Markets Sell Off amid Iran Tensions — But Oil and Defense Stocks Hold Up

TradingKey - Following U.S. and Israeli airstrikes on Iran, investors are watching closely to see how U.S. markets will open on Monday. Early declines in Asia and Europe suggest pressure on equities, yet the sharp surge in oil prices could offer a lifeline for the energy sector.

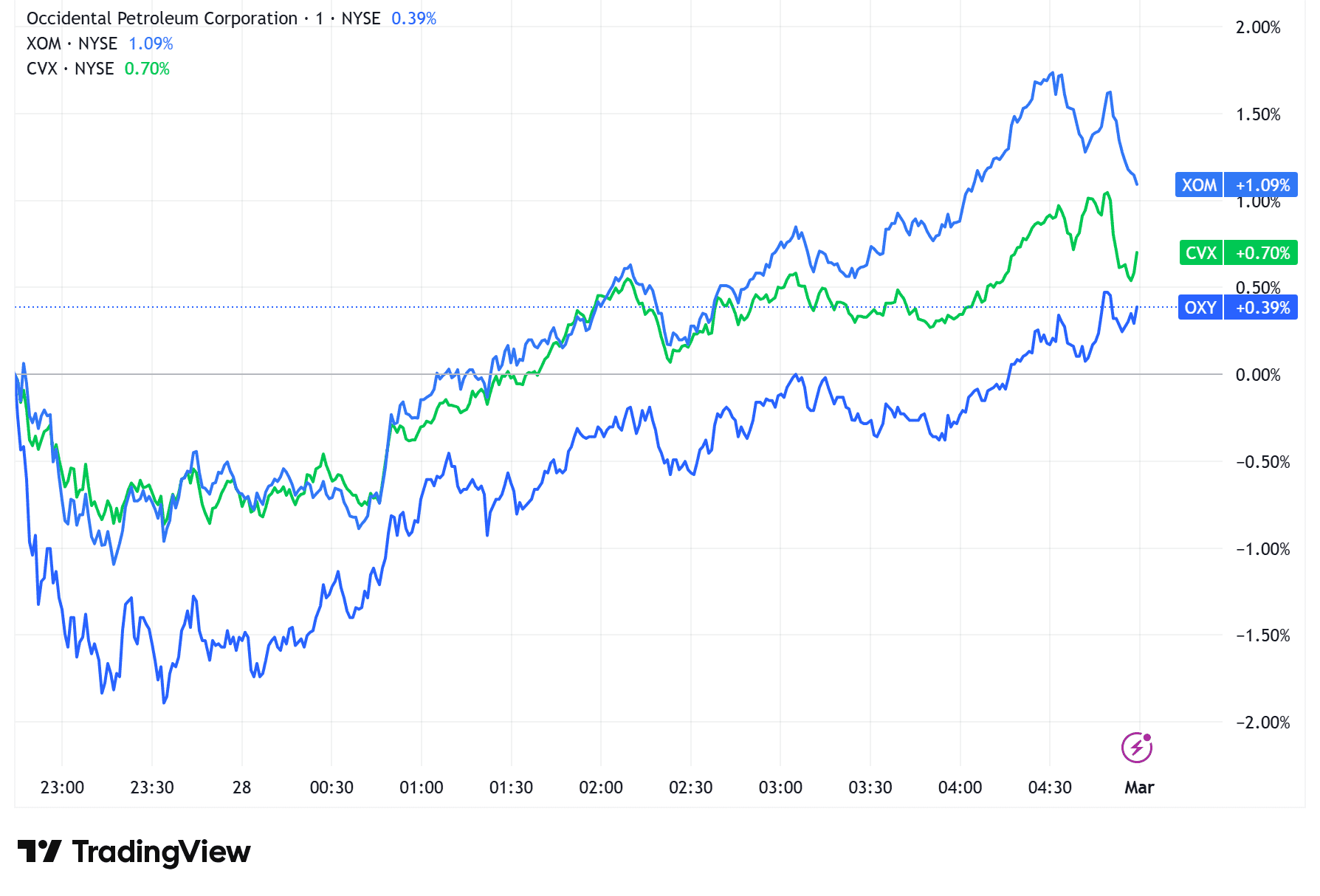

Oil Stocks Rise in Premarket

Against a backdrop of broad global sell‑offs, upstream and integrated oil companies are standing out as rare gainers. In U.S. pre‑market trading, energy shares climbed across the board — Occidental Petroleum Corp. (OXY) rose 6%, Exxon Mobil Corp. (XOM) gained 5%, and Chevron Corp. (CVX) advanced 4%.

The rally stemmed directly from the oil spike. After the strikes, Brent crude surged nearly 14%, from just above US $70 to over US $80 per barrel, while WTI climbed almost 12%. Analysts warn that if shipping through the Strait of Hormuz remains disrupted, prices reaching US $90 to $100 per barrel can no longer be dismissed as a low‑probability scenario.

For upstream producers and integrated majors, production is largely fixed in the short term — so every US $10 increase in crude translates into a disproportionate profit surge. Because this rise is driven by a risk premium, markets are now embedding assumptions of “persistently elevated prices” into forward earnings models, lifting valuation baselines across the energy sector.

Defense Stocks May Benefit

As cyclicals and indices slump, defense names are finding fresh momentum. The iShares U.S. Aerospace & Defense ETF (ITA) has gained roughly 35% since the first wave of strikes on Iran last year, while Lockheed Martin Corp. (LMT) and Northrop Grumman Corp. (NOC) shares are up about 40% and 46%, respectively.

Escalating war risk gives legislatures — from the U.S. Congress to allied parliaments — a straightforward argument for larger defense budgets. Spending on missile defense, drones, electronic warfare, intelligence and surveillance, and space‑asset protection appears set to climb. The mix of safe‑haven demand and order‑pipeline optimism is drawing investors toward defense stocks as natural hedges against geopolitical shocks, with many betting on sustained funding growth over the next three to five years.

That said, after years of rerating driven by the Russia–Ukraine war, Western defense equities are no longer deeply undervalued. Renewed turmoil in the Middle East adds another layer of risk premium atop already rich valuations — supporting prices now but potentially magnifying any future corrections.

