12% on Monday to close at 22.40 and later spiked 8%, indicating expectations of sharp market movements and a clear shift to a "risk-off" posture. Safe-haven assets such as gold and the U.S. dollar gained strength. Equity fund flows showed continued inflows into equity ETFs in February, with U.S. large-cap equities attracting significant capital, but there was also a notable rotation from high-growth stocks into more defensive value plays. Long-term U.S. funds recorded estimated outflows of $19.31 billion for the week ending March 4.

Overall Assessment: The U.S. equity market during the first week of March was largely dictated by geopolitical developments, prompting a flight to safety and increased volatility. While indices experienced daily swings, the underlying market logic reflected cautious investor sentiment, with a clear preference for defensive and value sectors. The elevated VIX underscored pervasive uncertainty.

Next Week's Key Market Drivers & Investment Outlook

Upcoming Events: The coming week will feature several significant economic data releases. The U.S. GDP Annual Growth Rate for Q4 (Secondary Estimate) is expected on Monday, March 9. The Consumer Price Index (CPI) for February 2026 is scheduled for release on Wednesday, March 11. Additionally, the Job Openings and Labor Turnover Survey (JOLTS) for January 2026 is due on March 13. Select corporate earnings reports, including BioNTech SE, United Natural Foods, Inc., and NET Power Inc., are scheduled for March 10.

Market Logic Projection: Geopolitical risks are anticipated to remain a dominant force, potentially overshadowing fundamental and technical market factors. The current elevated VIX suggests that market volatility is likely to persist. Any indication of sustained strength in labor market data or rising wages could reinforce the Federal Reserve’s tight monetary policy stance.

Strategy & Allocation Recommendations: Given the prevailing risk-off sentiment, a defensive strategy is advisable, favoring sectors like energy and traditional safe-haven assets. The market is expected to exhibit wider intraday swings and heightened sensitivity to incoming news. Continue to monitor the ongoing rotation towards cyclical and value-oriented stocks.

Risk Alerts: Geopolitical instability, particularly regarding the Middle East, remains a primary concern. The potential for persistent inflation, exacerbated by rising energy prices, could influence future central bank policy decisions. The elevated VIX signifies continued market volatility and the need for prudent risk management.

Markets Weekly

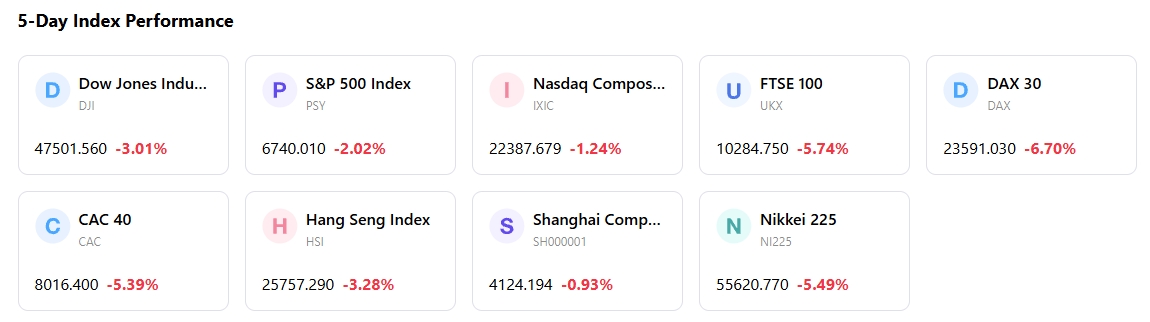

5-Day Index Performance

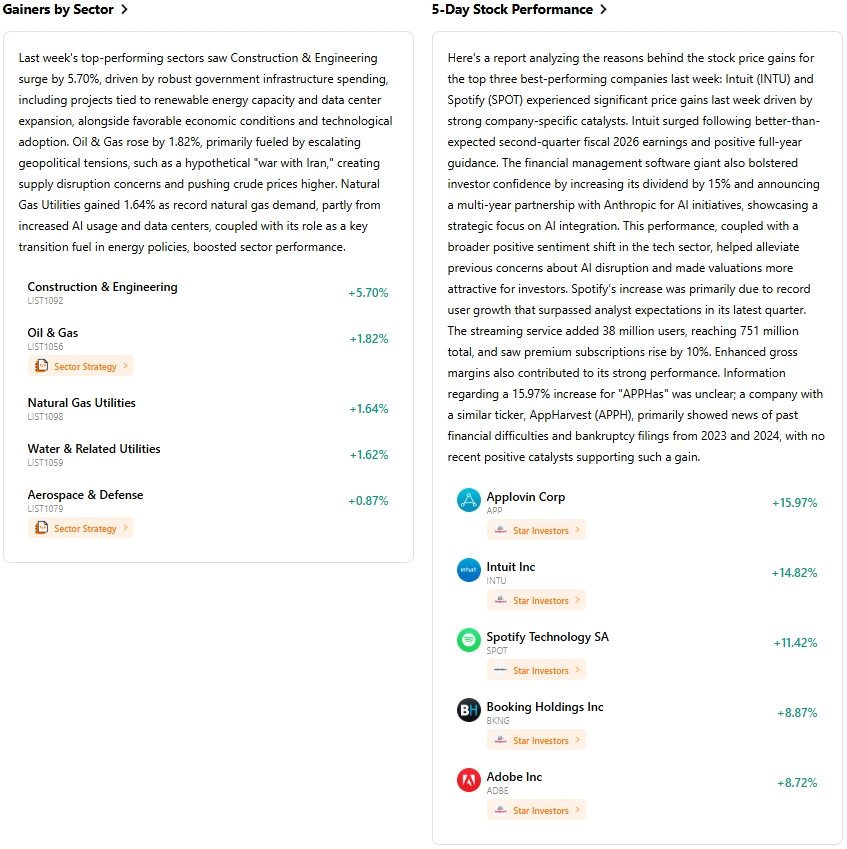

Recommended Articles