Alphabet, Apple, and Microsoft Got Kicked Out of the $4 Trillion Club. Could Nvidia Be Next?

Key Points

Nvidia stands to benefit from increased hyperscaler capital expenditures.

The company's order book depends heavily on data center spending.

Rubin could help Nvidia expand the use cases for its graphics processing units beyond the data center.

- 10 stocks we like better than Nvidia ›

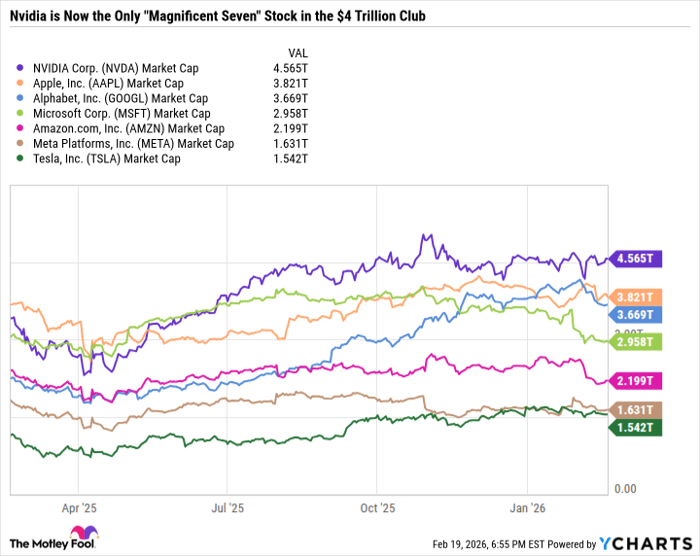

Microsoft surpassed $4 trillion in market capitalization last October. At the time of this writing, it has fallen below $3 trillion. Alphabet and Apple were both over $4 trillion in early February but are now down 11.8% and 9.7%, respectively, from their highs. That leaves Nvidia (NASDAQ: NVDA) with a table for one at the $4 trillion club.

With a market cap of $4.58 trillion, Nvidia would have to fall by 12.7% to lose its seat at the $4 trillion club. With a highly anticipated earnings report on Feb. 25, some investors may fear that Nvidia could soon get caught up in the growth stock sell-off.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Here's what investors should look for when Nvidia reports earnings, and if the artificial intelligence (AI) stock is a buy now.

Image source: Getty Images.

Nvidia is a bargain

Nvidia is valued largely based on its earnings growth. It has a price-to-earnings (P/E) ratio of 46.5 based on its trailing earnings, but just 24.2 based on the stock price divided by its annual earnings per share estimates over the next year.

For context, the S&P 500 (SNPINDEX: ^GSPC) has a 23.6 forward P/E ratio. And with Nvidia projected to continue growing earnings faster than the index over the long term, the stock is a compelling value as long as it keeps delivering decent results.

The biggest risk to Nvidia's investment thesis

With $99.2 billion in trailing-12-month net income, Nvidia could become not only the largest company in the world but also the most profitable within the next couple of years. But since Nvidia is so large, it takes a considerable amount of deal-making to move the needle.

Arguably, the biggest long-term risk to Nvidia is that its sheer size makes it heavily dependent on massive spending from key hyperscale customers. For example, Amazon plans to spend a staggering $200 billion on capital expenditures (capex) in 2026, mainly on AI, automation, and robotics. For context, Amazon's cash capex was under $50 billion in 2023.

In a similar vein, Microsoft is ramping up its spending, which is taking a sledgehammer to its free cash flow.

In just a couple of years, many big-tech hyperscalers have gone from capital-light, high-margin business models to capital-intensive companies. So far, investors aren't too happy -- as evidenced by Microsoft and Amazon being the two worst-performing "Magnificent Seven" stocks in 2026.

Data by YCharts.

Nvidia's growth rate could decline if hyperscalers slow their spending. Or worse, if key customer capex growth turns negative, Nvidia could face a cyclical downturn.

Nvidia is poised for a record year

With so many hyperscalers increasing 2026 capex, Nvidia's financials will most likely be excellent in the near term. But that's probably already baked into Nvidia's stock price. Rather, long-term investors should be focusing on Nvidia's next-generation Rubin chip rollout, which will mark the next stage in its order backlog and help secure its growth over the medium term.

In January, Nvidia forecast that it would begin shipping Rubin-based products in the second half of 2026. The upcoming Feb. 25 earnings call marks the first earnings release since Nvidia announced six new chips at CES. Investors will want to know if the release is still on track and how much of the latest capex increase is being captured by Nvidia.

Zooming out longer term, Nvidia's untapped opportunity is to monetize end markets beyond generative AI, such as autonomous AI, robotics, self-driving cars, and edge AI for industrial and commercial workflows.

Nvidia remains a high-conviction buy

In its current form, Nvidia heavily depends on a handful of customers in a key market -- data centers. A staggering 89.8% of third-quarter fiscal 2026 revenue came from its data center segment. The more Nvidia can take AI beyond the data center, the more diversified it will become, which could help broaden its customer base and reduce its vulnerability to a cyclical downturn.

Nvidia has held up better than its Magnificent Seven peers because it is benefiting from increased hyperscaler spending. However, investors care more about where a company is going than where it has been. And if 2026 marks a cyclical peak in capex spending, Nvidia could fall under pressure.

The good news is that the stock is still an incredible value for long-term investors. For the reasons mentioned, Nvidia will likely blow expectations out of the water in the near term. And if the stock price languishes, Nvidia will become too cheap to ignore -- even amid a technical slowdown.

All told, I don't think Nvidia will be kicked out of the $4 trillion club. Investors who are skeptical of the payoff of hyperscale spending may want to take a closer look at buying Nvidia instead of cloud infrastructure companies, as it remains an ultra-high margin, high-cash-flow business even after factoring in spending on Rubin.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $409,970!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,174,241!*

Now, it’s worth noting Stock Advisor’s total average return is 889% — a market-crushing outperformance compared to 192% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 24, 2026.

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has a disclosure policy.

Recommended Articles