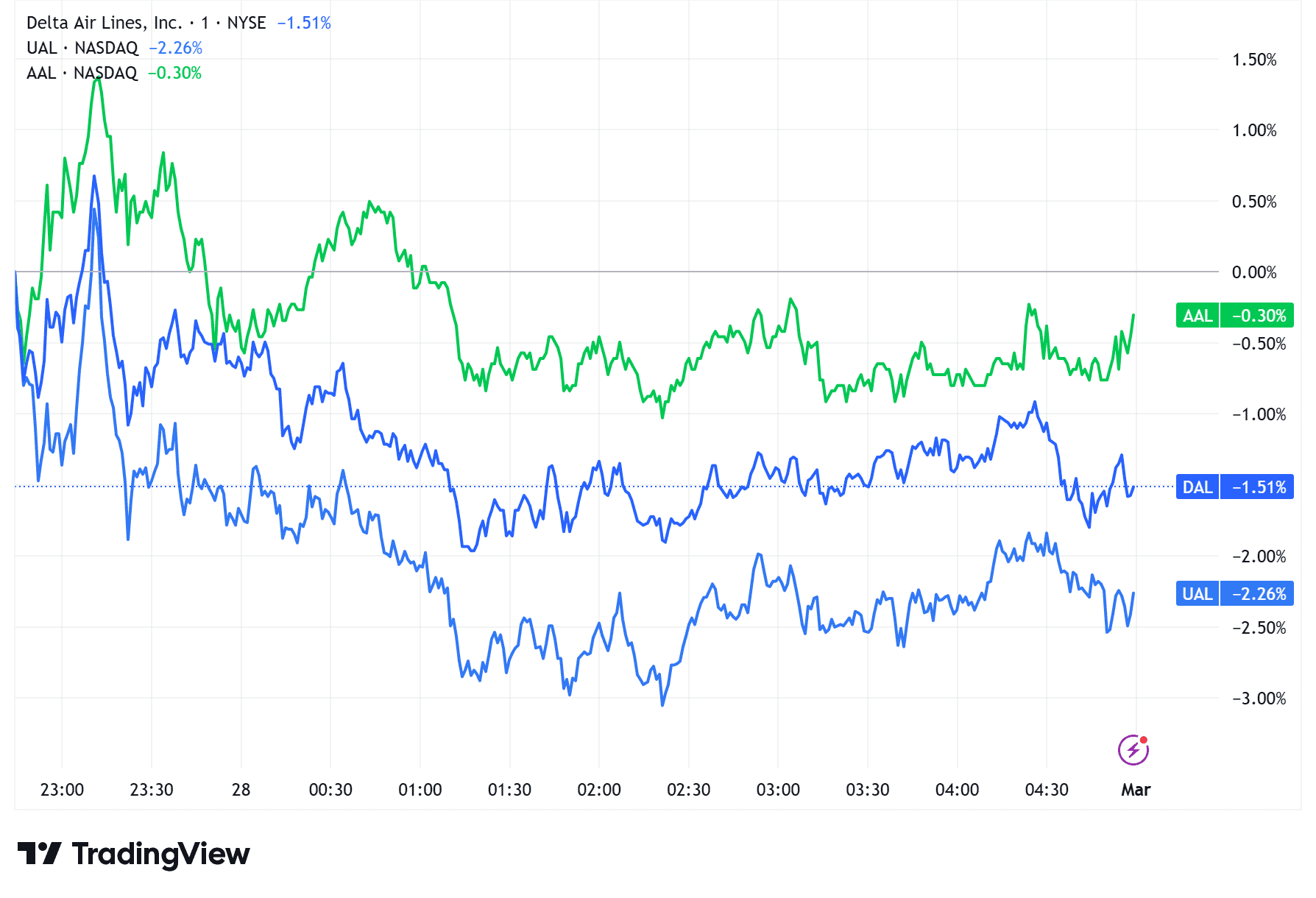

Airlines Become the Conflict’s Casualties

Commercial aviation, by contrast, has become a clear loser in this round of Middle East tensions. Data show that the four major U.S. carriers — Delta Air Lines Inc. (DAL), United Airlines Holdings Inc. (UAL), American Airlines Group Inc. (AAL), and Southwest Airlines Co. (LUV) — all fell in pre‑market trading.

The Middle East is a critical transit hub for global routes. After the strikes and subsequent Iranian missile retaliation, oil prices spiked and airspace across the region closed for consecutive days. Major hubs such as Dubai and Doha halted operations, forcing widespread flight cancellations.

Airlines now face a double blow. Direct losses stem from scrapped flights and refunds, while indirect losses arise from rerouting — higher fuel consumption, crew expenses, and reduced aircraft utilization. These pressures compound quickly when sustained for days or weeks.

Maritime Transport Faces Parallel Pressures

The Strait of Hormuz is one of the world’s most critical maritime chokepoints, linking the Persian Gulf to the Gulf of Oman and the Arabian Sea and serving as a vital artery for Middle Eastern oil exports. Iran, itself a major producer, sits directly on the passage.

On Sunday, Bloomberg reported that oil and gas shipments through the Strait had largely ground to a halt. The Islamic Revolutionary Guard Corps warned commercial vessels that the waterway was unsafe. Analysts at RBC Capital Markets noted that the Guard “could still deploy small boats, mines, drones, and missiles to deter shipping until hostilities end,” forcing insurers and operators to steer clear of the route.

The financial impact extends well beyond halted cargoes. Shipping operators are contending with soaring fuel costs as oil rises. Unless freight rates climb in tandem, profit margins will shrink. Vessels entering or leaving the Hormuz corridor face sharply higher war‑risk premiums and insurance surcharges. Added to that, the possibility of prolonged disruption is undermining global‑trade sentiment, pressuring both freight markets and broader demand outlooks

Recommended Articles