Prediction: Broadcom Stock Will Reach $450 By the End of the Year

Key Points

Broadcom is designing custom AI chips in collaboration with AI hyperscalers.

These products have proven a huge winner, and the stock has jumped.

Even at a lower valuation, Broadcom's stock could make solid gains in 2026.

- 10 stocks we like better than Broadcom ›

Broadcom (NASDAQ: AVGO) is one of the more popular tech stocks right now. Its products are surging in popularity, and can be seen as a viable alternative to graphics processing units (GPUs) from Nvidia (NASDAQ: NVDA). That's a monster of a company to compete against, but Broadcom is succeeding thanks to its custom-designed AI chips.

Although Broadcom's stock is about $330 right now, I think it could reach $450 by the end of the year. That's about a 36% upside -- easily a market-crushing stock. So, how can Broadcom dominate 2026? Simple. It just needs to keep doing what it has been doing.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Its AI semiconductor division has proven a bright spot

This company isn't just AI chips and connectivity switches. It has a diverse lineup of software, mainframe hardware, and even cybersecurity. But the most popular division by far is Broadcom's AI semiconductors.

Broadcom has emerged into the AI computing scene thanks to its ASICs (application-specific integrated circuits). ASICs have been around forever, but Broadcom has become the primary company launching AI versions of them. Essentially, it partners with a client to design an AI chip meant specifically for their workloads. Then, it works with production facilities to manufacture these chips.

At the end, the AI hyperscaler gets a chip specifically for its workload that it didn't have to figure out how to produce (an extremely in-depth and nuanced process).

The most famous example of one of Broadcom's custom AI chips is the Tensor Processing Unit (TPU) from Google. The TPU has been a bright spot in Google's internal AI capabilities, as well as in other clients' systems, because it's available for rent via Google Cloud.

Broadcom has several other clients that are currently in production, with more slated to launch later this year. This will drive outsized revenue growth for Broadcom, which is the primary reason why I'm bullish on it.

AI chips will be Broadcom's largest product by the end of the year

For the first-quarter of its fiscal 2026 (ended in early February), Broadcom expects its AI semiconductor revenue to double year over year to $8.2 billion. For reference, the total revenue for Broadcom is expected to be $19.1 billion.

However, there's something important to point out. If we subtract out the AI semiconductor revenue from Broadcom's $19.1 billion total projection for Q1 FY 2026, we're left with $10.9 billion in non-AI semiconductor revenue. In Q1 FY 2025, Broadcom generated $14.9 billion in revenue, or about $10.8 billion, with no AI semiconductor revenue. This means that Broadcom's core business isn't growing at all, and the growth is coming from AI.

This shouldn't come as too much of a surprise, as Broadcom has likely shifted resources around to maximize its AI growth while it's the biggest thing. However, if something should happen to AI spending, Broadcom could be in a bit of trouble.

Regardless, I think AI spending is set to continue for several years, with many projects pointing to it lasting through 2030 at a minimum. Wall Street analyst projections back this up, as they expect companywide revenue growth to be 52% in FY 2026 and 39% in FY 2027. All this adds up to a stock that can soar, and I think the $450 price target by the end of the year is achievable.

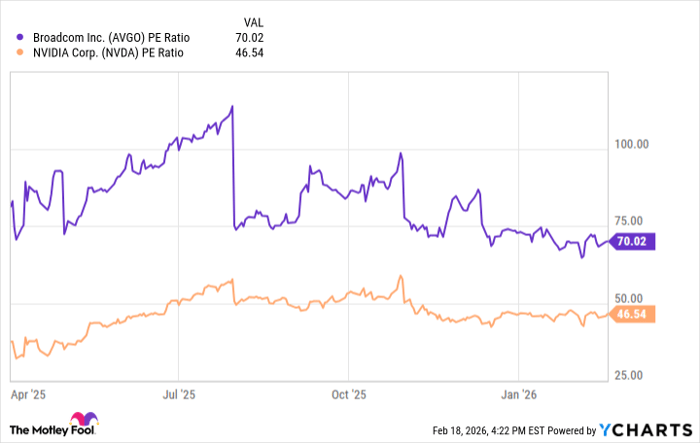

The average estimate for analysts is $10.27 in earnings per share (EPS). Currently, Broadcom trades for a price-to-earnings (P/E) ratio of 70, which is very expensive. A more reasonable price tag is 45 times trailing earnings, which is where Nvidia currently trades.

AVGO PE Ratio data by YCharts.

With a P/E ratio of 45 and EPS of $10.27, that would price the stock at over $462 per share. That exceeds the original $450 target, and if the market deems Broadcom to have a higher multiple than 45 times earnings, it could be worth even more.

If Broadcom can deliver monster growth over the next few months thanks to its AI chips, it can be a huge winner this year. I think investors should consider buying the stock right now as it's down around 20% from its all-time high.

Should you buy stock in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $424,262!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,163,635!*

Now, it’s worth noting Stock Advisor’s total average return is 904% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 23, 2026.

Keithen Drury has positions in Broadcom and Nvidia. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles